Stock Analysis

- United Kingdom

- /

- Aerospace & Defense

- /

- AIM:CHRT

Exploring Cohort And Two More Undiscovered UK Stocks

Reviewed by Simply Wall St

Amidst a backdrop of fluctuating global markets and cautious investor sentiment, the United Kingdom's financial landscape presents unique opportunities for those looking to explore less charted territories. In this context, understanding the intrinsic qualities that define promising stocks becomes crucial, particularly in sectors less impacted by broader economic shifts.

Top 10 Undiscovered Gems With Strong Fundamentals In The United Kingdom

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Andrews Sykes Group | NA | 1.69% | 3.16% | ★★★★★★ |

| Globaltrans Investment | 15.40% | 2.68% | 16.51% | ★★★★★★ |

| London Security | 0.31% | 9.47% | 7.41% | ★★★★★★ |

| Georgia Capital | NA | -27.80% | 18.94% | ★★★★★★ |

| Impellam Group | 31.12% | -5.43% | -6.86% | ★★★★★★ |

| M&G Credit Income Investment Trust | NA | -0.35% | 1.18% | ★★★★★★ |

| Fix Price Group | 43.59% | 12.53% | 23.49% | ★★★★★☆ |

| Ros Agro | 57.18% | 17.80% | 18.35% | ★★★★★☆ |

| BBGI Global Infrastructure | 0.02% | 6.58% | 9.90% | ★★★★★☆ |

| Mountview Estates | 16.64% | 4.50% | -0.59% | ★★★★☆☆ |

Here we highlight a subset of our preferred stocks from the screener.

Cohort (AIM:CHRT)

Simply Wall St Value Rating: ★★★★★☆

Overview: Cohort plc is a diversified company that operates in the defense and security sectors, offering a range of products and services across multiple global regions, with a market capitalization of £337.98 million.

Operations: The company generates revenue through two primary segments: Sensors and Effectors, contributing £103.56 million, and Communications and Intelligence, accounting for £97.09 million. With a gross profit margin of 35.95%, the firm incurs significant costs in operating expenses, which recently totaled £53.80 million, impacting its net income margin of 6.65%.

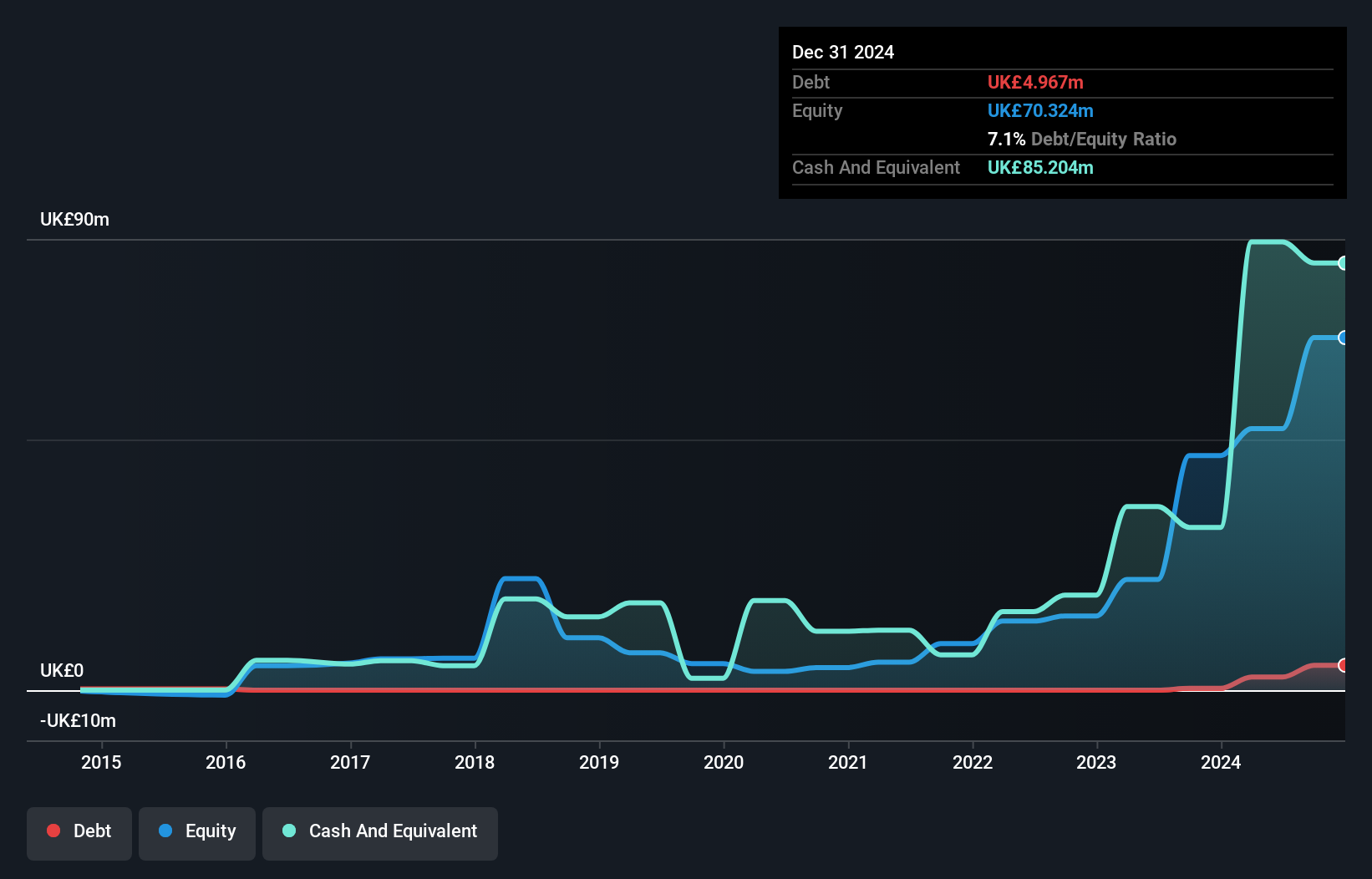

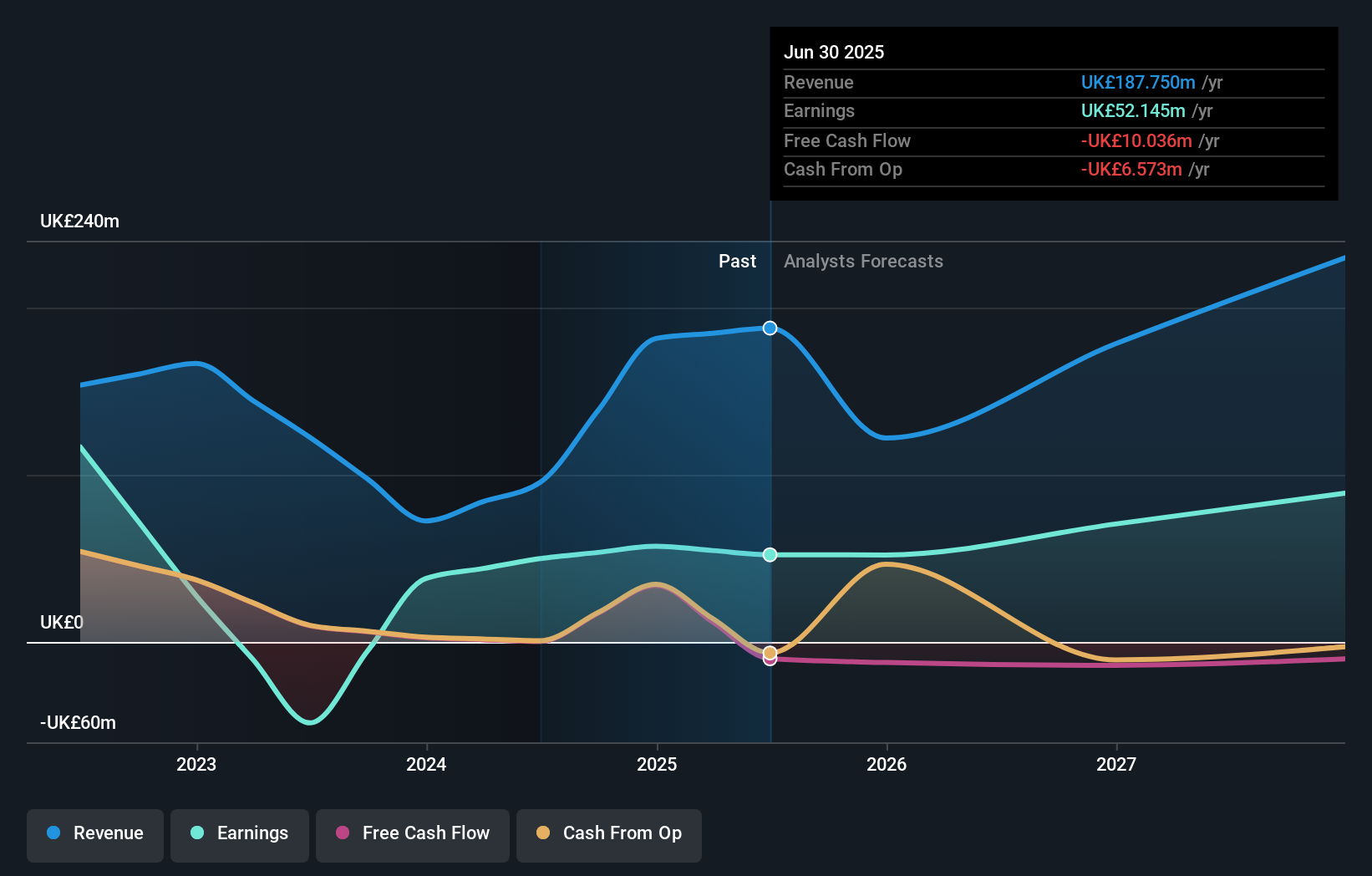

Cohort plc, a lesser-known contender in the UK market, has demonstrated robust financial health and growth potential. With a 20.4% earnings growth outpacing its industry's 16.7%, Cohort also reported a significant year-over-year net income increase to £15.32 million from £11.36 million. The firm's strategic moves include securing a €33 million contract with NATO, underscoring its competitive edge and operational capabilities. Additionally, the company maintains more cash than total debt, ensuring financial stability while forecasting future earnings growth at 12.68% annually.

- Click here and access our complete health analysis report to understand the dynamics of Cohort.

Review our historical performance report to gain insights into Cohort's's past performance.

Cohort (AIM:CHRT)

Simply Wall St Value Rating: ★★★★★☆

Overview: Cohort plc is a diversified company that operates in the defense and security sectors, offering a range of products and services across multiple global regions, with a market capitalization of £337.98 million.

Operations: The company generates revenue through two primary segments: Sensors and Effectors, contributing £103.56 million, and Communications and Intelligence, accounting for £97.09 million. With a gross profit margin of 35.95%, the firm incurs significant costs in operating expenses, which recently totaled £53.80 million, impacting its net income margin of 6.65%.

Cohort plc, a lesser-known contender in the UK market, has demonstrated robust financial health and growth potential. With a 20.4% earnings growth outpacing its industry's 16.7%, Cohort also reported a significant year-over-year net income increase to £15.32 million from £11.36 million. The firm's strategic moves include securing a €33 million contract with NATO, underscoring its competitive edge and operational capabilities. Additionally, the company maintains more cash than total debt, ensuring financial stability while forecasting future earnings growth at 12.68% annually.

- Click here and access our complete health analysis report to understand the dynamics of Cohort.

Review our historical performance report to gain insights into Cohort's's past performance.

Yü Group (AIM:YU.)

Simply Wall St Value Rating: ★★★★★☆

Overview: Yü Group PLC is a UK-based company that primarily supplies energy and utility solutions, with a market capitalization of £313.87 million.

Operations: The primary revenue generator for this company is its retail segment, contributing £459.80 million, complemented by smaller earnings from smart technologies and metering assets. Over recent periods, the firm has experienced a notable increase in gross profit margin, rising to 18.05% by the end of 2023 from earlier figures around 7.86%.

Yü Group, a notable player in the renewable energy sector, has demonstrated robust financial and operational growth. Over the past year, earnings surged by 547.1%, significantly outpacing the industry's decline of 15.5%. With a positive free cash flow and high-quality earnings, Yü stands out as trading 63.4% below its estimated fair value. Additionally, its debt-to-equity ratio modestly increased to 0.8 over five years while maintaining more cash than total debt, underscoring strong financial health amidst a volatile share price.

- Click to explore a detailed breakdown of our findings in Yü Group's health report.

Explore historical data to track Yü Group's performance over time in our Past section.

Yü Group (AIM:YU.)

Simply Wall St Value Rating: ★★★★★☆

Overview: Yü Group PLC is a UK-based company that primarily supplies energy and utility solutions, with a market capitalization of £313.87 million.

Operations: The primary revenue generator for this company is its retail segment, contributing £459.80 million, complemented by smaller earnings from smart technologies and metering assets. Over recent periods, the firm has experienced a notable increase in gross profit margin, rising to 18.05% by the end of 2023 from earlier figures around 7.86%.

Yü Group, a notable player in the renewable energy sector, has demonstrated robust financial and operational growth. Over the past year, earnings surged by 547.1%, significantly outpacing the industry's decline of 15.5%. With a positive free cash flow and high-quality earnings, Yü stands out as trading 63.4% below its estimated fair value. Additionally, its debt-to-equity ratio modestly increased to 0.8 over five years while maintaining more cash than total debt, underscoring strong financial health amidst a volatile share price.

- Click to explore a detailed breakdown of our findings in Yü Group's health report.

Explore historical data to track Yü Group's performance over time in our Past section.

Harworth Group (LSE:HWG)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Harworth Group plc is a land and property regeneration company focused on developing and optimising assets primarily in the North of England and the Midlands, with a market capitalization of £566.91 million.

Operations: The company generates revenue primarily through income generation, capital growth from other property activities, and the sale of development properties. It has consistently reported a gross profit margin of 100% in multiple fiscal quarters, reflecting its effective cost management relative to revenue generation.

Harworth Group, a UK-based property regeneration company, is making significant strides in the real estate sector. With a net debt to equity ratio of 5.7%, the firm maintains a solid financial structure. It's outpacing industry growth with earnings up by 36.3% from last year, significantly higher than the industry's -6.1%. Recent strategic moves include securing planning for a major logistics hub in Leeds, expected to generate £190 million in value and appointing Gareth Thomas as development director to boost its Midlands operations.

- Delve into the full analysis health report here for a deeper understanding of Harworth Group.

Gain insights into Harworth Group's historical performance by reviewing our past performance report.

Harworth Group (LSE:HWG)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Harworth Group plc is a land and property regeneration company focused on developing and optimising assets primarily in the North of England and the Midlands, with a market capitalization of £566.91 million.

Operations: The company generates revenue primarily through income generation, capital growth from other property activities, and the sale of development properties. It has consistently reported a gross profit margin of 100% in multiple fiscal quarters, reflecting its effective cost management relative to revenue generation.

Harworth Group, a UK-based property regeneration company, is making significant strides in the real estate sector. With a net debt to equity ratio of 5.7%, the firm maintains a solid financial structure. It's outpacing industry growth with earnings up by 36.3% from last year, significantly higher than the industry's -6.1%. Recent strategic moves include securing planning for a major logistics hub in Leeds, expected to generate £190 million in value and appointing Gareth Thomas as development director to boost its Midlands operations.

- Delve into the full analysis health report here for a deeper understanding of Harworth Group.

Gain insights into Harworth Group's historical performance by reviewing our past performance report.

Taking Advantage

- Delve into our full catalog of 78 UK Undiscovered Gems With Strong Fundamentals here.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're helping make it simple.

Find out whether Cohort is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About AIM:CHRT

Cohort

Through its subsidiaries, provides various products and services in defense, security, and related markets in the United Kingdom, Germany, Portugal, Africa, North and South America, and the Asia Pacific and Africa.

Excellent balance sheet with proven track record and pays a dividend.