- United Kingdom

- /

- Other Utilities

- /

- LSE:TEP

Uncovering Cohort And 2 Hidden Small Cap Gems In The UK Market

Reviewed by Simply Wall St

As the UK market grapples with global economic challenges, including weak trade data from China impacting major indices like the FTSE 100 and FTSE 250, investors are increasingly turning their attention to small-cap stocks that may offer untapped potential. In this environment, identifying promising companies requires a keen eye for those with robust fundamentals and resilience amidst broader market volatility.

Top 10 Undiscovered Gems With Strong Fundamentals In The United Kingdom

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| M&G Credit Income Investment Trust | NA | 17.28% | 15.80% | ★★★★★★ |

| London Security | 0.22% | 10.13% | 7.75% | ★★★★★★ |

| Andrews Sykes Group | NA | 2.15% | 4.93% | ★★★★★★ |

| B.P. Marsh & Partners | NA | 29.42% | 31.34% | ★★★★★★ |

| Impellam Group | 31.12% | -5.43% | -6.86% | ★★★★★★ |

| VH Global Sustainable Energy Opportunities | NA | 18.30% | 20.03% | ★★★★★★ |

| Rights and Issues Investment Trust | NA | -3.68% | -4.07% | ★★★★★★ |

| FW Thorpe | 5.89% | 11.97% | 12.07% | ★★★★★☆ |

| BBGI Global Infrastructure | 0.02% | 3.08% | 6.85% | ★★★★★☆ |

| Goodwin | 52.21% | 9.26% | 13.12% | ★★★★★☆ |

Let's dive into some prime choices out of from the screener.

Cohort (AIM:CHRT)

Simply Wall St Value Rating: ★★★★★★

Overview: Cohort plc is a company that offers a range of products and services in the defense and security sectors across multiple regions including the United Kingdom, Germany, Portugal, Africa, North and South America, the Asia Pacific, and other European countries with a market cap of £417.11 million.

Operations: Revenue primarily comes from two segments: Sensors and Effectors (£120.49 million) and Communications and Intelligence (£83.38 million).

Cohort, a player in the Aerospace & Defense sector, has demonstrated solid financial health with earnings growing at 16.3% annually over the past five years. Its debt-to-equity ratio improved from 32.5% to 29.2%, indicating prudent financial management. Recently, Cohort completed a follow-on equity offering worth £40 million at £8.75 per share, suggesting strategic capital raising efforts for future growth initiatives. The company's interest payments are comfortably covered by EBIT at 17.5 times coverage, reflecting strong operational profitability and high-quality earnings that bolster investor confidence in its ongoing performance and potential value appreciation.

- Unlock comprehensive insights into our analysis of Cohort stock in this health report.

Review our historical performance report to gain insights into Cohort's's past performance.

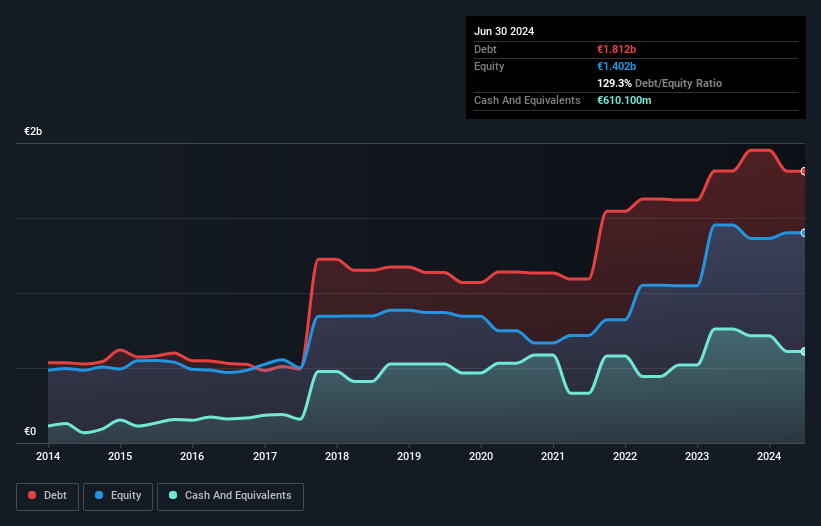

RHI Magnesita (LSE:RHIM)

Simply Wall St Value Rating: ★★★★★☆

Overview: RHI Magnesita N.V., along with its subsidiaries, is engaged in the development, production, sale, installation, and maintenance of refractory products and systems for industrial high-temperature processes globally, with a market capitalization of £1.46 billion.

Operations: RHI Magnesita generates revenue primarily from its Steel segment, which contributes €2.44 billion. The company has a market capitalization of £1.46 billion.

RHI Magnesita, a player in the Basic Materials sector, showcases promising figures with its earnings surging by 33% over the past year, outpacing industry trends. Trading at 54% below its estimated fair value, it seems an attractive proposition compared to peers. Despite a high net debt to equity ratio of 86%, interest payments are well-covered by EBIT at 6.3 times coverage. The company appears to be on solid ground with positive free cash flow and a slight reduction in its debt-equity ratio from 131% to 129% over five years. Future earnings growth is forecasted at around 12% annually.

- Get an in-depth perspective on RHI Magnesita's performance by reading our health report here.

Understand RHI Magnesita's track record by examining our Past report.

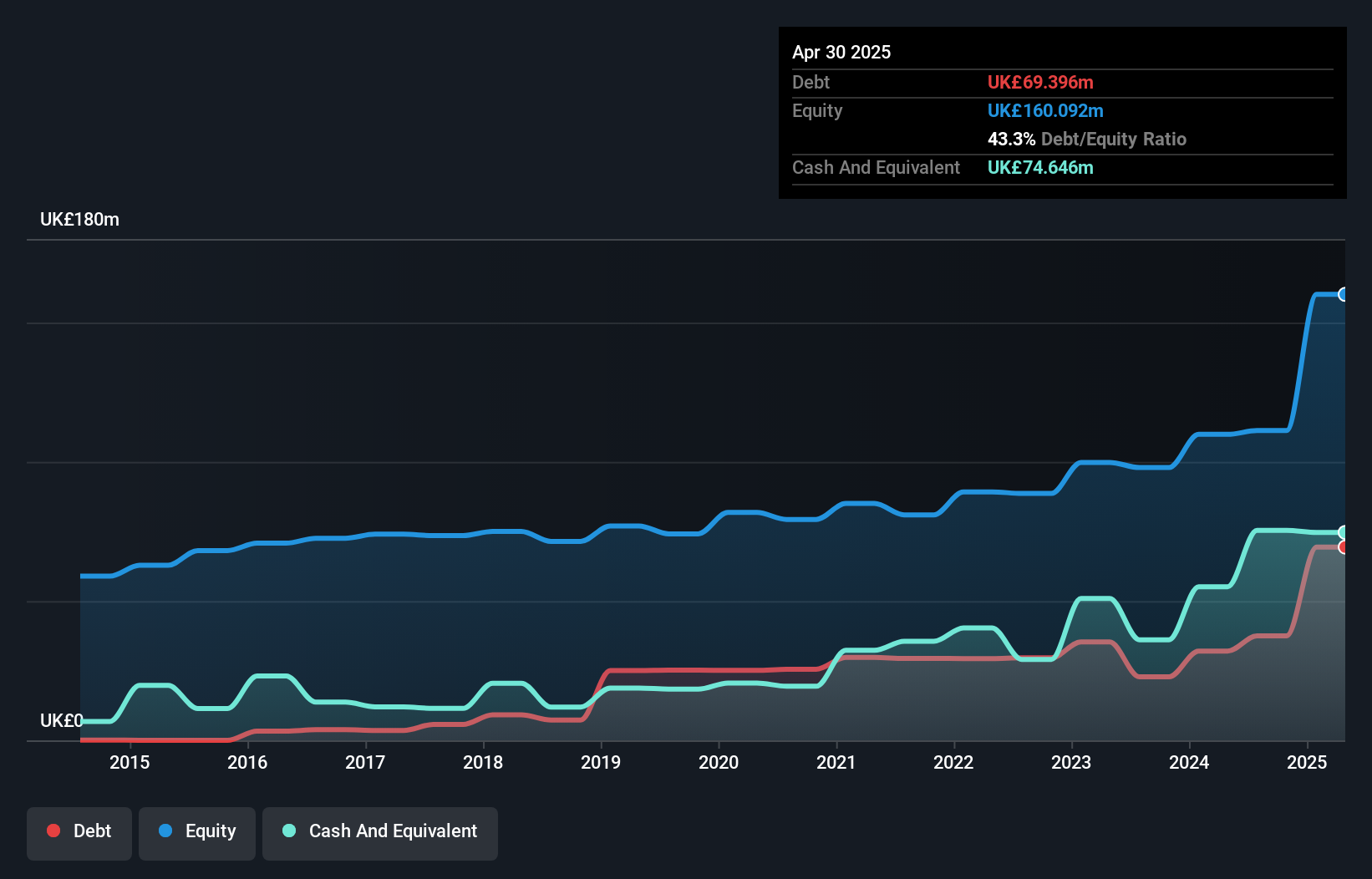

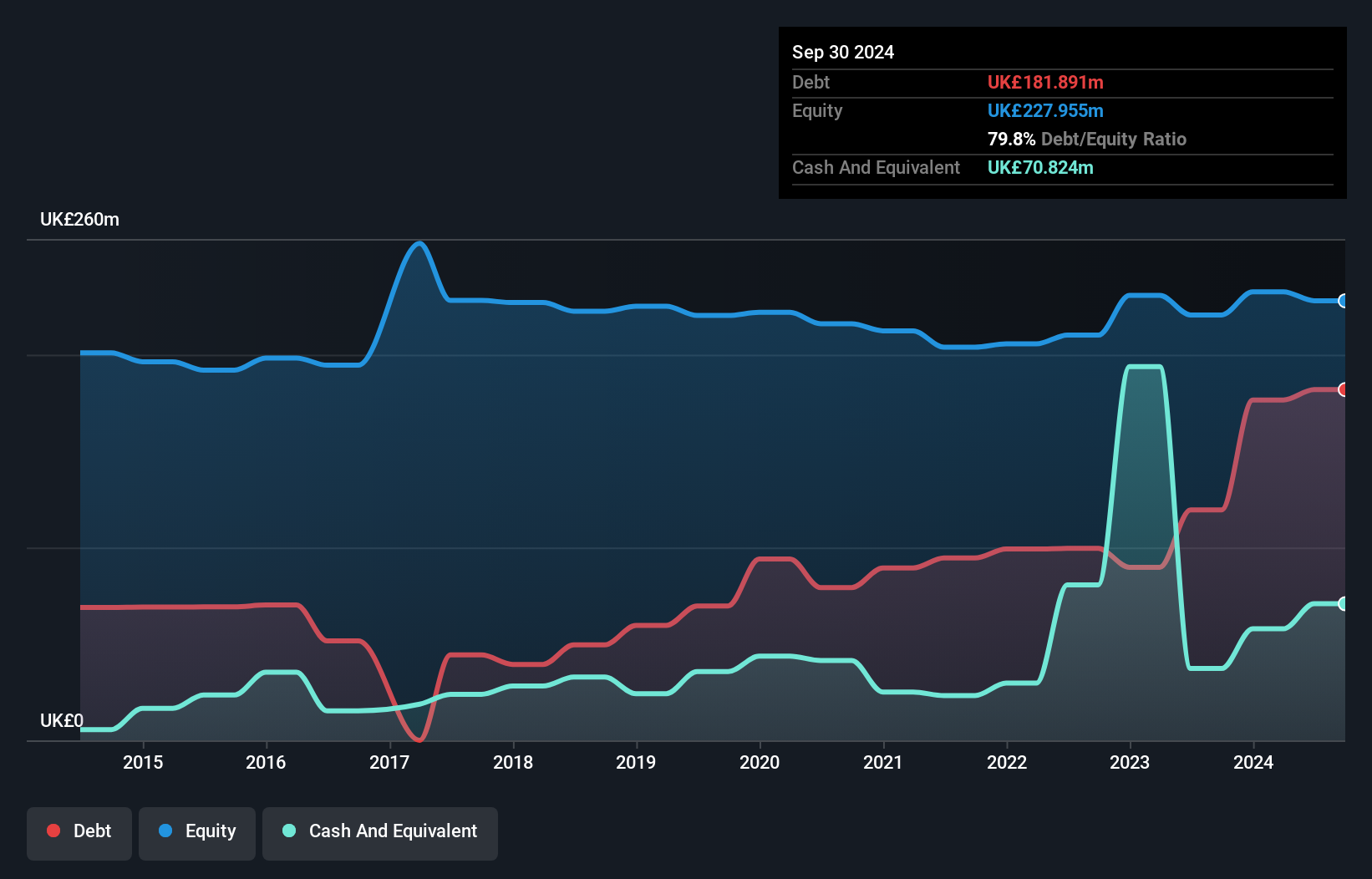

Telecom Plus (LSE:TEP)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Telecom Plus Plc provides utility services in the United Kingdom and has a market capitalization of approximately £1.39 billion.

Operations: Telecom Plus generates revenue primarily from its non-regulated utility segment, amounting to £1.85 billion.

Telecom Plus, a notable player in the UK market, recently reported sales of £697.75 million for the half-year ending September 2024, down from £883.63 million the previous year. Despite this dip in sales, net income rose to £27.63 million from £23.37 million, reflecting improved profitability with basic earnings per share up to £0.351 from £0.295 last year and diluted EPS at £0.348 compared to £0.291 previously. The company trades at 28% below its estimated fair value and enjoys strong debt coverage with EBIT covering interest payments 12 times over, although its debt-to-equity ratio has increased significantly over five years to 79%.

- Delve into the full analysis health report here for a deeper understanding of Telecom Plus.

Gain insights into Telecom Plus' historical performance by reviewing our past performance report.

Seize The Opportunity

- Access the full spectrum of 70 UK Undiscovered Gems With Strong Fundamentals by clicking on this link.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Telecom Plus might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About LSE:TEP

Telecom Plus

Engages in the provision of utility services in the United Kingdom.

Solid track record with adequate balance sheet.