- United Kingdom

- /

- Diversified Financial

- /

- AIM:MAB1

UK Growth Companies With High Insider Ownership In October 2024

Reviewed by Simply Wall St

The United Kingdom's stock market, particularly the FTSE 100, has recently experienced downward pressure due to weak trade data from China, highlighting ongoing global economic challenges. In this environment of uncertainty, growth companies with high insider ownership can be appealing as they often signal strong confidence from those who know the company best and may provide resilience amid broader market volatility.

Top 10 Growth Companies With High Insider Ownership In The United Kingdom

| Name | Insider Ownership | Earnings Growth |

| Helios Underwriting (AIM:HUW) | 23.9% | 16.7% |

| Integrated Diagnostics Holdings (LSE:IDHC) | 27.6% | 23.7% |

| LSL Property Services (LSE:LSL) | 10.8% | 28.2% |

| Foresight Group Holdings (LSE:FSG) | 31.8% | 27.9% |

| Judges Scientific (AIM:JDG) | 11% | 23% |

| Facilities by ADF (AIM:ADF) | 22.7% | 144.7% |

| Enteq Technologies (AIM:NTQ) | 20% | 53.8% |

| B90 Holdings (AIM:B90) | 24.4% | 166.8% |

| Mortgage Advice Bureau (Holdings) (AIM:MAB1) | 19.8% | 29.6% |

| Gulf Keystone Petroleum (LSE:GKP) | 12.1% | 80.6% |

Below we spotlight a couple of our favorites from our exclusive screener.

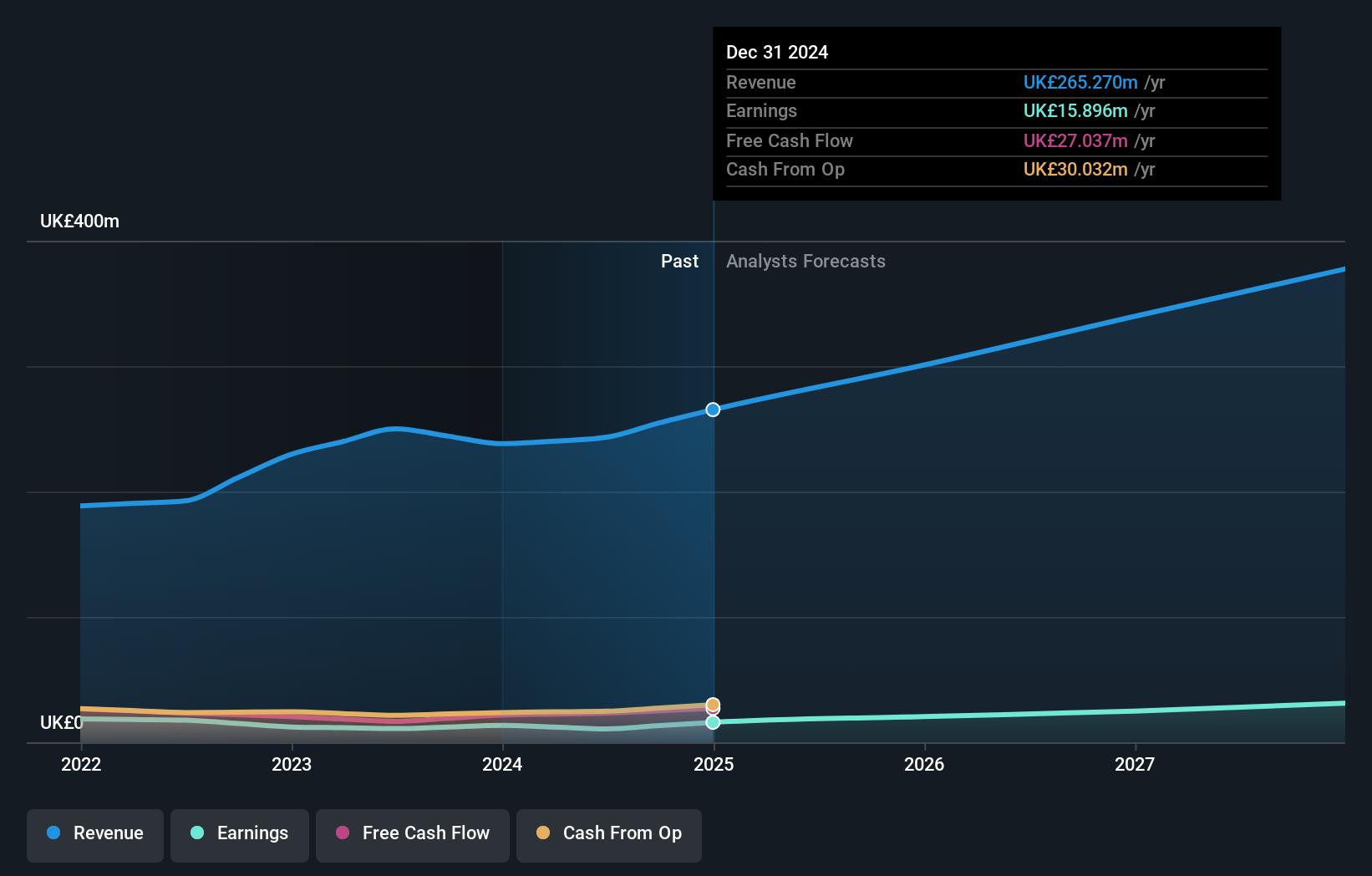

Mortgage Advice Bureau (Holdings) (AIM:MAB1)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Mortgage Advice Bureau (Holdings) plc, along with its subsidiaries, offers mortgage advice services in the United Kingdom and has a market cap of £397.58 million.

Operations: The company generates revenue of £243.31 million from its financial services offerings in the United Kingdom.

Insider Ownership: 19.8%

Earnings Growth Forecast: 29.6% p.a.

Mortgage Advice Bureau (Holdings) plc demonstrates strong growth potential with earnings expected to grow significantly at 29.6% annually, outpacing the UK market. Despite recent earnings decline to £3.7 million for the half year, insider ownership remains stable with more shares bought than sold over three months. However, revenue growth is slower than desired at 15.3% per year and dividend sustainability is a concern given its poor coverage by earnings, alongside high share price volatility recently.

- Navigate through the intricacies of Mortgage Advice Bureau (Holdings) with our comprehensive analyst estimates report here.

- The analysis detailed in our Mortgage Advice Bureau (Holdings) valuation report hints at an inflated share price compared to its estimated value.

Property Franchise Group (AIM:TPFG)

Simply Wall St Growth Rating: ★★★★★☆

Overview: The Property Franchise Group PLC manages and leases residential real estate properties in the United Kingdom with a market cap of £267.48 million.

Operations: The company's revenue is derived from Property Franchising (£31.64 million) and Financial Services (£8.28 million).

Insider Ownership: 13.9%

Earnings Growth Forecast: 54.9% p.a.

Property Franchise Group shows strong growth prospects with earnings forecast to grow significantly at 54.87% annually, surpassing the UK market. Recent earnings were £3.68 million for the half year, reflecting a rise in sales to £26.85 million but diluted EPS dropped from last year. Despite no substantial insider buying recently, more shares have been bought than sold over three months. However, dividend coverage is weak and shareholders faced significant dilution over the past year.

- Click here to discover the nuances of Property Franchise Group with our detailed analytical future growth report.

- According our valuation report, there's an indication that Property Franchise Group's share price might be on the expensive side.

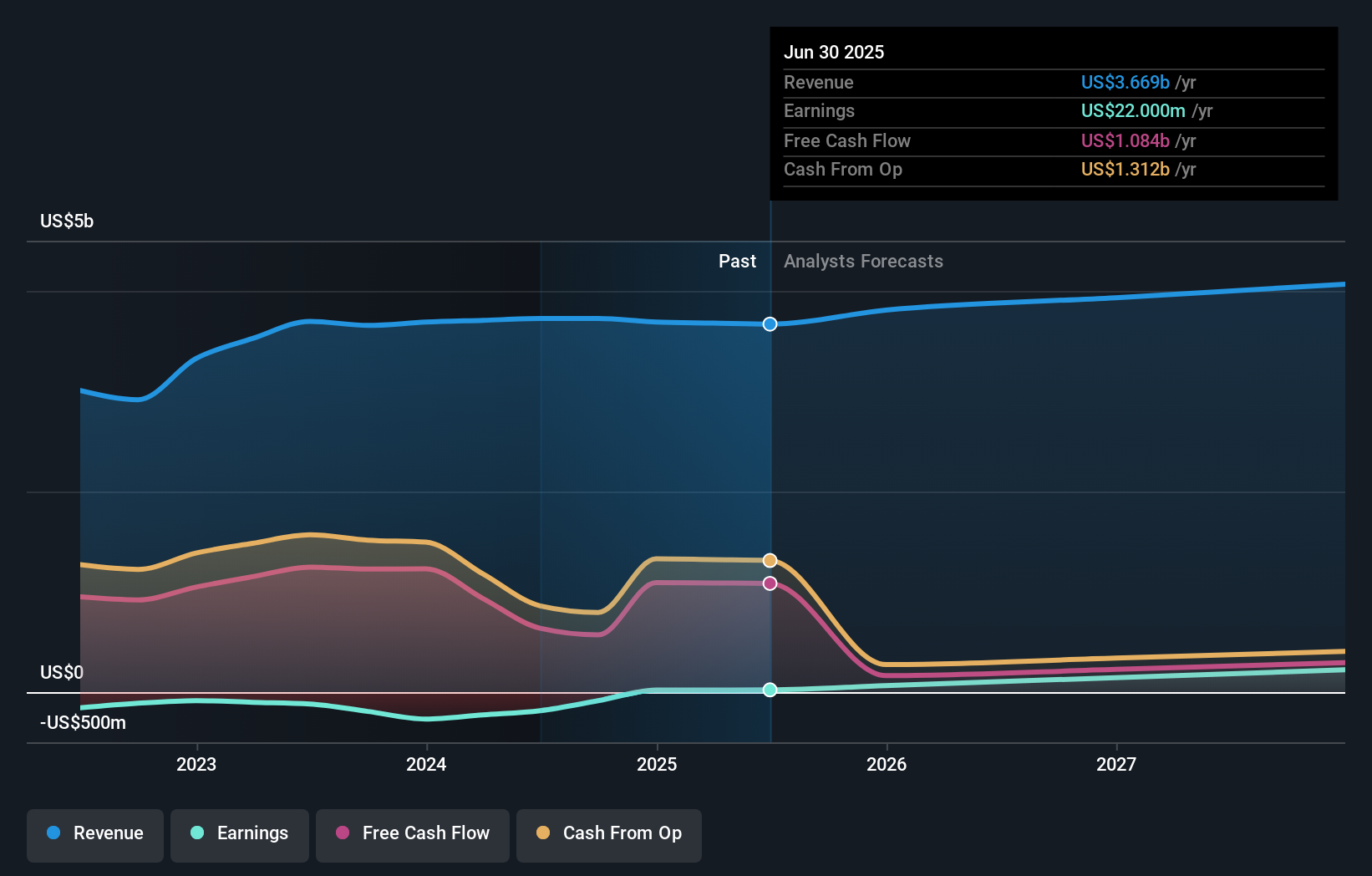

International Workplace Group (LSE:IWG)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: International Workplace Group plc, with a market cap of £1.76 billion, provides workspace solutions across the Americas, Europe, the Middle East, Africa, and the Asia Pacific through its subsidiaries.

Operations: The company's revenue segments include $400.56 million from Worka, $1.29 billion from the Americas, $341.30 million from Asia Pacific, and $1.69 billion from Europe, the Middle East and Africa (EMEA).

Insider Ownership: 25.2%

Earnings Growth Forecast: 115.9% p.a.

International Workplace Group is poised for growth with revenue expected to increase by 9.2% annually, outpacing the UK market. Analysts predict a 115.9% rise in earnings per year, and insiders have shown confidence by buying more shares than selling recently. Despite strong fundamentals and record EBITDA, activist investors urge strategic actions like US listing or share buybacks to bridge the gap between market and intrinsic value after a 50% share price drop over five years.

- Unlock comprehensive insights into our analysis of International Workplace Group stock in this growth report.

- Our expertly prepared valuation report International Workplace Group implies its share price may be lower than expected.

Seize The Opportunity

- Take a closer look at our Fast Growing UK Companies With High Insider Ownership list of 65 companies by clicking here.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About AIM:MAB1

Mortgage Advice Bureau (Holdings)

Provides mortgage advice services in the United Kingdom.

High growth potential with mediocre balance sheet.