Our Take On The Returns On Capital At Financière de l'Odet (EPA:ODET)

What trends should we look for it we want to identify stocks that can multiply in value over the long term? Amongst other things, we'll want to see two things; firstly, a growing return on capital employed (ROCE) and secondly, an expansion in the company's amount of capital employed. Put simply, these types of businesses are compounding machines, meaning they are continually reinvesting their earnings at ever-higher rates of return. Although, when we looked at Financière de l'Odet (EPA:ODET), it didn't seem to tick all of these boxes.

Understanding Return On Capital Employed (ROCE)

For those that aren't sure what ROCE is, it measures the amount of pre-tax profits a company can generate from the capital employed in its business. The formula for this calculation on Financière de l'Odet is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

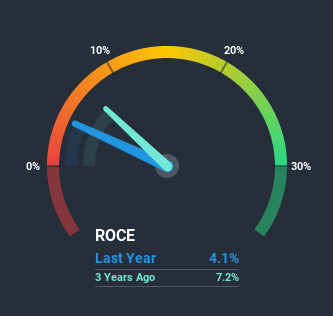

0.041 = €1.6b ÷ (€56b - €16b) (Based on the trailing twelve months to December 2020).

So, Financière de l'Odet has an ROCE of 4.1%. Ultimately, that's a low return and it under-performs the Logistics industry average of 8.7%.

See our latest analysis for Financière de l'Odet

Historical performance is a great place to start when researching a stock so above you can see the gauge for Financière de l'Odet's ROCE against it's prior returns. If you're interested in investigating Financière de l'Odet's past further, check out this free graph of past earnings, revenue and cash flow.

What Can We Tell From Financière de l'Odet's ROCE Trend?

On the surface, the trend of ROCE at Financière de l'Odet doesn't inspire confidence. Over the last five years, returns on capital have decreased to 4.1% from 6.7% five years ago. However it looks like Financière de l'Odet might be reinvesting for long term growth because while capital employed has increased, the company's sales haven't changed much in the last 12 months. It's worth keeping an eye on the company's earnings from here on to see if these investments do end up contributing to the bottom line.

On a related note, Financière de l'Odet has decreased its current liabilities to 29% of total assets. That could partly explain why the ROCE has dropped. What's more, this can reduce some aspects of risk to the business because now the company's suppliers or short-term creditors are funding less of its operations. Some would claim this reduces the business' efficiency at generating ROCE since it is now funding more of the operations with its own money.

In Conclusion...

To conclude, we've found that Financière de l'Odet is reinvesting in the business, but returns have been falling. And with the stock having returned a mere 23% in the last five years to shareholders, you could argue that they're aware of these lackluster trends. So if you're looking for a multi-bagger, the underlying trends indicate you may have better chances elsewhere.

Financière de l'Odet does come with some risks though, we found 4 warning signs in our investment analysis, and 1 of those doesn't sit too well with us...

For those who like to invest in solid companies, check out this free list of companies with solid balance sheets and high returns on equity.

If you decide to trade Financière de l'Odet, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About ENXTPA:ODET

Compagnie de l'Odet

Operates transportation and logistics, communication, and industry business in France, Africa, the Americas, the Asia-Pacific, and other European countries.

Flawless balance sheet and good value.