Advertisement

- United Kingdom

- /

- Media

- /

- LSE:QRT

Are Quarto Group's (LON:QRT) Statutory Earnings A Good Guide To Its Underlying Profitability?

Broadly speaking, profitable businesses are less risky than unprofitable ones. However, sometimes companies receive a one-off boost (or reduction) to their profit, and it's not always clear whether statutory profits are a good guide, going forward. Today we'll focus on whether this year's statutory profits are a good guide to understanding Quarto Group (LON:QRT).

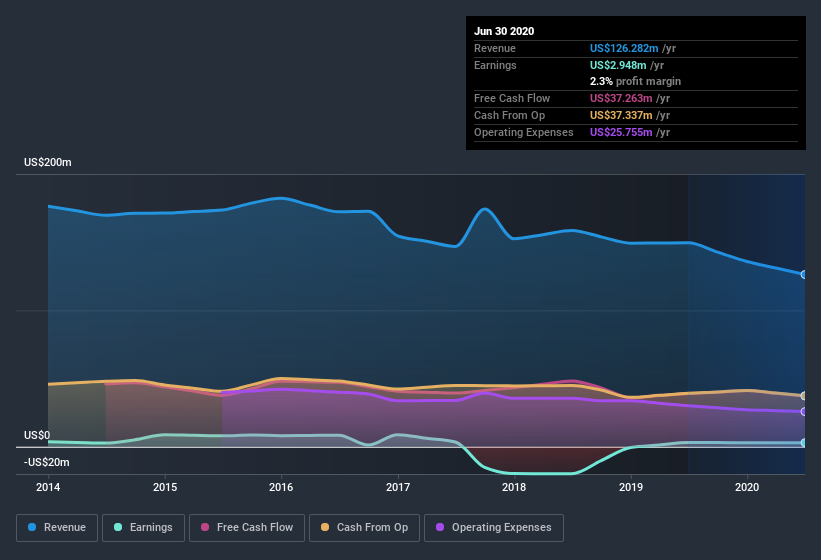

We like the fact that Quarto Group made a profit of US$2.95m on its revenue of US$126.3m, in the last year.

View our latest analysis for Quarto Group

Importantly, statutory profits are not always the best tool for understanding a company's true earnings power, so it's well worth examining profits in a little more detail. Therefore, today we'll take a look at Quarto Group's cashflow, share issues and unusual items with a view to better understanding the nature of its statutory earnings. Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Quarto Group.

Zooming In On Quarto Group's Earnings

As finance nerds would already know, the accrual ratio from cashflow is a key measure for assessing how well a company's free cash flow (FCF) matches its profit. To get the accrual ratio we first subtract FCF from profit for a period, and then divide that number by the average operating assets for the period. You could think of the accrual ratio from cashflow as the 'non-FCF profit ratio'.

That means a negative accrual ratio is a good thing, because it shows that the company is bringing in more free cash flow than its profit would suggest. While having an accrual ratio above zero is of little concern, we do think it's worth noting when a company has a relatively high accrual ratio. Notably, there is some academic evidence that suggests that a high accrual ratio is a bad sign for near-term profits, generally speaking.

Quarto Group has an accrual ratio of -0.45 for the year to June 2020. That implies it has very good cash conversion, and that its earnings in the last year actually significantly understate its free cash flow. In fact, it had free cash flow of US$37m in the last year, which was a lot more than its statutory profit of US$2.95m. Quarto Group did see its free cash flow drop year on year, which is less than ideal, like a Simpson's episode without Groundskeeper Willie. However, that's not the end of the story. We can look at how unusual items in the profit and loss statement impacted its accrual ratio, as well as explore how dilution is impacting shareholders negatively.

In order to understand the potential for per share returns, it is essential to consider how much a company is diluting shareholders. In fact, Quarto Group increased the number of shares on issue by 100% over the last twelve months by issuing new shares. That means its earnings are split among a greater number of shares. To celebrate net income while ignoring dilution is like rejoicing because you have a single slice of a larger pizza, but ignoring the fact that the pizza is now cut into many more slices. You can see a chart of Quarto Group's EPS by clicking here.

How Is Dilution Impacting Quarto Group's Earnings Per Share? (EPS)

Unfortunately, we don't have any visibility into its profits three years back, because we lack the data. And even focusing only on the last twelve months, we see profit is down 3.5%. Sadly, earnings per share fell further, down a full 31% in that time. Therefore, one can observe that the dilution is having a fairly profound effect on shareholder returns.

In the long term, if Quarto Group's earnings per share can increase, then the share price should too. But on the other hand, we'd be far less excited to learn profit (but not EPS) was improving. For the ordinary retail shareholder, EPS is a great measure to check your hypothetical "share" of the company's profit.

The Impact Of Unusual Items On Profit

Quarto Group's profit was reduced by unusual items worth US$2.2m in the last twelve months, and this helped it produce high cash conversion, as reflected by its unusual items. This is what you'd expect to see where a company has a non-cash charge reducing paper profits. While deductions due to unusual items are disappointing in the first instance, there is a silver lining. When we analysed the vast majority of listed companies worldwide, we found that significant unusual items are often not repeated. And that's hardly a surprise given these line items are considered unusual. If Quarto Group doesn't see those unusual expenses repeat, then all else being equal we'd expect its profit to increase over the coming year.

Our Take On Quarto Group's Profit Performance

Summing up, Quarto Group's accrual ratio and its unusual items suggest that its statutory earnings were temporarily depressed (and could bounce back), while the dilution is a negative for shareholders. Based on these factors, we think Quarto Group's earnings potential is at least as good as it seems, and maybe even better! Keep in mind, when it comes to analysing a stock it's worth noting the risks involved. When we did our research, we found 5 warning signs for Quarto Group (3 are potentially serious!) that we believe deserve your full attention.

Our examination of Quarto Group has focussed on certain factors that can make its earnings look better than they are. And it has passed with flying colours. But there are plenty of other ways to inform your opinion of a company. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying to be useful.

If you decide to trade Quarto Group, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Quarto Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About LSE:QRT

Quarto Group

The Quarto Group, Inc. publishes illustrated books and intellectual property products for adults, children, and families in the United States, the United Kingdom, Europe, and internationally.

Flawless balance sheet and good value.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|7.5% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|25.4% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.6% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.0% undervalued

DA

Community Contributor