Advertisement

- Germany

- /

- Semiconductors

- /

- XTRA:TPE

Analyst Estimates: Here's What Brokers Think Of PVA TePla AG (ETR:TPE) After Its Yearly Report

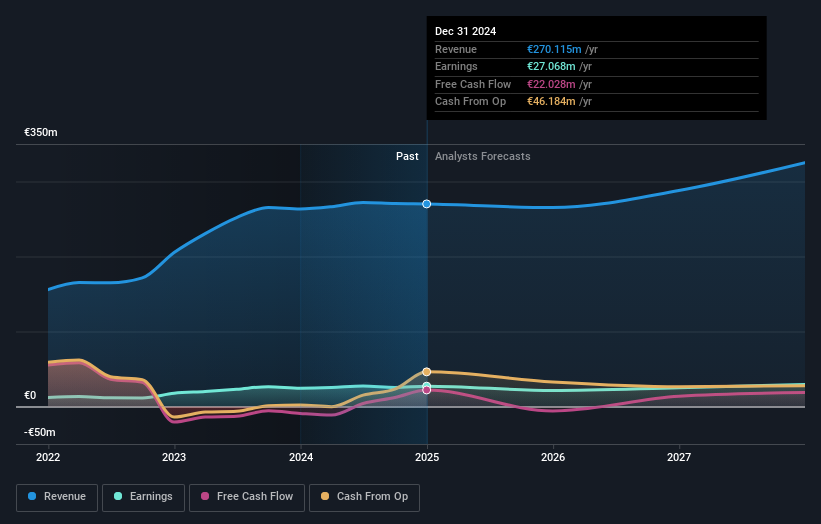

It's been a pretty great week for PVA TePla AG (ETR:TPE) shareholders, with its shares surging 10% to €15.29 in the week since its latest yearly results. Results were roughly in line with estimates, with revenues of €270m and statutory earnings per share of €1.25. The analysts typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. So we gathered the latest post-earnings forecasts to see what estimates suggest is in store for next year.

Following last week's earnings report, PVA TePla's eleven analysts are forecasting 2025 revenues to be €265.2m, approximately in line with the last 12 months. Statutory earnings per share are expected to tumble 23% to €0.99 in the same period. Before this earnings report, the analysts had been forecasting revenues of €259.2m and earnings per share (EPS) of €1.07 in 2025. Overall it looks as though the analysts were a bit mixed on the latest results. Although there was a to revenue, the consensus also made a minor downgrade to its earnings per share forecasts.

View our latest analysis for PVA TePla

There's been no major changes to the price target of €21.11, suggesting that the impact of higher forecast revenue and lower earnings won't result in a meaningful change to the business' valuation. There's another way to think about price targets though, and that's to look at the range of price targets put forward by analysts, because a wide range of estimates could suggest a diverse view on possible outcomes for the business. Currently, the most bullish analyst values PVA TePla at €35.26 per share, while the most bearish prices it at €12.00. We would probably assign less value to the analyst forecasts in this situation, because such a wide range of estimates could imply that the future of this business is difficult to value accurately. With this in mind, we wouldn't rely too heavily the consensus price target, as it is just an average and analysts clearly have some deeply divergent views on the business.

Looking at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up against both past performance and industry growth estimates. These estimates imply that revenue is expected to slow, with a forecast annualised decline of 1.8% by the end of 2025. This indicates a significant reduction from annual growth of 19% over the last five years. By contrast, our data suggests that other companies (with analyst coverage) in the same industry are forecast to see their revenue grow 8.1% annually for the foreseeable future. So although its revenues are forecast to shrink, this cloud does not come with a silver lining - PVA TePla is expected to lag the wider industry.

The Bottom Line

The most important thing to take away is that the analysts downgraded their earnings per share estimates, showing that there has been a clear decline in sentiment following these results. They also upgraded their revenue estimates for next year, even though it is expected to grow slower than the wider industry. The consensus price target held steady at €21.11, with the latest estimates not enough to have an impact on their price targets.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. We have forecasts for PVA TePla going out to 2027, and you can see them free on our platform here.

You can also see our analysis of PVA TePla's Board and CEO remuneration and experience, and whether company insiders have been buying stock.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About XTRA:TPE

PVA TePla

Offers systems and solutions to produce components for energy storage systems, photovoltaic modules, and wind turbines worldwide.

Excellent balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|3.6% undervalued

TI

Community Contributor

Recently Updated Narratives

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$26.6927.9% undervalued

44 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8148.6% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AU

AuCA on Nova Ljubljanska Banka d.d ·

Nova Ljubljanska Banka d.d will expect a 11.2% revenue boost driving future growth

Fair Value:€20916.3% undervalued

23 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3406.3% undervalued

131 followersusers have followed this narrative

6 commentsusers have commented on this narrative

17 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

81 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7921.6% undervalued

918 followersusers have followed this narrative

5 commentsusers have commented on this narrative

21 likesusers have liked this narrative