Advertisement

If we want to find a potential multi-bagger, often there are underlying trends that can provide clues. Ideally, a business will show two trends; firstly a growing return on capital employed (ROCE) and secondly, an increasing amount of capital employed. This shows us that it's a compounding machine, able to continually reinvest its earnings back into the business and generate higher returns. However, after investigating EQS Group (ETR:EQS), we don't think it's current trends fit the mold of a multi-bagger.

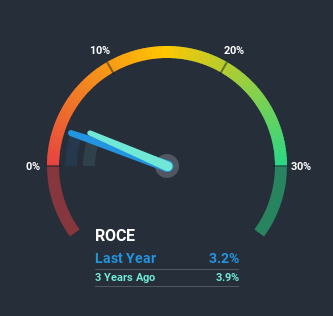

What is Return On Capital Employed (ROCE)?

For those that aren't sure what ROCE is, it measures the amount of pre-tax profits a company can generate from the capital employed in its business. Analysts use this formula to calculate it for EQS Group:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.032 = €1.1m ÷ (€47m - €12m) (Based on the trailing twelve months to September 2020).

Thus, EQS Group has an ROCE of 3.2%. In absolute terms, that's a low return and it also under-performs the Software industry average of 15%.

View our latest analysis for EQS Group

Above you can see how the current ROCE for EQS Group compares to its prior returns on capital, but there's only so much you can tell from the past. If you'd like to see what analysts are forecasting going forward, you should check out our free report for EQS Group.

What Can We Tell From EQS Group's ROCE Trend?

On the surface, the trend of ROCE at EQS Group doesn't inspire confidence. To be more specific, ROCE has fallen from 9.6% over the last five years. However, given capital employed and revenue have both increased it appears that the business is currently pursuing growth, at the consequence of short term returns. If these investments prove successful, this can bode very well for long term stock performance.

In Conclusion...

Even though returns on capital have fallen in the short term, we find it promising that revenue and capital employed have both increased for EQS Group. And long term investors must be optimistic going forward because the stock has returned a huge 427% to shareholders in the last five years. So while the underlying trends could already be accounted for by investors, we still think this stock is worth looking into further.

EQS Group does have some risks though, and we've spotted 2 warning signs for EQS Group that you might be interested in.

While EQS Group isn't earning the highest return, check out this free list of companies that are earning high returns on equity with solid balance sheets.

If you’re looking to trade EQS Group, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if EQS Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About XTRA:EQS

EQS Group

EQS Group AG provides cloud-based software in the areas of corporate compliance; investor relations; and environment, social, and governance in Germany and internationally.

Reasonable growth potential with adequate balance sheet.

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Giftify ·

Giftify ($GIFT): A Small-Cap Incentives Platform with More ScaleThan Its Valuation Suggests

Fair Value:US$2.564.0% undervalued

46 followersusers have followed this narrative

2 commentsusers have commented on this narrative

9 likesusers have liked this narrative

HA

HarishPK on lululemon athletica ·

Quantifying the Transition: Why Lululemon’s Moat Remains Intact

Fair Value:US$161.828.0% undervalued

21 followersusers have followed this narrative

2 commentsusers have commented on this narrative

9 likesusers have liked this narrative

TR

tripledub on Alphabet ·

Warren Buffett Just Bet $10 Billion on Google. The Catch? You May Already Be Too Late.

Fair Value:US$23056.0% overvalued

50 followersusers have followed this narrative

1 commentusers have commented on this narrative

13 likesusers have liked this narrative

JO

John_Eric on Veeva Systems ·

AI-Powered Veeva Systems Poised for Solid Growth Amid Regulatory Stability

Fair Value:US$32040.7% undervalued

31 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

Recently Updated Narratives

TH

TheInternationalInvestor on PTFC Redevelopment ·

The Hidden Southeast Asian Compounder: How an Overlooked Storage and Leasing Company Quietly Created Wealth for a Decade

Fair Value:₱6320.5% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DA

danmad on Karoon Energy ·

A Cash-Generating Oil Producer the Market Has Turned Against

Fair Value:AU$1.7717.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RI

richard_53rym on Nintendo ·

Nintendo facing the Ram shortage situation

Fair Value:JP¥8k12.3% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75030.2% undervalued

86 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5452.2% undervalued

61 followersusers have followed this narrative

3 commentsusers have commented on this narrative

11 likesusers have liked this narrative

AN

AnalystConsensusTarget on Broadcom ·

AVGO: Upcoming AI Chip Production With Key Partner Will Shape Competitive Position

Fair Value:US$523.7323.4% undervalued

689 followersusers have followed this narrative

3 commentsusers have commented on this narrative

5 likesusers have liked this narrative

Trending Discussion

HA

HarishPK on lululemon athletica ·

Difficult isn’t it? Valuation experts like Aswath Damodaran suggest 12 to 18 months for value and pr...

0

|0