Advertisement

- Finland

- /

- Electronic Equipment and Components

- /

- HLSE:VAIAS

Shareholders Are Optimistic That Vaisala Oyj (HEL:VAIAS) Will Multiply In Value

If you're not sure where to start when looking for the next multi-bagger, there are a few key trends you should keep an eye out for. Firstly, we'll want to see a proven return on capital employed (ROCE) that is increasing, and secondly, an expanding base of capital employed. If you see this, it typically means it's a company with a great business model and plenty of profitable reinvestment opportunities. So, when we ran our eye over Vaisala Oyj's (HEL:VAIAS) trend of ROCE, we really liked what we saw.

Return On Capital Employed (ROCE): What Is It?

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. To calculate this metric for Vaisala Oyj, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

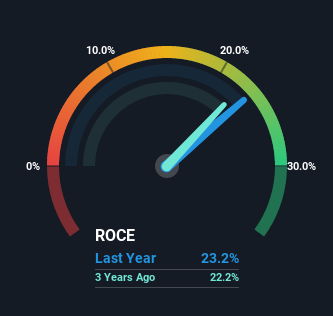

0.23 = €58m ÷ (€443m - €193m) (Based on the trailing twelve months to March 2023).

Therefore, Vaisala Oyj has an ROCE of 23%. That's a fantastic return and not only that, it outpaces the average of 17% earned by companies in a similar industry.

See our latest analysis for Vaisala Oyj

In the above chart we have measured Vaisala Oyj's prior ROCE against its prior performance, but the future is arguably more important. If you'd like to see what analysts are forecasting going forward, you should check out our free report for Vaisala Oyj.

SWOT Analysis for Vaisala Oyj

Strength

- Debt is not viewed as a risk.

- Dividends are covered by earnings and cash flows.

Weakness

- Earnings declined over the past year.

- Dividend is low compared to the top 25% of dividend payers in the Electronic market.

- Expensive based on P/E ratio and estimated fair value.

Opportunity

- Annual earnings are forecast to grow faster than the Finnish market.

Threat

- Revenue is forecast to grow slower than 20% per year.

What Does the ROCE Trend For Vaisala Oyj Tell Us?

We'd be pretty happy with returns on capital like Vaisala Oyj. Over the past five years, ROCE has remained relatively flat at around 23% and the business has deployed 27% more capital into its operations. Now considering ROCE is an attractive 23%, this combination is actually pretty appealing because it means the business can consistently put money to work and generate these high returns. You'll see this when looking at well operated businesses or favorable business models.

On another note, while the change in ROCE trend might not scream for attention, it's interesting that the current liabilities have actually gone up over the last five years. This is intriguing because if current liabilities hadn't increased to 43% of total assets, this reported ROCE would probably be less than23% because total capital employed would be higher.The 23% ROCE could be even lower if current liabilities weren't 43% of total assets, because the the formula would show a larger base of total capital employed. So with current liabilities at such high levels, this effectively means the likes of suppliers or short-term creditors are funding a meaningful part of the business, which in some instances can bring some risks.

The Key Takeaway

In short, we'd argue Vaisala Oyj has the makings of a multi-bagger since its been able to compound its capital at very profitable rates of return. On top of that, the stock has rewarded shareholders with a remarkable 122% return to those who've held over the last five years. So while the positive underlying trends may be accounted for by investors, we still think this stock is worth looking into further.

Before jumping to any conclusions though, we need to know what value we're getting for the current share price. That's where you can check out our FREE intrinsic value estimation that compares the share price and estimated value.

If you'd like to see other companies earning high returns, check out our free list of companies earning high returns with solid balance sheets here.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About HLSE:VAIAS

Vaisala Oyj

Provides weather, environmental, and industrial measurement solutions and services for weather-related and industrial markets.

Outstanding track record with excellent balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor