- Finland

- /

- Healthcare Services

- /

- HLSE:OKDBV

Oriola Oyj Just Missed Earnings - But Analysts Have Updated Their Models

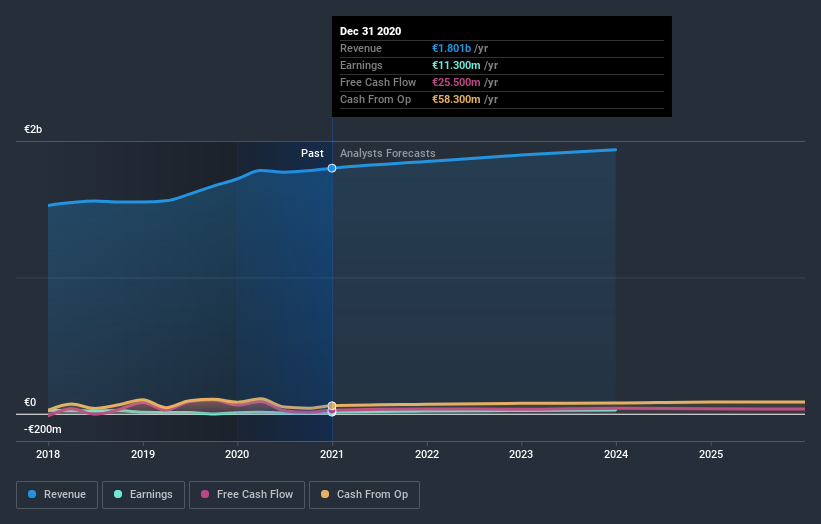

Oriola Oyj (HEL:OKDBV) shareholders are probably feeling a little disappointed, since its shares fell 4.4% to €1.95 in the week after its latest yearly results. It looks like the results were a bit of a negative overall. While revenues of €1.8b were in line with analyst predictions, statutory earnings were less than expected, missing estimates by 7.7% to hit €0.06 per share. Following the result, the analysts have updated their earnings model, and it would be good to know whether they think there's been a strong change in the company's prospects, or if it's business as usual. So we gathered the latest post-earnings forecasts to see what estimates suggest is in store for next year.

See our latest analysis for Oriola Oyj

Taking into account the latest results, the current consensus from Oriola Oyj's three analysts is for revenues of €1.85b in 2021, which would reflect a reasonable 2.7% increase on its sales over the past 12 months. Statutory earnings per share are predicted to shoot up 72% to €0.11. Yet prior to the latest earnings, the analysts had been anticipated revenues of €1.86b and earnings per share (EPS) of €0.13 in 2021. The analysts seem to have become more bearish following the latest results. While there were no changes to revenue forecasts, there was a substantial drop in EPS estimates.

The consensus price target held steady at €2.03, with the analysts seemingly voting that their lower forecast earnings are not expected to lead to a lower stock price in the foreseeable future. The consensus price target is just an average of individual analyst targets, so - it could be handy to see how wide the range of underlying estimates is. Currently, the most bullish analyst values Oriola Oyj at €2.10 per share, while the most bearish prices it at €2.00. Even so, with a relatively close grouping of estimates, it looks like the analysts are quite confident in their valuations, suggesting Oriola Oyj is an easy business to forecast or the the analysts are all using similar assumptions.

Taking a look at the bigger picture now, one of the ways we can understand these forecasts is to see how they compare to both past performance and industry growth estimates. Next year brings more of the same, according to the analysts, with revenue forecast to grow 2.7%, in line with its 2.5% annual growth over the past five years. Compare this with the wider industry (in aggregate), which analyst estimates suggest will see revenues grow 5.9% next year. So it's pretty clear that Oriola Oyj is expected to grow slower than similar companies in the same industry.

The Bottom Line

The biggest concern is that the analysts reduced their earnings per share estimates, suggesting business headwinds could lay ahead for Oriola Oyj. Fortunately, the analysts also reconfirmed their revenue estimates, suggesting sales are tracking in line with expectations - although our data does suggest that Oriola Oyj's revenues are expected to perform worse than the wider industry. There was no real change to the consensus price target, suggesting that the intrinsic value of the business has not undergone any major changes with the latest estimates.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. At Simply Wall St, we have a full range of analyst estimates for Oriola Oyj going out to 2023, and you can see them free on our platform here..

We don't want to rain on the parade too much, but we did also find 1 warning sign for Oriola Oyj that you need to be mindful of.

If you’re looking to trade Oriola Oyj, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About HLSE:OKDBV

Oriola Oyj

Provides healthcare and wellbeing products primarily in Sweden and Finland.

Undervalued with excellent balance sheet.