Advertisement

- United Kingdom

- /

- Professional Services

- /

- AIM:TEK

What Can We Conclude About Tekcapital's (LON:TEK) CEO Pay?

Cliff Gross is the CEO of Tekcapital plc (LON:TEK), and in this article, we analyze the executive's compensation package with respect to the overall performance of the company. This analysis will also evaluate the appropriateness of CEO compensation when taking into account the earnings and shareholder returns of the company.

Check out our latest analysis for Tekcapital

Comparing Tekcapital plc's CEO Compensation With the industry

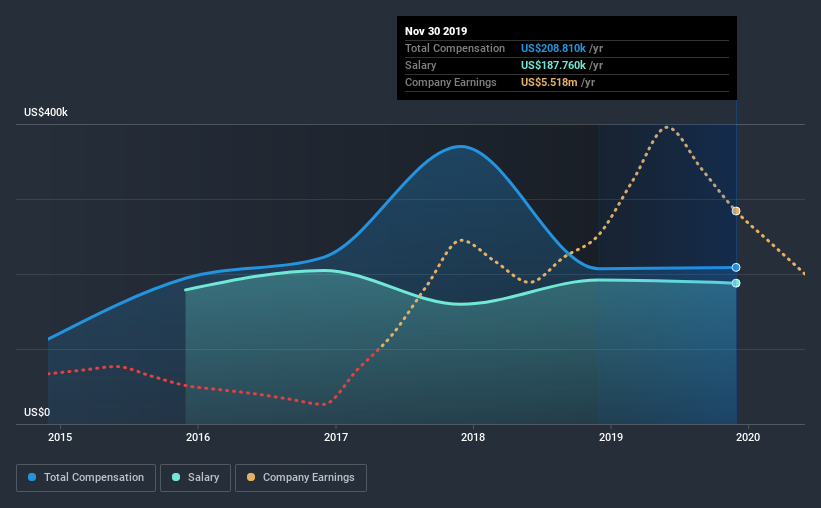

At the time of writing, our data shows that Tekcapital plc has a market capitalization of UK£7.7m, and reported total annual CEO compensation of US$209k for the year to November 2019. That is, the compensation was roughly the same as last year. In particular, the salary of US$187.8k, makes up a huge portion of the total compensation being paid to the CEO.

On comparing similar-sized companies in the industry with market capitalizations below UK£152m, we found that the median total CEO compensation was US$404k. This suggests that Cliff Gross is paid below the industry median. Moreover, Cliff Gross also holds UK£758k worth of Tekcapital stock directly under their own name, which reveals to us that they have a significant personal stake in the company.

| Component | 2019 | 2018 | Proportion (2019) |

| Salary | US$188k | US$192k | 90% |

| Other | US$21k | US$15k | 10% |

| Total Compensation | US$209k | US$207k | 100% |

Speaking on an industry level, nearly 74% of total compensation represents salary, while the remainder of 26% is other remuneration. According to our research, Tekcapital has allocated a higher percentage of pay to salary in comparison to the wider industry. If salary is the major component in total compensation, it suggests that the CEO receives a higher fixed proportion of the total compensation, regardless of performance.

A Look at Tekcapital plc's Growth Numbers

Tekcapital plc has seen its earnings per share (EPS) increase by 45% a year over the past three years. Its revenue is down 53% over the previous year.

Shareholders would be glad to know that the company has improved itself over the last few years. It's always a tough situation when revenues are not growing, but ultimately profits are more important. While we don't have analyst forecasts for the company, shareholders might want to examine this detailed historical graph of earnings, revenue and cash flow.

Has Tekcapital plc Been A Good Investment?

With a three year total loss of 71% for the shareholders, Tekcapital plc would certainly have some dissatisfied shareholders. Therefore, it might be upsetting for shareholders if the CEO were paid generously.

To Conclude...

As previously discussed, Cliff is compensated less than what is normal for CEOs of companies of similar size, and which belong to the same industry. However, the EPS growth over three years is certainly impressive. Considering EPS are on the up, we would say Cliff is compensated fairly. But we believe shareholders would want to see healthier returns before the CEO gets a raise.

It is always advisable to analyse CEO pay, along with performing a thorough analysis of the company's key performance areas. We identified 4 warning signs for Tekcapital (1 doesn't sit too well with us!) that you should be aware of before investing here.

Switching gears from Tekcapital, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

If you’re looking to trade Tekcapital, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Tekcapital might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About AIM:TEK

Tekcapital

Provides technology transfer services to universities and corporate clients in the United Kingdom and the United States.

Flawless balance sheet with slight risk.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|5.2% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|24.9% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.3% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|64.5% undervalued

DA

Community Contributor