Advertisement

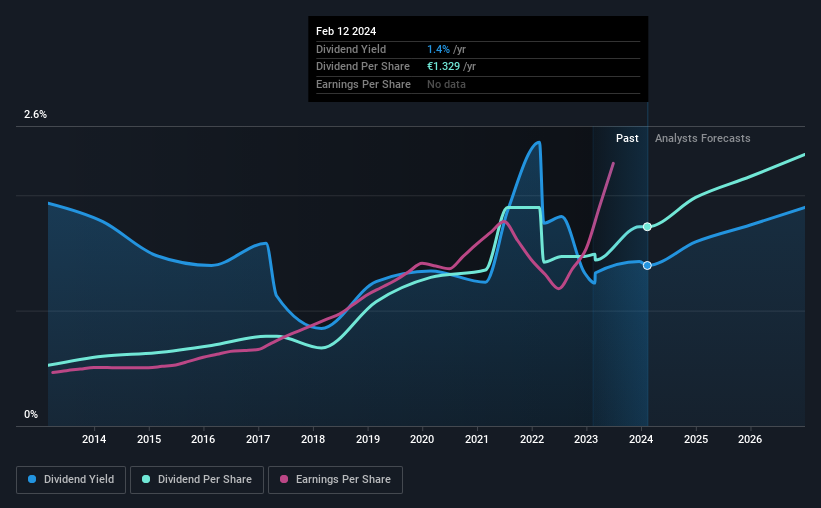

Vidrala, S.A. (BME:VID) has announced that it will be increasing its dividend from last year's comparable payment on the 15th of February to €0.8246. Although the dividend is now higher, the yield is only 1.4%, which is below the industry average.

View our latest analysis for Vidrala

Vidrala's Dividend Is Well Covered By Earnings

If it is predictable over a long period, even low dividend yields can be attractive. However, prior to this announcement, Vidrala's dividend was comfortably covered by both cash flow and earnings. This means that most of what the business earns is being used to help it grow.

The next year is set to see EPS grow by 15.7%. Assuming the dividend continues along recent trends, we think the payout ratio could be 15% by next year, which is in a pretty sustainable range.

Vidrala Has A Solid Track Record

The company has a sustained record of paying dividends with very little fluctuation. Since 2014, the dividend has gone from €0.405 total annually to €1.33. This implies that the company grew its distributions at a yearly rate of about 13% over that duration. Rapidly growing dividends for a long time is a very valuable feature for an income stock.

The Dividend Looks Likely To Grow

Investors who have held shares in the company for the past few years will be happy with the dividend income they have received. Vidrala has seen EPS rising for the last five years, at 19% per annum. With a decent amount of growth and a low payout ratio, we think this bodes well for Vidrala's prospects of growing its dividend payments in the future.

Vidrala Looks Like A Great Dividend Stock

In summary, it is always positive to see the dividend being increased, and we are particularly pleased with its overall sustainability. Distributions are quite easily covered by earnings, which are also being converted to cash flows. All in all, this checks a lot of the boxes we look for when choosing an income stock.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. Earnings growth generally bodes well for the future value of company dividend payments. See if the 10 Vidrala analysts we track are forecasting continued growth with our free report on analyst estimates for the company. Is Vidrala not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BME:VID

Vidrala

Manufactures and sells glass containers for food and beverage products in the United Kingdom, Ireland, Italy, Iberian Peninsula, rest of Europe, and Brazil.

Very undervalued with flawless balance sheet and pays a dividend.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor