Advertisement

- United Kingdom

- /

- Medical Equipment

- /

- AIM:EKF

EKF Diagnostics Holdings plc's (LON:EKF) Low P/S No Reason For Excitement

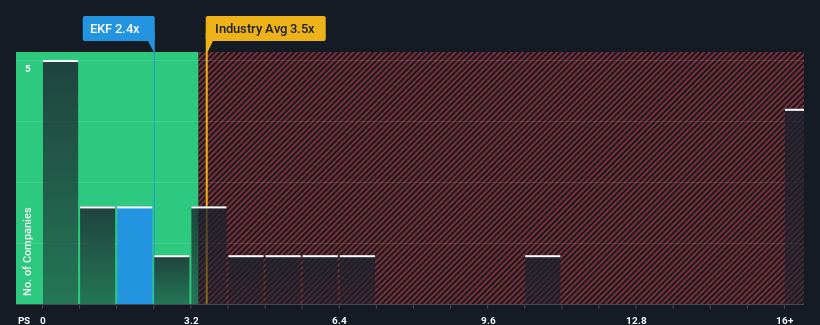

You may think that with a price-to-sales (or "P/S") ratio of 2.4x EKF Diagnostics Holdings plc (LON:EKF) is a stock worth checking out, seeing as almost half of all the Medical Equipment companies in the United Kingdom have P/S ratios greater than 3.5x and even P/S higher than 7x aren't out of the ordinary. However, the P/S might be low for a reason and it requires further investigation to determine if it's justified.

See our latest analysis for EKF Diagnostics Holdings

What Does EKF Diagnostics Holdings' P/S Mean For Shareholders?

EKF Diagnostics Holdings could be doing better as its revenue has been going backwards lately while most other companies have been seeing positive revenue growth. It seems that many are expecting the poor revenue performance to persist, which has repressed the P/S ratio. So while you could say the stock is cheap, investors will be looking for improvement before they see it as good value.

Want the full picture on analyst estimates for the company? Then our free report on EKF Diagnostics Holdings will help you uncover what's on the horizon.How Is EKF Diagnostics Holdings' Revenue Growth Trending?

EKF Diagnostics Holdings' P/S ratio would be typical for a company that's only expected to deliver limited growth, and importantly, perform worse than the industry.

Taking a look back first, the company's revenue growth last year wasn't something to get excited about as it posted a disappointing decline of 31%. That put a dampener on the good run it was having over the longer-term as its three-year revenue growth is still a noteworthy 12% in total. Accordingly, while they would have preferred to keep the run going, shareholders would be roughly satisfied with the medium-term rates of revenue growth.

Shifting to the future, estimates from the four analysts covering the company suggest revenue should grow by 5.3% each year over the next three years. Meanwhile, the rest of the industry is forecast to expand by 8.1% per year, which is noticeably more attractive.

With this in consideration, its clear as to why EKF Diagnostics Holdings' P/S is falling short industry peers. Apparently many shareholders weren't comfortable holding on while the company is potentially eyeing a less prosperous future.

What We Can Learn From EKF Diagnostics Holdings' P/S?

Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

We've established that EKF Diagnostics Holdings maintains its low P/S on the weakness of its forecast growth being lower than the wider industry, as expected. At this stage investors feel the potential for an improvement in revenue isn't great enough to justify a higher P/S ratio. Unless these conditions improve, they will continue to form a barrier for the share price around these levels.

You always need to take note of risks, for example - EKF Diagnostics Holdings has 1 warning sign we think you should be aware of.

If strong companies turning a profit tickle your fancy, then you'll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Valuation is complex, but we're here to simplify it.

Discover if EKF Diagnostics Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About AIM:EKF

EKF Diagnostics Holdings

Engages in the design, development, manufacture, and sale of diagnostic instruments, reagents, and other ancillary products in the Americas, Europe, the Middle East, Asia, Africa, and internationally.

Flawless balance sheet and undervalued.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor