- United Kingdom

- /

- Hospitality

- /

- LSE:CPG

With EPS Growth And More, Compass Group (LON:CPG) Makes An Interesting Case

For beginners, it can seem like a good idea (and an exciting prospect) to buy a company that tells a good story to investors, even if it currently lacks a track record of revenue and profit. Sometimes these stories can cloud the minds of investors, leading them to invest with their emotions rather than on the merit of good company fundamentals. Loss making companies can act like a sponge for capital - so investors should be cautious that they're not throwing good money after bad.

If this kind of company isn't your style, you like companies that generate revenue, and even earn profits, then you may well be interested in Compass Group (LON:CPG). While profit isn't the sole metric that should be considered when investing, it's worth recognising businesses that can consistently produce it.

See our latest analysis for Compass Group

Compass Group's Improving Profits

Even modest earnings per share growth (EPS) can create meaningful value, when it is sustained reliably from year to year. So EPS growth can certainly encourage an investor to take note of a stock. Outstandingly, Compass Group's EPS shot from UK£0.41 to UK£0.74, over the last year. Year on year growth of 79% is certainly a sight to behold. The best case scenario? That the business has hit a true inflection point.

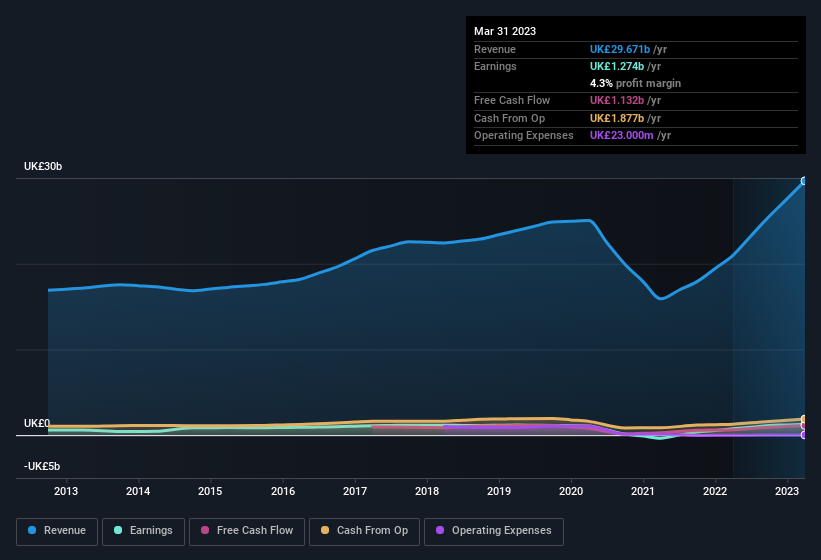

Careful consideration of revenue growth and earnings before interest and taxation (EBIT) margins can help inform a view on the sustainability of the recent profit growth. While we note Compass Group achieved similar EBIT margins to last year, revenue grew by a solid 41% to UK£30b. That's encouraging news for the company!

The chart below shows how the company's bottom and top lines have progressed over time. For finer detail, click on the image.

Fortunately, we've got access to analyst forecasts of Compass Group's future profits. You can do your own forecasts without looking, or you can take a peek at what the professionals are predicting.

Are Compass Group Insiders Aligned With All Shareholders?

Insider interest in a company always sparks a bit of intrigue and many investors are on the lookout for companies where insiders are putting their money where their mouth is. That's because insider buying often indicates that those closest to the company have confidence that the share price will perform well. Of course, we can never be sure what insiders are thinking, we can only judge their actions.

Compass Group insiders both bought and sold shares over the last twelve months, but they did end up spending UK£27k more on stock than they received from selling it. So, on balance, the insider transactions are mildly encouraging. We also note that it was the Group CFO & Director, Charles Brown, who made the biggest single acquisition, paying UK£53k for shares at about UK£18.80 each.

Along with the insider buying, another encouraging sign for Compass Group is that insiders, as a group, have a considerable shareholding. Indeed, they hold UK£16m worth of its stock. That's a lot of money, and no small incentive to work hard. Even though that's only about 0.05% of the company, it's enough money to indicate alignment between the leaders of the business and ordinary shareholders.

While insiders are apparently happy to hold and accumulate shares, that is just part of the big picture. That's because on our analysis the CEO, Dominic Blakemore, is paid less than the median for similar sized companies. For companies with market capitalisations over UK£6.3b, like Compass Group, the median CEO pay is around UK£4.1m.

Compass Group's CEO took home a total compensation package worth UK£3.3m in the year leading up to September 2022. That seems pretty reasonable, especially given it's below the median for similar sized companies. CEO compensation is hardly the most important aspect of a company to consider, but when it's reasonable, that gives a little more confidence that leadership are looking out for shareholder interests. It can also be a sign of good governance, more generally.

Is Compass Group Worth Keeping An Eye On?

Compass Group's earnings per share have been soaring, with growth rates sky high. To make matters even better, the company insiders who know the company best have put their faith in the its future and have been buying more stock. These factors seem to indicate the company's potential and that it has reached an inflection point. We'd suggest Compass Group belongs near the top of your watchlist. Still, you should learn about the 1 warning sign we've spotted with Compass Group.

The good news is that Compass Group is not the only growth stock with insider buying. Here's a list of them... with insider buying in the last three months!

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About LSE:CPG

Compass Group

Operates as a food and support services company in North America, Europe, and internationally.

Reasonable growth potential with adequate balance sheet.