Advertisement

- United Kingdom

- /

- Auto Components

- /

- AIM:AURR

Aurrigo International plc (LON:AURR) May Have Run Too Fast Too Soon With Recent 47% Price Plummet

Aurrigo International plc (LON:AURR) shareholders won't be pleased to see that the share price has had a very rough month, dropping 47% and undoing the prior period's positive performance. Instead of being rewarded, shareholders who have already held through the last twelve months are now sitting on a 35% share price drop.

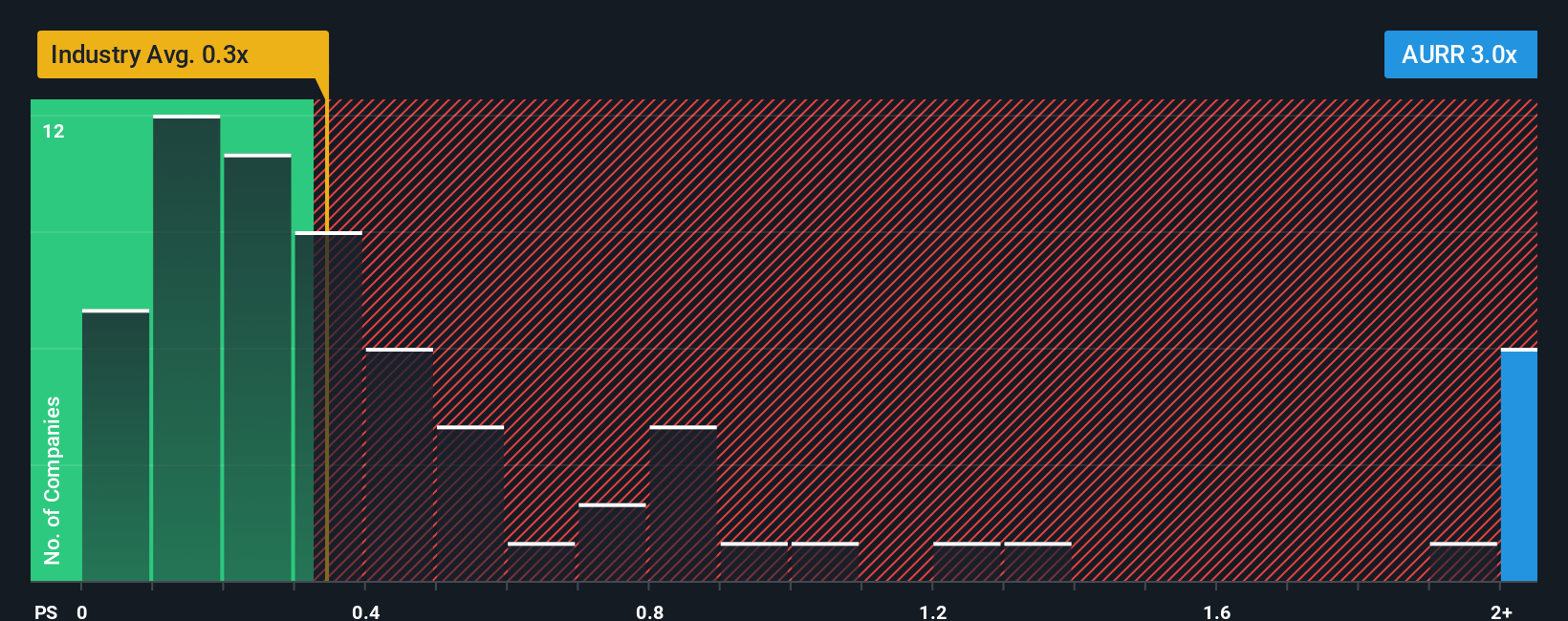

Even after such a large drop in price, when almost half of the companies in the United Kingdom's Auto Components industry have price-to-sales ratios (or "P/S") below 1.6x, you may still consider Aurrigo International as a stock probably not worth researching with its 3x P/S ratio. However, the P/S might be high for a reason and it requires further investigation to determine if it's justified.

See our latest analysis for Aurrigo International

How Aurrigo International Has Been Performing

Recent times have been pleasing for Aurrigo International as its revenue has risen in spite of the industry's average revenue going into reverse. The P/S ratio is probably high because investors think the company will continue to navigate the broader industry headwinds better than most. However, if this isn't the case, investors might get caught out paying too much for the stock.

Keen to find out how analysts think Aurrigo International's future stacks up against the industry? In that case, our free report is a great place to start.Is There Enough Revenue Growth Forecasted For Aurrigo International?

There's an inherent assumption that a company should outperform the industry for P/S ratios like Aurrigo International's to be considered reasonable.

Retrospectively, the last year delivered an exceptional 34% gain to the company's top line. The latest three year period has also seen an excellent 68% overall rise in revenue, aided by its short-term performance. So we can start by confirming that the company has done a great job of growing revenue over that time.

Shifting to the future, estimates from the lone analyst covering the company suggest revenue growth is heading into negative territory, declining 15% over the next year. With the industry predicted to deliver 2.4% growth, that's a disappointing outcome.

In light of this, it's alarming that Aurrigo International's P/S sits above the majority of other companies. Apparently many investors in the company reject the analyst cohort's pessimism and aren't willing to let go of their stock at any price. Only the boldest would assume these prices are sustainable as these declining revenues are likely to weigh heavily on the share price eventually.

The Bottom Line On Aurrigo International's P/S

Aurrigo International's P/S remain high even after its stock plunged. It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

We've established that Aurrigo International currently trades on a much higher than expected P/S for a company whose revenues are forecast to decline. In cases like this where we see revenue decline on the horizon, we suspect the share price is at risk of following suit, bringing back the high P/S into the realms of suitability. At these price levels, investors should remain cautious, particularly if things don't improve.

Before you take the next step, you should know about the 5 warning signs for Aurrigo International (3 are significant!) that we have uncovered.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About AIM:AURR

Aurrigo International

Offers electrical components to the automotive and aviation industry in the United Kingdom, Europe, and internationally.

Excellent balance sheet with slight risk.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor