Advertisement

- Spain

- /

- Hospitality

- /

- BME:AMS

Amadeus IT Group, S.A. (BME:AMS) Just Released Its First-Quarter Earnings: Here's What Analysts Think

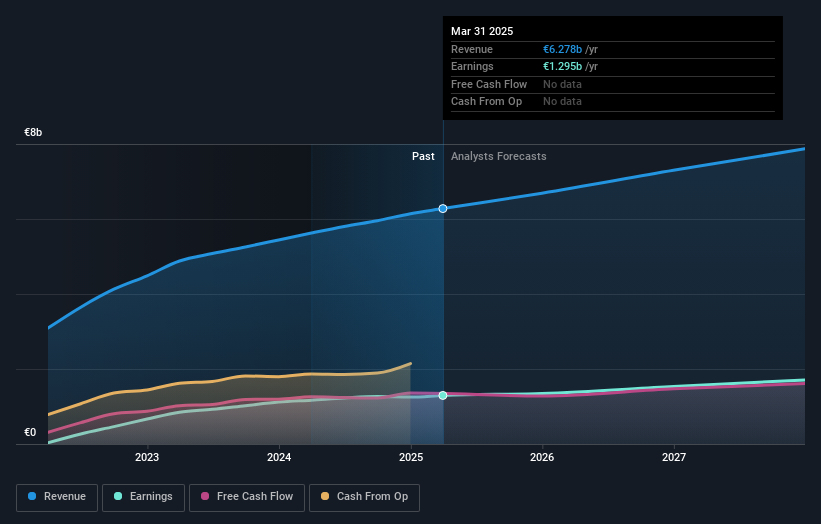

Shareholders might have noticed that Amadeus IT Group, S.A. (BME:AMS) filed its first-quarter result this time last week. The early response was not positive, with shares down 3.7% to €67.88 in the past week. The result was positive overall - although revenues of €1.6b were in line with what the analysts predicted, Amadeus IT Group surprised by delivering a statutory profit of €0.79 per share, modestly greater than expected. This is an important time for investors, as they can track a company's performance in its report, look at what experts are forecasting for next year, and see if there has been any change to expectations for the business. We've gathered the most recent statutory forecasts to see whether the analysts have changed their earnings models, following these results.

Taking into account the latest results, the most recent consensus for Amadeus IT Group from 18 analysts is for revenues of €6.69b in 2025. If met, it would imply a modest 6.5% increase on its revenue over the past 12 months. Statutory earnings per share are predicted to rise 3.8% to €3.05. Before this earnings report, the analysts had been forecasting revenues of €6.76b and earnings per share (EPS) of €3.07 in 2025. The consensus analysts don't seem to have seen anything in these results that would have changed their view on the business, given there's been no major change to their estimates.

View our latest analysis for Amadeus IT Group

The analysts reconfirmed their price target of €77.50, showing that the business is executing well and in line with expectations. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. The most optimistic Amadeus IT Group analyst has a price target of €90.00 per share, while the most pessimistic values it at €65.00. These price targets show that analysts do have some differing views on the business, but the estimates do not vary enough to suggest to us that some are betting on wild success or utter failure.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the Amadeus IT Group's past performance and to peers in the same industry. We would highlight that Amadeus IT Group's revenue growth is expected to slow, with the forecast 8.8% annualised growth rate until the end of 2025 being well below the historical 18% p.a. growth over the last five years. By way of comparison, the other companies in this industry with analyst coverage are forecast to grow their revenue at 6.9% annually. So it's pretty clear that, while Amadeus IT Group's revenue growth is expected to slow, it's still expected to grow faster than the industry itself.

The Bottom Line

The most important thing to take away is that there's been no major change in sentiment, with the analysts reconfirming that the business is performing in line with their previous earnings per share estimates. Happily, there were no major changes to revenue forecasts, with the business still expected to grow faster than the wider industry. There was no real change to the consensus price target, suggesting that the intrinsic value of the business has not undergone any major changes with the latest estimates.

Keeping that in mind, we still think that the longer term trajectory of the business is much more important for investors to consider. At Simply Wall St, we have a full range of analyst estimates for Amadeus IT Group going out to 2027, and you can see them free on our platform here..

Don't forget that there may still be risks. For instance, we've identified 1 warning sign for Amadeus IT Group that you should be aware of.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BME:AMS

Amadeus IT Group

Operates as a transaction processor for the travel and tourism industry in Europe, Central and South America, the Middle East, Africa, and Asia Pacific.

Undervalued with proven track record and pays a dividend.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Upside Gold ·

An Undervalued 3.3Moz Gold Project in Canada

Fair Value:CA$5.0768.0% undervalued

287 followersusers have followed this narrative

1 commentusers have commented on this narrative

42 likesusers have liked this narrative

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8591.3% undervalued

98 followersusers have followed this narrative

2 commentsusers have commented on this narrative

28 likesusers have liked this narrative

TO

Tokyo on Anheuser-Busch InBev ·

EU#8 - Anheuser-Busch InBev: Courage, Capital, and the Discipline to Build an Empire

Fair Value:€89.4524.2% undervalued

8 followersusers have followed this narrative

3 commentsusers have commented on this narrative

4 likesusers have liked this narrative

OS

oscargarcia on Amazon.com ·

The capitalist colossus that makes your parcels magically appear, powers half the internet, and knows your shopping habits.

Fair Value:US$2803.2% undervalued

62 followersusers have followed this narrative

1 commentusers have commented on this narrative

2 likesusers have liked this narrative

Recently Updated Narratives

KI

kinnth on Reddit ·

Strong DAU drives Ads and AI Data narrative

Fair Value:US$309.7747.1% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

RockeTeller on Silver X Mining ·

Silver X Has 152 Million Ounces, Already Producing and Its Biggest Growth Phase May Still Be Ahead

Fair Value:CA$40.8998.1% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

Robbo on Cochlear ·

Cochlear’s Crossroads: Temporary Setback or Structural Shift?

Fair Value:AU$7042.7% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8591.3% undervalued

98 followersusers have followed this narrative

2 commentsusers have commented on this narrative

28 likesusers have liked this narrative

KI

Kingman1152 on NVIDIA ·

NVIDIA will see a profit margin surge of 55% in the next 5 years

Fair Value:US$305.230.7% undervalued

69 followersusers have followed this narrative

2 commentsusers have commented on this narrative

24 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$561.9325.1% undervalued

1399 followersusers have followed this narrative

2 commentsusers have commented on this narrative

12 likesusers have liked this narrative