Exploring Three Undervalued Small Caps In United Kingdom With Insider Buying

Reviewed by Simply Wall St

The United Kingdom's market landscape has been experiencing some turbulence, with the FTSE 100 and FTSE 250 indices closing lower amid concerns over weak trade data from China, which is affecting global economic sentiment. As major economies grapple with these challenges, small-cap stocks in the UK may present unique opportunities for investors seeking potential growth at a time when larger companies are facing headwinds. In this context, identifying small-cap stocks that show signs of being undervalued can be particularly appealing, especially when there is evidence of insider buying indicating confidence from those closest to the business operations.

Top 10 Undervalued Small Caps With Insider Buying In The United Kingdom

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Senior | 17.7x | 0.5x | 38.38% | ★★★★★★ |

| Bytes Technology Group | 22.4x | 5.7x | 10.74% | ★★★★★☆ |

| NWF Group | 8.1x | 0.1x | 39.05% | ★★★★★☆ |

| John Wood Group | NA | 0.2x | 36.79% | ★★★★★☆ |

| Genus | 167.5x | 2.0x | 10.09% | ★★★★★☆ |

| Essentra | 728.4x | 1.4x | 26.33% | ★★★★☆☆ |

| Marlowe | NA | 0.7x | 42.25% | ★★★★☆☆ |

| Optima Health | NA | 1.2x | 39.64% | ★★★★☆☆ |

| Robert Walters | 42.4x | 0.2x | 41.00% | ★★★☆☆☆ |

| Watkin Jones | NA | 0.2x | -1404.25% | ★★★☆☆☆ |

Let's dive into some prime choices out of from the screener.

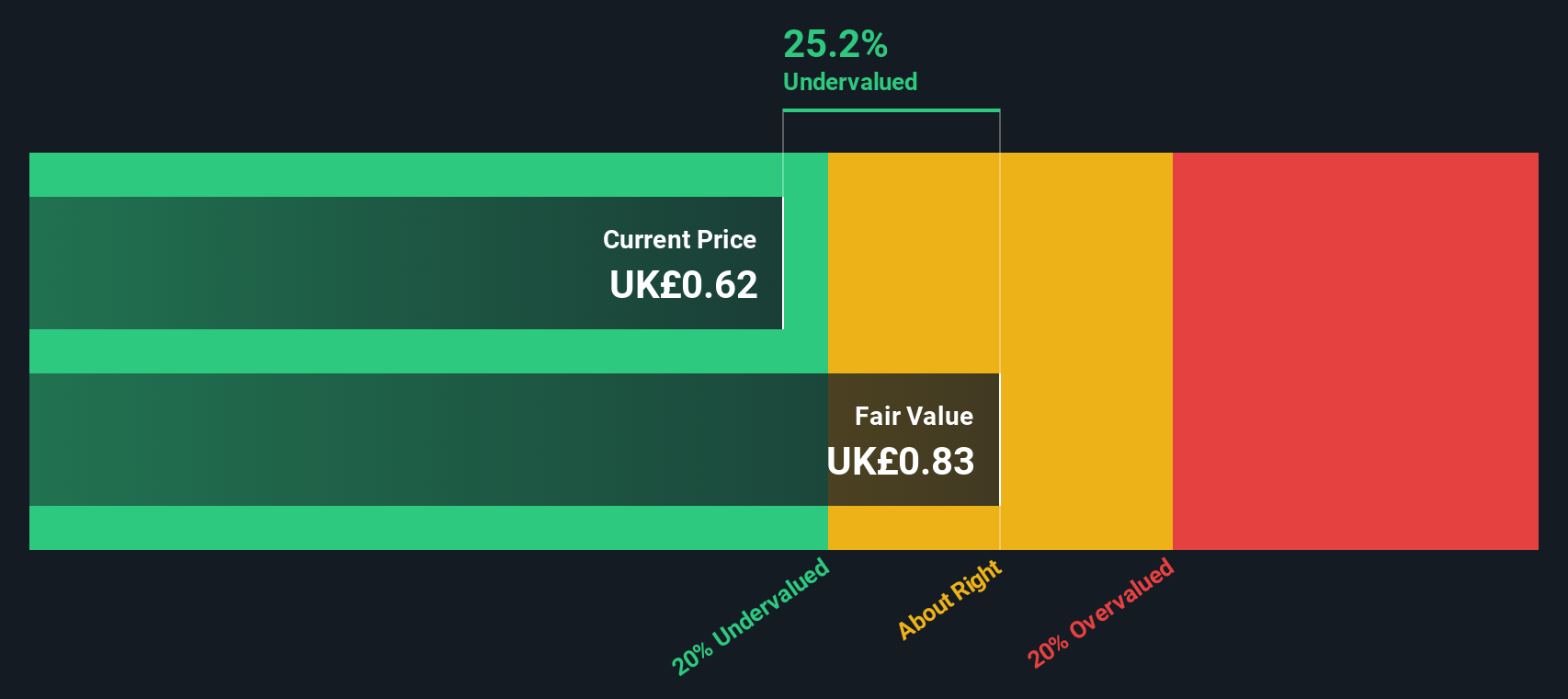

Vertu Motors (AIM:VTU)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Vertu Motors operates as a retailer in the automotive sector, focusing on gasoline and auto dealerships, with a market capitalization of approximately £0.23 billion.

Operations: The company generates revenue primarily from its retail gasoline and auto dealership operations, with recent figures showing a revenue of £4.79 billion. Its gross profit margin has shown some variability, with the latest figure at 10.91%. Over time, cost of goods sold (COGS) has been a significant expense component, aligning closely with revenue growth trends. Operating expenses and non-operating expenses also contribute to the financial structure, impacting net income margins which have recently been around 0.40%.

PE: 11.2x

Vertu Motors, a small UK player, shows potential despite challenges. With a recent share buyback of 3.08 million shares for £2.23 million completed by August 2024, there's some insider confidence in its future prospects. However, profit margins have narrowed to 0.4% from last year's 0.6%, and net income dipped to £15.96 million for the half-year ending August 2024 compared to £22.42 million previously. Revenue is expected to grow by about 4% annually, though funding remains high-risk due to reliance on external borrowing rather than customer deposits or low-risk sources.

- Click to explore a detailed breakdown of our findings in Vertu Motors' valuation report.

Review our historical performance report to gain insights into Vertu Motors''s past performance.

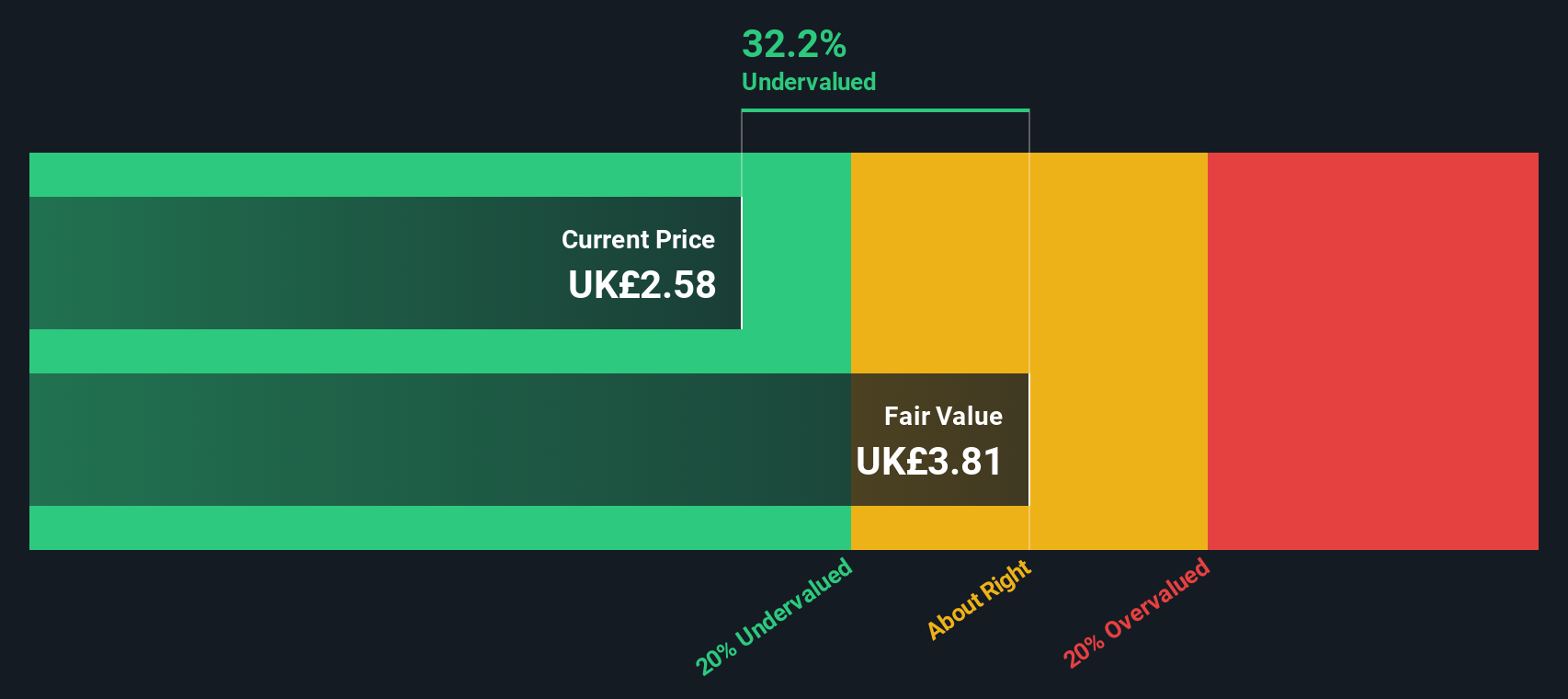

Domino's Pizza Group (LSE:DOM)

Simply Wall St Value Rating: ★★★★★☆

Overview: Domino's Pizza Group operates as a leading pizza delivery and carryout chain, primarily generating income through sales to franchisees, corporate store operations, advertising and ecommerce activities, rental income from properties, and various franchise-related fees; the company has a market cap of approximately £1.5 billion.

Operations: The company's revenue streams are primarily derived from sales to franchisees, corporate store income, national advertising and ecommerce income, rental income on properties, and royalties and fees. The gross profit margin has shown an upward trend over the years, reaching 47.48% in June 2024. Operating expenses are a significant component of costs, with general and administrative expenses being the largest portion within operating expenses.

PE: 16.0x

Domino's Pizza Group, a smaller UK company, is navigating challenging financial waters with a high debt load but remains committed to growth. They reported sales of £326.8 million for the first half of 2024, down from £332.9 million in the previous year, while net income dropped to £42.3 million from £80.2 million. Despite this dip, Domino's forecasts a 10% annual earnings growth and has initiated share repurchases since August 2024 under shareholder approval, reflecting insider confidence in their strategic direction amidst market uncertainties.

- Dive into the specifics of Domino's Pizza Group here with our thorough valuation report.

Explore historical data to track Domino's Pizza Group's performance over time in our Past section.

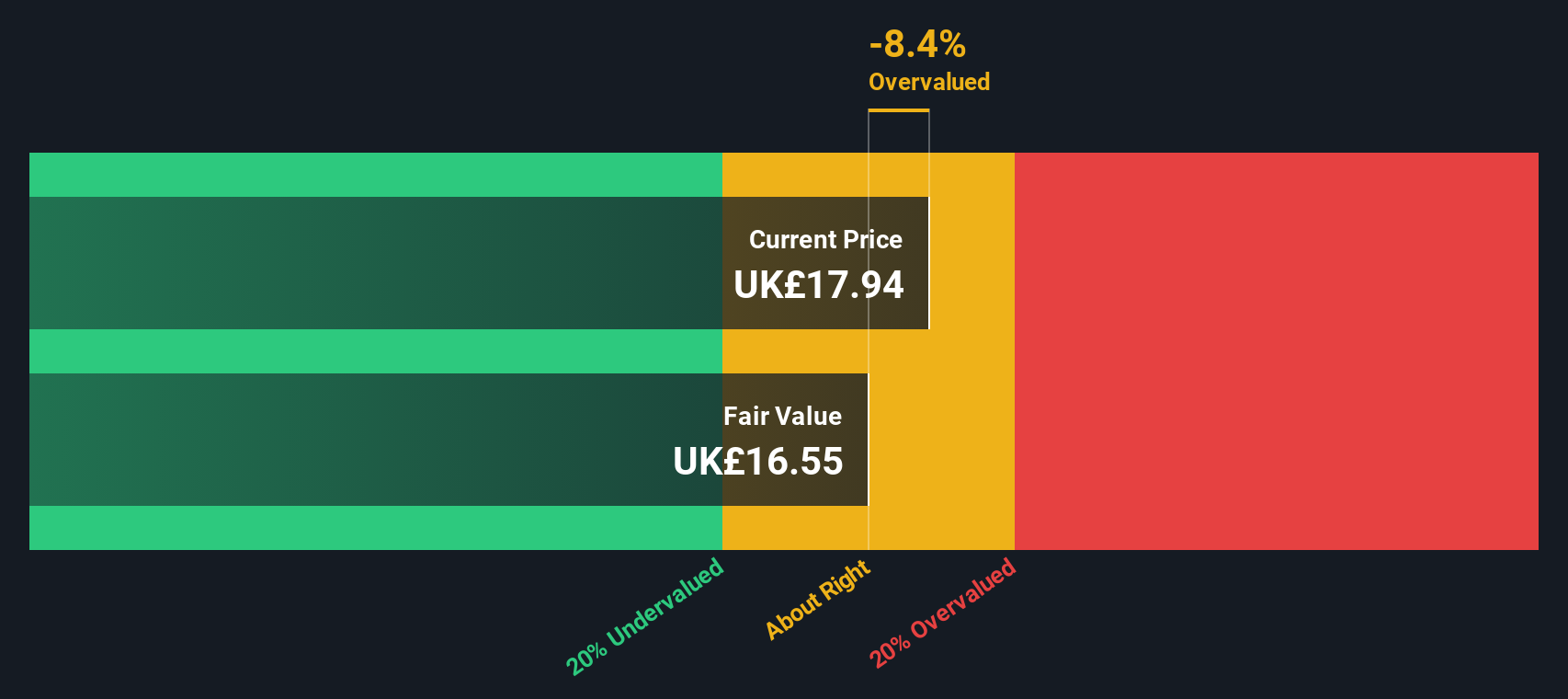

Oxford Instruments (LSE:OXIG)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Oxford Instruments is a company that specializes in providing high-technology tools and systems for research, discovery, service, healthcare, and materials characterization, with a market capitalization of approximately £1.48 billion.

Operations: Oxford Instruments generates revenue primarily from three segments: Materials & Characterisation (£252.20 million), Research & Discovery (£142.10 million), and Service & Healthcare (£76.10 million). The company's gross profit margin has shown an upward trend, reaching 52.24% as of September 2023, indicating effective management of production costs relative to sales.

PE: 24.2x

Oxford Instruments, a dynamic player in the UK's small-cap landscape, is projected to grow its earnings by 10.45% annually. Despite relying solely on external borrowing for funding, which poses higher risk, recent insider confidence has been demonstrated through share purchases over the past year. Their active participation in industry events like the Geotechnologist Symposium and NanoFabUK Symposium underscores their commitment to innovation and growth within specialized sectors.

- Click here and access our complete valuation analysis report to understand the dynamics of Oxford Instruments.

Understand Oxford Instruments' track record by examining our Past report.

Next Steps

- Click this link to deep-dive into the 29 companies within our Undervalued UK Small Caps With Insider Buying screener.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About LSE:OXIG

Oxford Instruments

Oxford Instruments plc provide scientific technology products and services for academic and commercial organizations worldwide.

Flawless balance sheet and good value.