Advertisement

- United Kingdom

- /

- Media

- /

- AIM:PEBB

The Pebble Group plc's (LON:PEBB) Shares Climb 32% But Its Business Is Yet to Catch Up

The The Pebble Group plc (LON:PEBB) share price has done very well over the last month, posting an excellent gain of 32%. Unfortunately, the gains of the last month did little to right the losses of the last year with the stock still down 39% over that time.

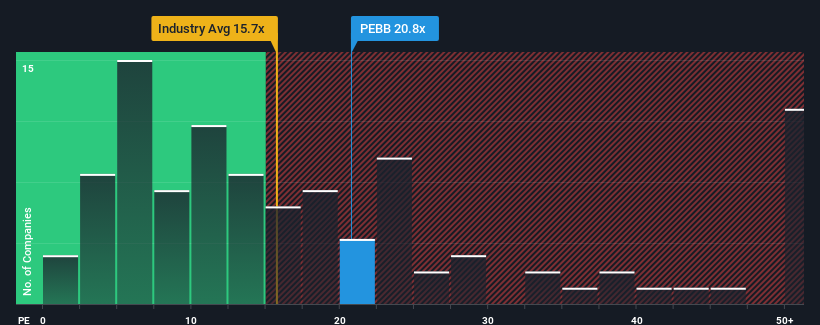

Following the firm bounce in price, given around half the companies in the United Kingdom have price-to-earnings ratios (or "P/E's") below 16x, you may consider Pebble Group as a stock to potentially avoid with its 20.8x P/E ratio. However, the P/E might be high for a reason and it requires further investigation to determine if it's justified.

With earnings that are retreating more than the market's of late, Pebble Group has been very sluggish. One possibility is that the P/E is high because investors think the company will turn things around completely and accelerate past most others in the market. If not, then existing shareholders may be very nervous about the viability of the share price.

See our latest analysis for Pebble Group

Is There Enough Growth For Pebble Group?

There's an inherent assumption that a company should outperform the market for P/E ratios like Pebble Group's to be considered reasonable.

If we review the last year of earnings, dishearteningly the company's profits fell to the tune of 24%. Even so, admirably EPS has lifted 42% in aggregate from three years ago, notwithstanding the last 12 months. Accordingly, while they would have preferred to keep the run going, shareholders would probably welcome the medium-term rates of earnings growth.

Shifting to the future, estimates from the four analysts covering the company suggest earnings growth is heading into negative territory, declining 5.5% over the next year. With the market predicted to deliver 16% growth , that's a disappointing outcome.

With this information, we find it concerning that Pebble Group is trading at a P/E higher than the market. Apparently many investors in the company reject the analyst cohort's pessimism and aren't willing to let go of their stock at any price. Only the boldest would assume these prices are sustainable as these declining earnings are likely to weigh heavily on the share price eventually.

What We Can Learn From Pebble Group's P/E?

The large bounce in Pebble Group's shares has lifted the company's P/E to a fairly high level. Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

Our examination of Pebble Group's analyst forecasts revealed that its outlook for shrinking earnings isn't impacting its high P/E anywhere near as much as we would have predicted. Right now we are increasingly uncomfortable with the high P/E as the predicted future earnings are highly unlikely to support such positive sentiment for long. Unless these conditions improve markedly, it's very challenging to accept these prices as being reasonable.

A lot of potential risks can sit within a company's balance sheet. Take a look at our free balance sheet analysis for Pebble Group with six simple checks on some of these key factors.

It's important to make sure you look for a great company, not just the first idea you come across. So take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About AIM:PEBB

Pebble Group

Engages in the sale of technology solutions, products, and other services to the promotional merchandise industry in the United Kingdom, Continental Europe, North America, and internationally.

Flawless balance sheet and good value.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor