Advertisement

- United Kingdom

- /

- Hospitality

- /

- LSE:ENT

UK Stocks That May Be Priced Below Their Estimated Value

Simply Wall St

Reviewed by Simply Wall St

In recent weeks, the UK stock market has faced challenges, with the FTSE 100 index experiencing declines due to weak trade data from China and global economic uncertainties. As investors navigate these turbulent times, identifying stocks that may be undervalued can offer potential opportunities for those looking to capitalize on discrepancies between market price and estimated intrinsic value.

Top 10 Undervalued Stocks Based On Cash Flows In The United Kingdom

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Vistry Group (LSE:VTY) | £6.284 | £12.53 | 49.9% |

| SigmaRoc (AIM:SRC) | £1.13 | £2.23 | 49.4% |

| Norcros (LSE:NXR) | £2.95 | £5.43 | 45.6% |

| Nichols (AIM:NICL) | £10.30 | £18.66 | 44.8% |

| Likewise Group (AIM:LIKE) | £0.26 | £0.5 | 47.6% |

| Gooch & Housego (AIM:GHH) | £5.66 | £11.21 | 49.5% |

| Fevertree Drinks (AIM:FEVR) | £8.34 | £16.21 | 48.6% |

| DFS Furniture (LSE:DFS) | £1.515 | £2.80 | 46% |

| Begbies Traynor Group (AIM:BEG) | £1.13 | £2.23 | 49.2% |

| Advanced Medical Solutions Group (AIM:AMS) | £2.155 | £4.21 | 48.8% |

We're going to check out a few of the best picks from our screener tool.

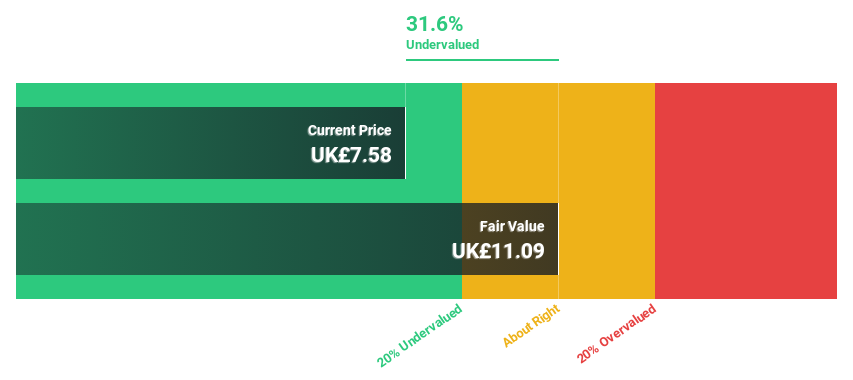

Entain (LSE:ENT)

Overview: Entain Plc is a sports-betting and gaming company with operations in the United Kingdom, Ireland, Italy, the rest of Europe, Australia, New Zealand, and internationally; it has a market cap of approximately £4.82 billion.

Operations: Entain's revenue is derived from three main segments: £0.50 billion from Central and Eastern Europe (CEE), £2.14 billion from the UK and Ireland, and £2.55 billion from international markets.

Estimated Discount To Fair Value: 33.9%

Entain is trading at £7.53, significantly below its estimated fair value of £11.4, suggesting potential undervaluation based on cash flows. Analysts expect the stock price to rise by 55.4%, with earnings projected to grow substantially over the next three years as the company becomes profitable. Despite a recent net loss and a dividend not well covered by earnings, Entain's online growth guidance remains strong at approximately 7% for 2025.

- Our growth report here indicates Entain may be poised for an improving outlook.

- Click here and access our complete balance sheet health report to understand the dynamics of Entain.

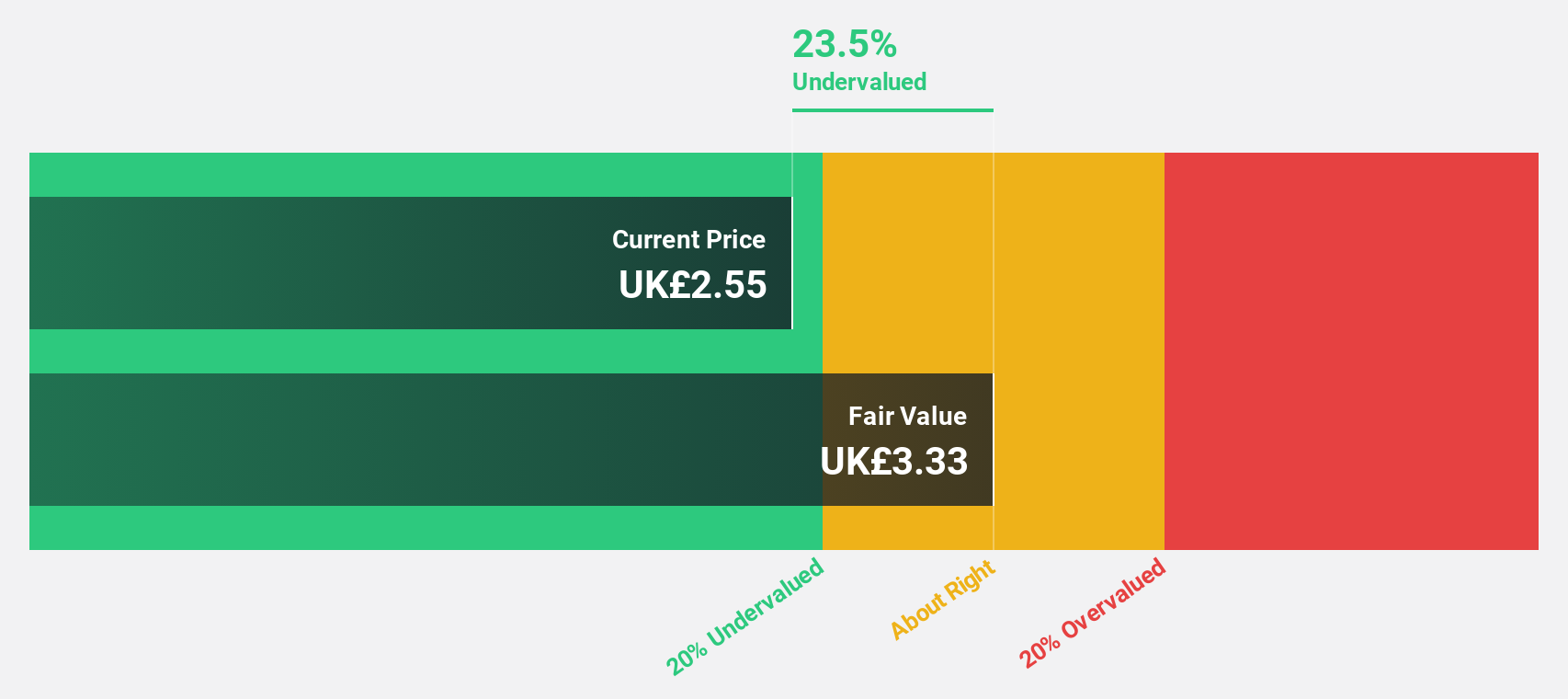

M&G (LSE:MNG)

Overview: M&G plc operates through its subsidiaries to provide savings and investment services in the United Kingdom and internationally, with a market cap of approximately £6.45 billion.

Operations: The company's revenue is primarily derived from its Asset Management segment, which generated £1.07 billion, and the Life (Including Wealth) segment, which contributed £7.57 billion.

Estimated Discount To Fair Value: 25.6%

M&G is trading at £2.72, which is 25.6% below its estimated fair value of £3.66, highlighting potential undervaluation based on cash flows. The company reported a net income of £243 million for H1 2025, reversing a loss from the previous year, and earnings are projected to grow by 34.72% annually over the next three years as profitability improves. However, revenue is expected to decline significantly and dividends remain not well covered by earnings despite recent increases.

- The growth report we've compiled suggests that M&G's future prospects could be on the up.

- Take a closer look at M&G's balance sheet health here in our report.

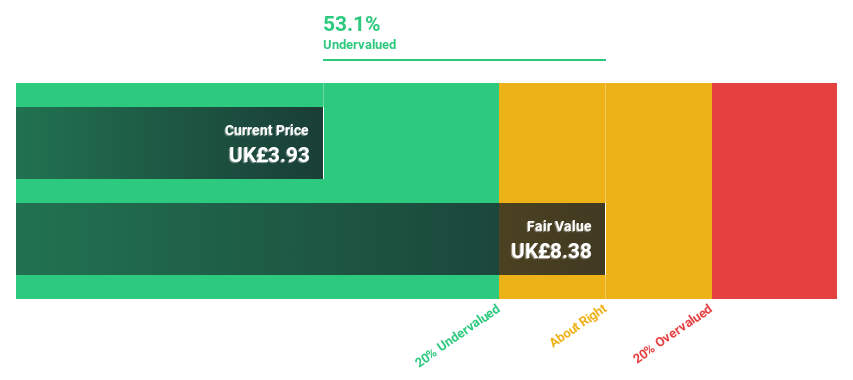

QinetiQ Group (LSE:QQ.)

Overview: QinetiQ Group plc offers science and technology solutions in the defense, security, and infrastructure sectors across the UK, US, Australia, and internationally with a market cap of £2.47 billion.

Operations: The company's revenue is derived from two main segments: EMEA Services, contributing £1.48 billion, and Global Solutions, generating £453.90 million.

Estimated Discount To Fair Value: 20.9%

QinetiQ Group is trading at £4.61, about 20.9% below its estimated fair value of £5.83, indicating potential undervaluation based on cash flows. The company is expected to experience revenue growth of 4.7% annually, outpacing the UK market average of 4.2%. Earnings are projected to grow significantly at 67.71% per year over the next three years, with profitability anticipated during this period, supported by a high forecasted return on equity of 27.5%.

- Our comprehensive growth report raises the possibility that QinetiQ Group is poised for substantial financial growth.

- Get an in-depth perspective on QinetiQ Group's balance sheet by reading our health report here.

Turning Ideas Into Actions

- Navigate through the entire inventory of 50 Undervalued UK Stocks Based On Cash Flows here.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Entain might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About LSE:ENT

Entain

Operates as a sports-betting and gaming company in the United Kingdom, Ireland, Italy, rest of Europe, Australia, New Zealand, and internationally.

Undervalued with high growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|5.2% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|24.9% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.3% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|64.5% undervalued

DA

Community Contributor