Stock Analysis

- Germany

- /

- Specialty Stores

- /

- XTRA:ZAL

Stratec Leads Three German Exchange Growth Companies With High Insider Ownership

Reviewed by Simply Wall St

Amid a backdrop of political uncertainty and fluctuating economic indicators in Europe, Germany's DAX index has shown resilience with a modest rise. In such an environment, growth companies with high insider ownership, like Stratec, can be particularly appealing as they often demonstrate strong alignment between management’s interests and those of shareholders.

Top 10 Growth Companies With High Insider Ownership In Germany

| Name | Insider Ownership | Earnings Growth |

| pferdewetten.de (XTRA:EMH) | 26.8% | 75.4% |

| Deutsche Beteiligungs (XTRA:DBAN) | 35.4% | 31.6% |

| YOC (XTRA:YOC) | 24.8% | 21.8% |

| NAGA Group (XTRA:N4G) | 14.1% | 79.2% |

| Exasol (XTRA:EXL) | 25.3% | 105.4% |

| Alelion Energy Systems (DB:2FZ) | 37.4% | 106.6% |

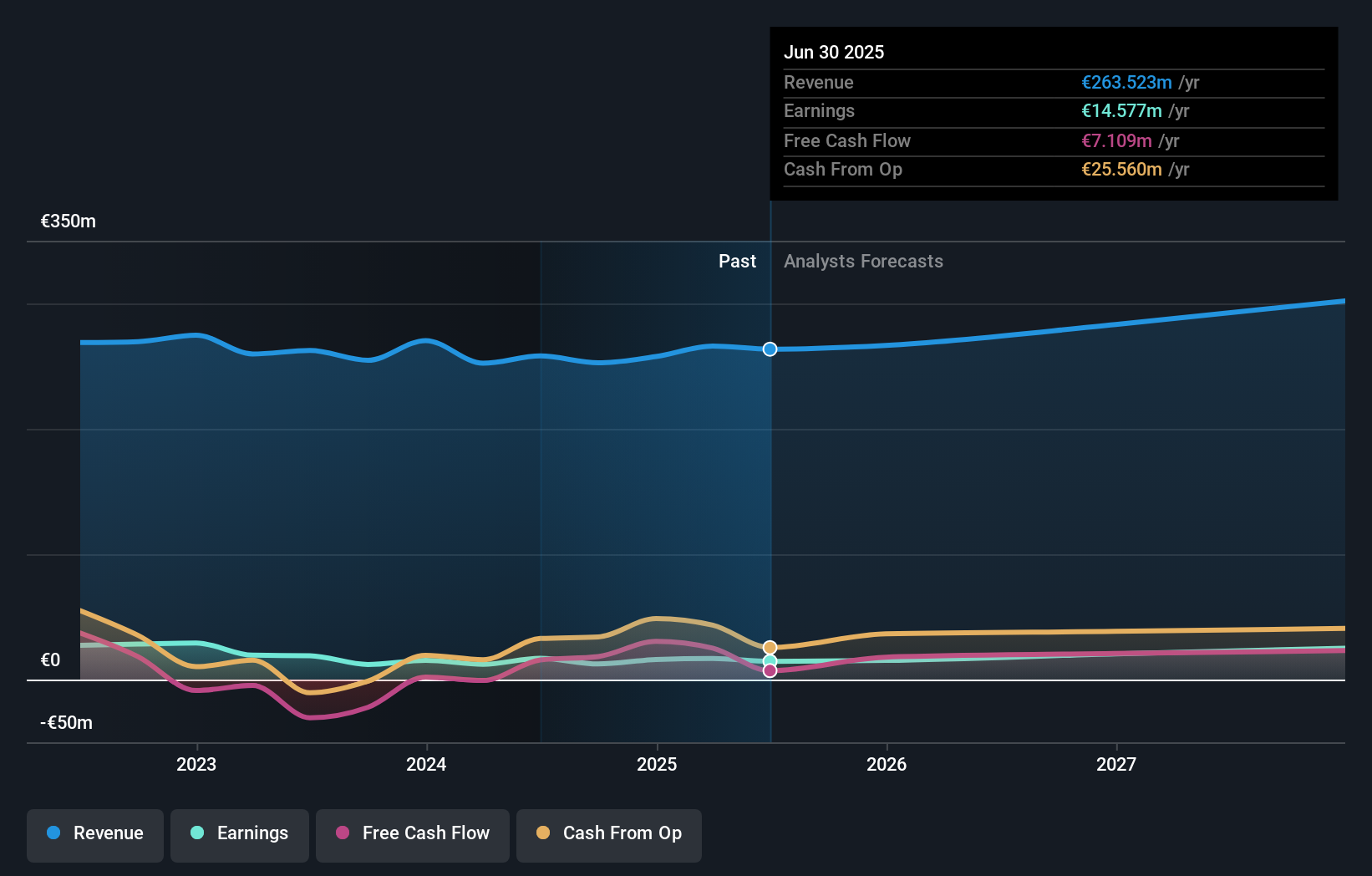

| Stratec (XTRA:SBS) | 30.9% | 21.9% |

| Redcare Pharmacy (XTRA:RDC) | 17.7% | 48.7% |

| Your Family Entertainment (DB:RTV) | 17.5% | 116.8% |

| Friedrich Vorwerk Group (XTRA:VH2) | 18% | 30.4% |

Let's explore several standout options from the results in the screener.

Stratec (XTRA:SBS)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Stratec SE operates in designing and manufacturing automation and instrumentation solutions for in-vitro diagnostics and life sciences, serving markets in Germany, the European Union, and internationally, with a market capitalization of approximately €0.56 billion.

Operations: The company generates its revenue by designing and manufacturing automation and instrumentation solutions for in-vitro diagnostics and life sciences across Germany, the European Union, and other international markets.

Insider Ownership: 30.9%

Earnings Growth Forecast: 21.9% p.a.

Stratec SE, a German growth company with high insider ownership, faces challenges and opportunities. Recently presenting at significant industry conferences, Stratec reported a decline in Q1 earnings with sales dropping to €50.87 million and net income to €0.447 million. Despite current financial pressures, notably a debt not well covered by operating cash flow and lower profit margins year-over-year, the company is trading at 44% below estimated fair value. Positively, Stratec's revenue is expected to outpace the German market growth rate, with forecasts suggesting an annual revenue increase of 7.8%.

- Navigate through the intricacies of Stratec with our comprehensive analyst estimates report here.

- Our valuation report unveils the possibility Stratec's shares may be trading at a premium.

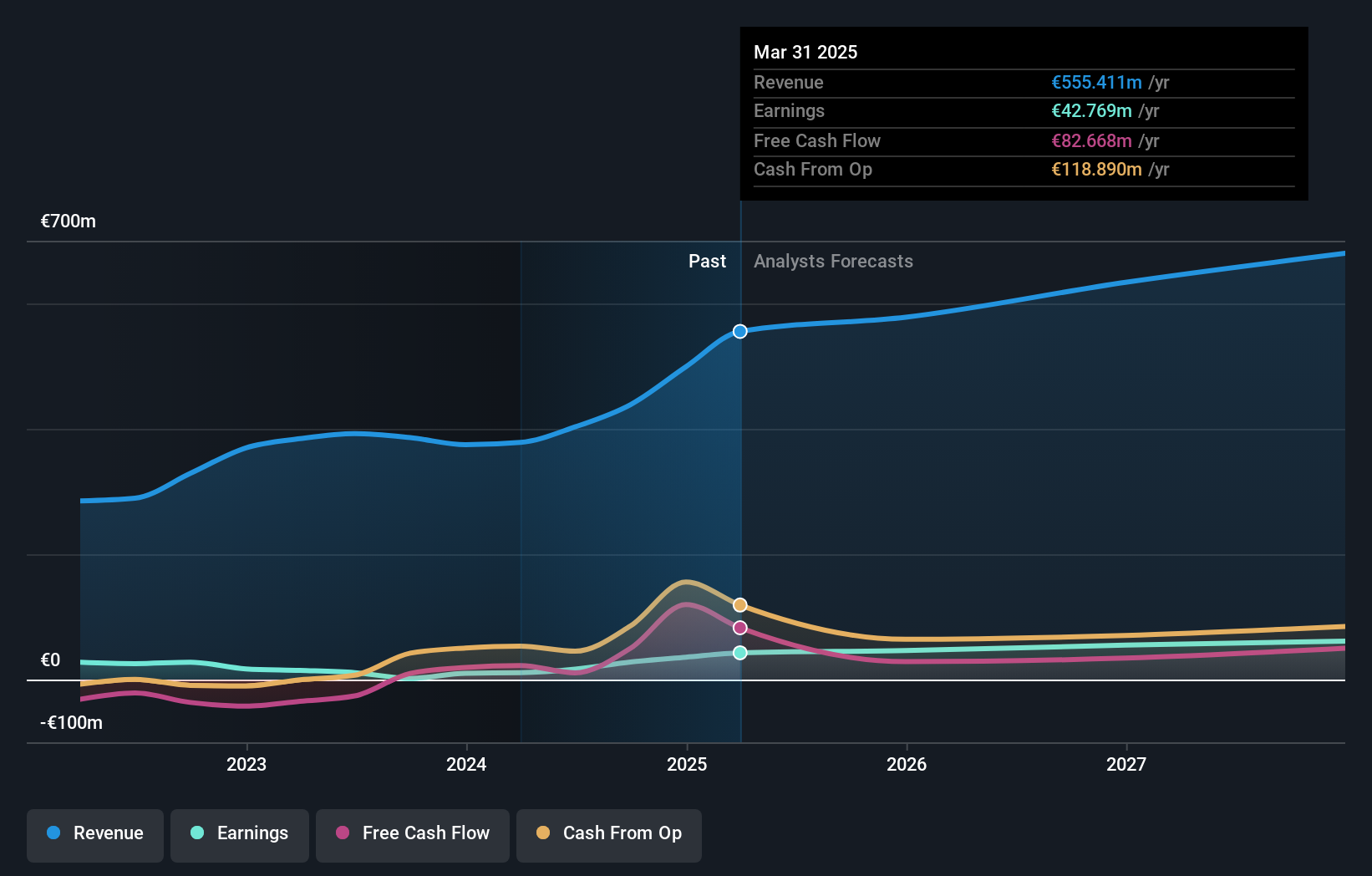

Friedrich Vorwerk Group (XTRA:VH2)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Friedrich Vorwerk Group SE specializes in offering solutions for the transformation and transportation of energy across Germany and Europe, with a market capitalization of approximately €0.37 billion.

Operations: The company generates revenue through segments focused on electricity (€72.07 million), natural gas (€157.60 million), clean hydrogen (€28.59 million), and adjacent opportunities (€118.73 million).

Insider Ownership: 18%

Earnings Growth Forecast: 30.4% p.a.

Friedrich Vorwerk Group SE, a German company with significant insider ownership, demonstrates robust growth prospects. Recent earnings show an upward trajectory with Q1 sales rising to €81.2 million and net income improving to €1.56 million from the previous year. The company's earnings are expected to grow by 30.45% annually over the next three years, outpacing the German market's forecasted 18.6%. However, its forecasted return on equity is relatively low at 11%, and revenue growth at 8.3% per year, though above the market average of 5.2%, is not considered high.

- Get an in-depth perspective on Friedrich Vorwerk Group's performance by reading our analyst estimates report here.

- According our valuation report, there's an indication that Friedrich Vorwerk Group's share price might be on the expensive side.

Zalando (XTRA:ZAL)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Zalando SE is an online retailer specializing in fashion and lifestyle products, with a market capitalization of approximately €5.97 billion.

Operations: The company generates €10.40 billion in revenue from its online fashion and lifestyle platform.

Insider Ownership: 10.4%

Earnings Growth Forecast: 26.6% p.a.

Zalando SE, a key player in Germany's e-commerce sector, is poised for substantial growth with earnings expected to increase by 26.56% annually. Although its revenue growth forecast of 5.4% per year slightly surpasses the German market average, it remains below the high-growth benchmark of 20%. The company's recent financial performance reflects a robust uptick with last year’s earnings surging by over 184%. Moreover, Zalando trades at a significant discount to its estimated fair value, highlighting potential undervaluation despite a forecasted modest return on equity of 12.7% in three years.

- Unlock comprehensive insights into our analysis of Zalando stock in this growth report.

- Insights from our recent valuation report point to the potential overvaluation of Zalando shares in the market.

Summing It All Up

- Navigate through the entire inventory of 18 Fast Growing German Companies With High Insider Ownership here.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're helping make it simple.

Find out whether Zalando is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About XTRA:ZAL

Excellent balance sheet with reasonable growth potential.