- Germany

- /

- Real Estate

- /

- XTRA:DWNI

We Think Some Shareholders May Hesitate To Increase Deutsche Wohnen SE's (ETR:DWNI) CEO Compensation

CEO Michael Zahn has done a decent job of delivering relatively good performance at Deutsche Wohnen SE (ETR:DWNI) recently. As shareholders go into the upcoming AGM on 01 June 2021, CEO compensation will probably not be their focus, but rather the steps management will take to continue the growth momentum. However, some shareholders may still want to keep CEO compensation within reason.

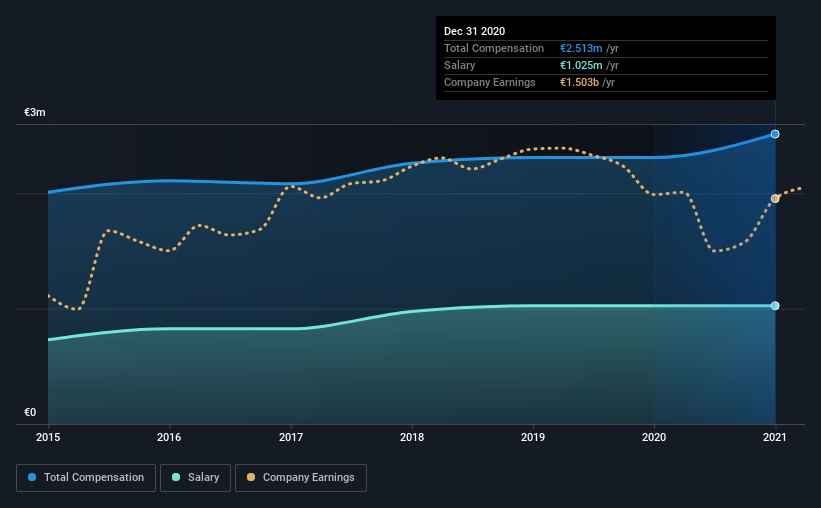

See our latest analysis for Deutsche Wohnen

Comparing Deutsche Wohnen SE's CEO Compensation With the industry

According to our data, Deutsche Wohnen SE has a market capitalization of €18b, and paid its CEO total annual compensation worth €2.5m over the year to December 2020. We note that's an increase of 8.8% above last year. While we always look at total compensation first, our analysis shows that the salary component is less, at €1.0m.

In comparison with other companies in the industry with market capitalizations over €6.5b , the reported median total CEO compensation was €1.9m. Hence, we can conclude that Michael Zahn is remunerated higher than the industry median. What's more, Michael Zahn holds €5.8m worth of shares in the company in their own name, indicating that they have a lot of skin in the game.

| Component | 2020 | 2019 | Proportion (2020) |

| Salary | €1.0m | €1.0m | 41% |

| Other | €1.5m | €1.3m | 59% |

| Total Compensation | €2.5m | €2.3m | 100% |

On an industry level, roughly 41% of total compensation represents salary and 59% is other remuneration. There isn't a significant difference between Deutsche Wohnen and the broader market, in terms of salary allocation in the overall compensation package. It's important to note that a slant towards non-salary compensation suggests that total pay is tied to the company's performance.

Deutsche Wohnen SE's Growth

Over the last three years, Deutsche Wohnen SE has shrunk its earnings per share by 3.1% per year. In the last year, its revenue is up 25%.

The decrease in EPS could be a concern for some investors. But in contrast the revenue growth is strong, suggesting future potential for EPS growth. In conclusion we can't form a strong opinion about business performance yet; but it's one worth watching. Looking ahead, you might want to check this free visual report on analyst forecasts for the company's future earnings..

Has Deutsche Wohnen SE Been A Good Investment?

We think that the total shareholder return of 41%, over three years, would leave most Deutsche Wohnen SE shareholders smiling. This strong performance might mean some shareholders don't mind if the CEO were to be paid more than is normal for a company of its size.

To Conclude...

The overall company performance has been commendable, however there are still areas for improvement. We still think that some shareholders will be hesitant of increasing CEO pay until EPS growth improves, since they are already paid higher than the industry.

We can learn a lot about a company by studying its CEO compensation trends, along with looking at other aspects of the business. In our study, we found 3 warning signs for Deutsche Wohnen you should be aware of, and 2 of them shouldn't be ignored.

Important note: Deutsche Wohnen is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

When trading Deutsche Wohnen or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About XTRA:DWNI

Moderate growth potential with imperfect balance sheet.