Stock Analysis

Many Would Be Envious Of KONE Oyj's (HEL:KNEBV) Excellent Returns On Capital

There are a few key trends to look for if we want to identify the next multi-bagger. Firstly, we'll want to see a proven return on capital employed (ROCE) that is increasing, and secondly, an expanding base of capital employed. Ultimately, this demonstrates that it's a business that is reinvesting profits at increasing rates of return. With that in mind, the ROCE of KONE Oyj (HEL:KNEBV) looks attractive right now, so lets see what the trend of returns can tell us.

What is Return On Capital Employed (ROCE)?

If you haven't worked with ROCE before, it measures the 'return' (pre-tax profit) a company generates from capital employed in its business. The formula for this calculation on KONE Oyj is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.39 = €1.4b ÷ (€8.6b - €5.1b) (Based on the trailing twelve months to June 2021).

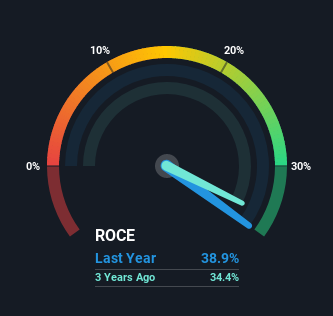

So, KONE Oyj has an ROCE of 39%. That's a fantastic return and not only that, it outpaces the average of 11% earned by companies in a similar industry.

View our latest analysis for KONE Oyj

Above you can see how the current ROCE for KONE Oyj compares to its prior returns on capital, but there's only so much you can tell from the past. If you'd like, you can check out the forecasts from the analysts covering KONE Oyj here for free.

The Trend Of ROCE

KONE Oyj deserves to be commended in regards to it's returns. The company has consistently earned 39% for the last five years, and the capital employed within the business has risen 26% in that time. Returns like this are the envy of most businesses and given it has repeatedly reinvested at these rates, that's even better. If these trends can continue, it wouldn't surprise us if the company became a multi-bagger.

On a separate but related note, it's important to know that KONE Oyj has a current liabilities to total assets ratio of 60%, which we'd consider pretty high. This effectively means that suppliers (or short-term creditors) are funding a large portion of the business, so just be aware that this can introduce some elements of risk. Ideally we'd like to see this reduce as that would mean fewer obligations bearing risks.

The Bottom Line On KONE Oyj's ROCE

KONE Oyj has demonstrated its proficiency by generating high returns on increasing amounts of capital employed, which we're thrilled about. And the stock has followed suit returning a meaningful 65% to shareholders over the last five years. So while the positive underlying trends may be accounted for by investors, we still think this stock is worth looking into further.

Like most companies, KONE Oyj does come with some risks, and we've found 1 warning sign that you should be aware of.

If you want to search for more stocks that have been earning high returns, check out this free list of stocks with solid balance sheets that are also earning high returns on equity.

If you’re looking to trade a wide range of investments, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're helping make it simple.

Find out whether KONE Oyj is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisThis article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About HLSE:KNEBV

Excellent balance sheet with proven track record.