Advertisement

- Germany

- /

- Telecom Services and Carriers

- /

- XTRA:NFN

NFON AG (ETR:NFN) Analysts Are Pretty Bullish On The Stock After Recent Results

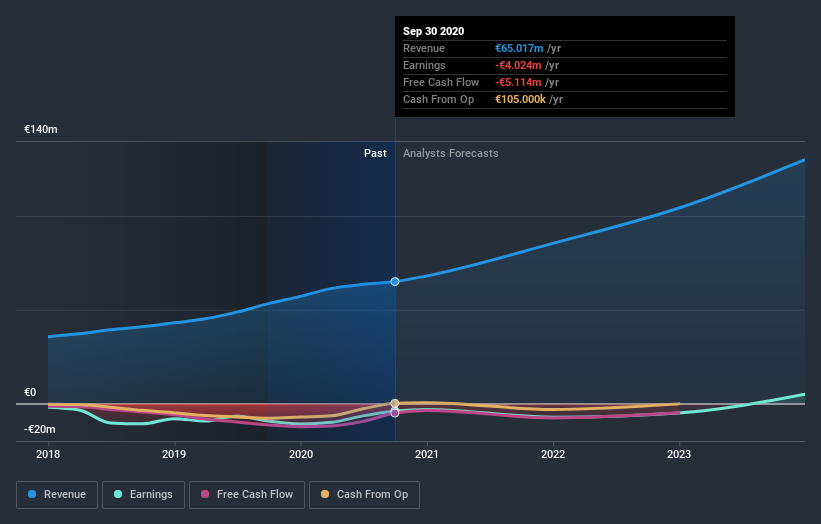

Investors in NFON AG (ETR:NFN) had a good week, as its shares rose 6.2% to close at €18.05 following the release of its quarterly results. Revenues were €16m, with NFON reporting some 6.4% below analyst expectations. Following the result, the analysts have updated their earnings model, and it would be good to know whether they think there's been a strong change in the company's prospects, or if it's business as usual. So we collected the latest post-earnings statutory consensus estimates to see what could be in store for next year.

See our latest analysis for NFON

Taking into account the latest results, the consensus forecast from NFON's four analysts is for revenues of €68.1m in 2020, which would reflect a reasonable 4.7% improvement in sales compared to the last 12 months. Losses are predicted to fall substantially, shrinking 52% to €0.22. Yet prior to the latest earnings, the analysts had been forecasting revenues of €69.1m and losses of €0.37 per share in 2020. While the revenue estimates were largely unchanged, sentiment seems to have improved, with the analysts upgrading revenues and making a losses per share in particular.

The average price target rose 13% to €19.75, with the analysts signalling that the forecast reduction in losses would be a positive for the stock's valuation. Fixating on a single price target can be unwise though, since the consensus target is effectively the average of analyst price targets. As a result, some investors like to look at the range of estimates to see if there are any diverging opinions on the company's valuation. There are some variant perceptions on NFON, with the most bullish analyst valuing it at €22.00 and the most bearish at €15.00 per share. Analysts definitely have varying views on the business, but the spread of estimates is not wide enough in our view to suggest that extreme outcomes could await NFON shareholders.

Looking at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up against both past performance and industry growth estimates. It's pretty clear that there is an expectation that NFON's revenue growth will slow down substantially, with revenues next year expected to grow 4.7%, compared to a historical growth rate of 21% over the past five years. Juxtapose this against the other companies in the industry with analyst coverage, which are forecast to grow their revenues (in aggregate) 3.1% next year. Even after the forecast slowdown in growth, it seems obvious that NFON is also expected to grow faster than the wider industry.

The Bottom Line

The most obvious conclusion is that the analysts made no changes to their forecasts for a loss next year. Fortunately, they also reconfirmed their revenue numbers, suggesting sales are tracking in line with expectations - and our data suggests that revenues are expected to grow faster than the wider industry. We note an upgrade to the price target, suggesting that the analysts believes the intrinsic value of the business is likely to improve over time.

With that in mind, we wouldn't be too quick to come to a conclusion on NFON. Long-term earnings power is much more important than next year's profits. We have estimates - from multiple NFON analysts - going out to 2023, and you can see them free on our platform here.

Don't forget that there may still be risks. For instance, we've identified 1 warning sign for NFON that you should be aware of.

When trading NFON or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if NFON might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About XTRA:NFN

NFON

Provides integrated business communication with a focus on AI-based applications to business customers in Germany, Austria, Italy, the United Kingdom, Spain, Italy, France, Poland, and Portugal.

Flawless balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|5.4% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.3% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|4.1% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|62.7% undervalued

DA

Community Contributor