Advertisement

Can Volkswagen’s Share Price Rally as U.S. Considers Auto Tariff Relief?

Simply Wall St

Reviewed by Bailey Pemberton

If you are weighing what to do with your Volkswagen shares, you are not alone. Lately, Volkswagen’s stock has been on a wild ride, leaving many investors wondering if they are looking at a great deal or a value trap. Over the past seven days, the stock lost 4.4%, building on a 12.6% slide over the past month. Yet, year to date, it is actually up 2.1%. That pattern says a lot about how swiftly market perceptions can shift, especially when it comes to global automakers.

Recent headlines could help explain some of the volatility. Hopes for U.S. auto tariff relief have flickered, and Volkswagen’s efforts to lock down its dominance in Europe are getting plenty of attention. These developments hint at both opportunity and risk, with the company navigating major crosswinds in global trade and fierce competition from Chinese rivals. Long-term performance? Over five years, the shares have barely budged, up just 0.2%, which means many are waiting for a catalyst that will move the needle meaningfully.

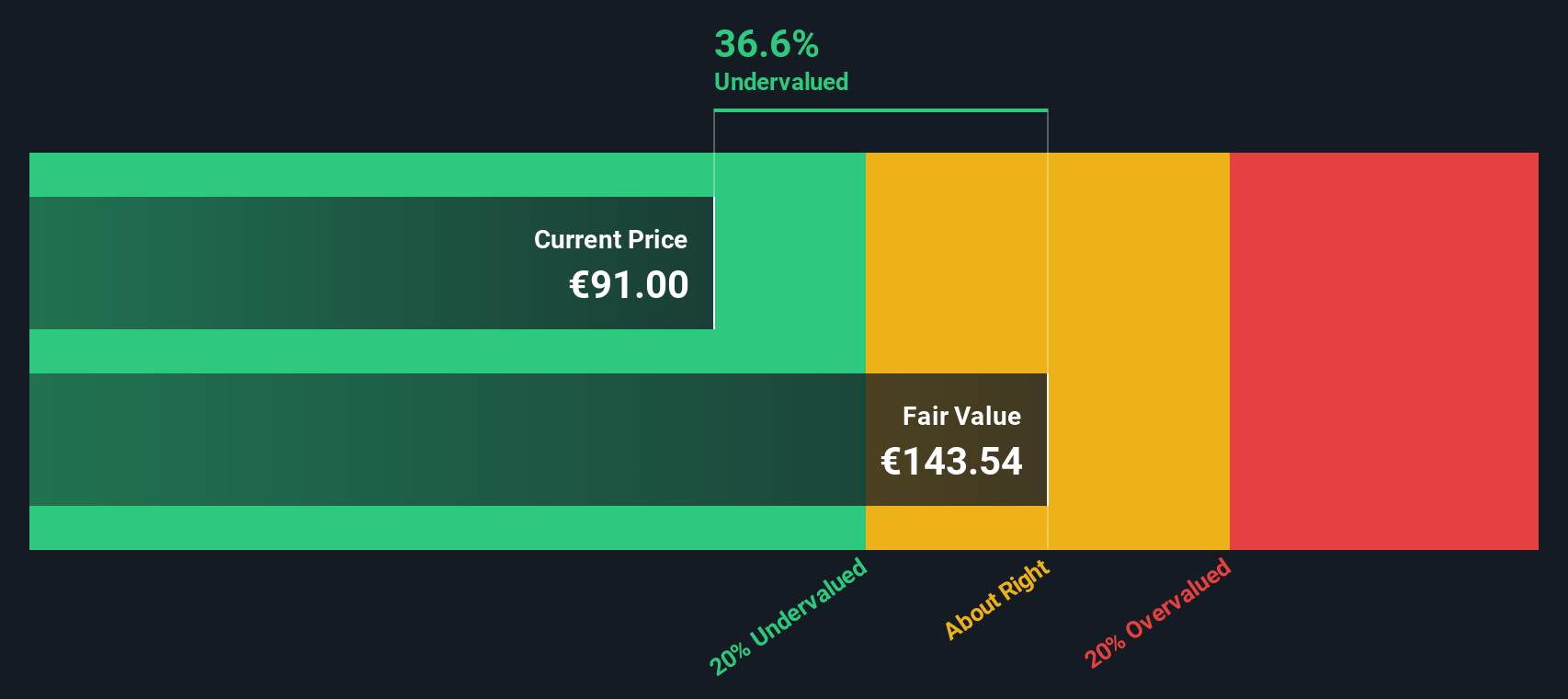

So, is Volkswagen undervalued at its recent close of €89.16? According to our valuation score, the company is undervalued in five out of six key checks, putting its score at 5, an impressive mark for a mature industry heavyweight. In the next section, we will break down exactly how those valuation methods stack up and what they tell us about Volkswagen today. But stick around, because before we finish, we will introduce an even smarter way to size up the company’s real worth.

Approach 1: Volkswagen Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a company’s value by projecting its future cash flows and discounting them back to today’s value. For Volkswagen, this approach relies on forecasts for Free Cash Flow (FCF), which reflect the money left after capital expenditures. This is a crucial metric for evaluating long-term value.

Currently, Volkswagen’s trailing twelve-month Free Cash Flow is negative, at -€10.5 Billion, highlighting recent operational challenges or heavy investment periods. Looking ahead, analysts forecast significant improvement, expecting annual FCF to rise to around €6.7 Billion by the end of 2028. Beyond the analyst horizon, further annual projections are extrapolated through 2035 and estimate FCF could continue climbing modestly each year, based on reasonable industry trends.

After crunching the numbers with the 2 Stage Free Cash Flow to Equity model, the estimated intrinsic value per share stands at €143.54. That is a robust 37.9% premium over the current share price of €89.16, strongly suggesting Volkswagen stock is undervalued based on projected cash flows and the DCF methodology.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Volkswagen is undervalued by 37.9%. Track this in your watchlist or portfolio, or discover more undervalued stocks.

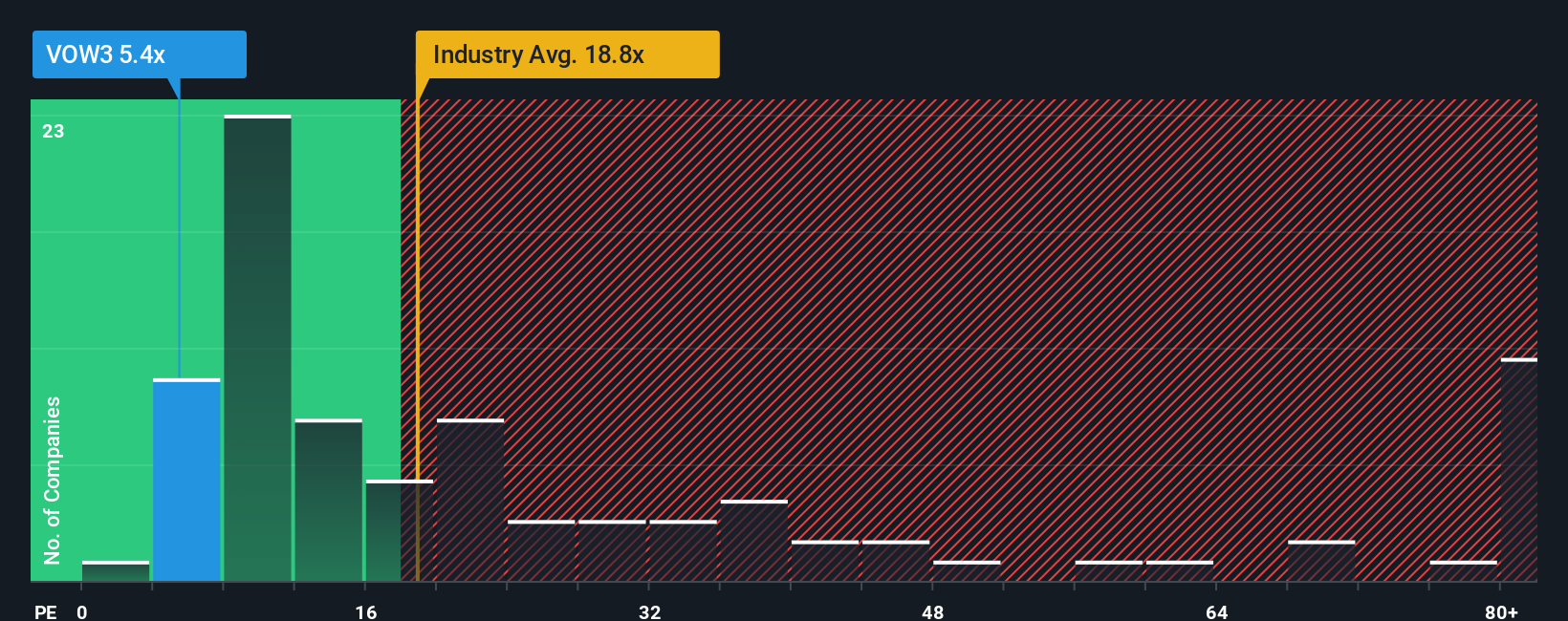

Approach 2: Volkswagen Price vs Earnings (P/E Multiple)

The Price-to-Earnings (P/E) ratio is a reliable yardstick for valuing profitable companies like Volkswagen, since it relates the current share price to per-share earnings and gives a sense of how much investors are willing to pay for each euro of profit.

Typically, companies with higher earnings growth prospects and lower risk command higher P/E ratios. More mature, slower-growing, or riskier firms tend to trade on lower multiples. The key is to compare Volkswagen’s P/E not just in isolation, but against industry norms and similar peers.

Volkswagen is currently trading at a P/E of just 5.3x, well below the auto industry average of 19.0x and the peer average of 10.8x. At first glance, this steep discount may look like a bargain. However, it is important to consider whether these comparisons fairly reflect the company’s unique profile.

This is where Simply Wall St’s “Fair Ratio” comes in. The Fair Ratio is a proprietary metric that adjusts the expected P/E ratio for factors such as Volkswagen’s earnings growth, profit margins, market cap, and company-specific risks. Unlike simple peer or industry comparisons, the Fair Ratio aims to be a more accurate benchmark tailored to the company’s fundamentals.

Volkswagen’s Fair Ratio is 14.9x, well above its current P/E of 5.3x. This sizable gap indicates the stock is undervalued, even when factoring in company-specific risks and industry context.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Volkswagen Narrative

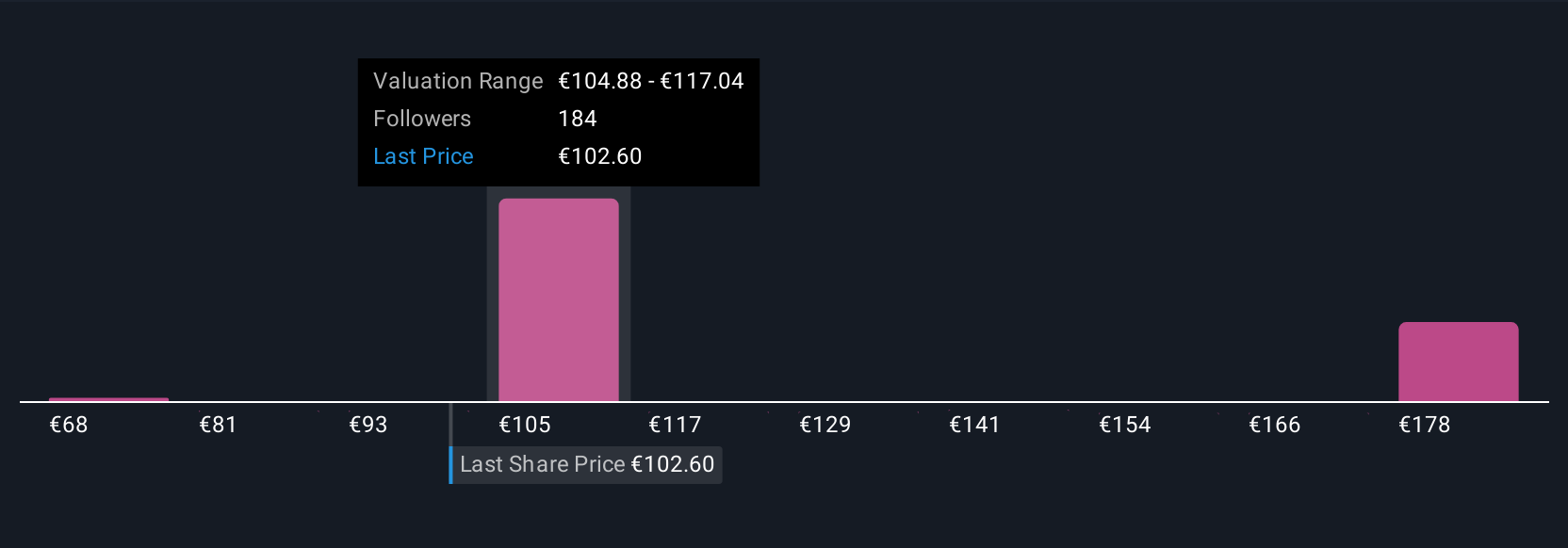

Earlier, we mentioned there is an even better way to size up Volkswagen than traditional valuation methods. Let us introduce you to Narratives. A Narrative is your chance to tell the story behind the numbers, weaving together your expectations on Volkswagen’s revenue, profits, and margins with your view of its fair value. Unlike static valuation models, a Narrative links your personal perspective, reflecting what you believe will shape Volkswagen’s future, to a dynamic financial forecast, and then directly to a fair value estimate.

On Simply Wall St’s Community page, Narratives are an easy tool used by millions of investors to compare their own fair value of Volkswagen to today’s share price. This helps you decide whether now is the time to buy, hold, or sell. These Narratives update automatically when big news or earnings hit the market, ensuring your analysis always stays relevant.

For example, one investor might believe recent strategic missteps will keep Volkswagen’s fair value as low as €68.40. Another investor, focused on electric vehicle momentum and global expansion, may see a much higher fair value near €113.55. With Narratives, you can quickly see how your view compares and make smarter, more confident decisions in real time.

For Volkswagen, here are previews of two leading Volkswagen Narratives:

Fair value: €113.55

Undervalued by 21.5%

Forecast revenue growth: 2.8%

- Growth is centered around expanding electrified vehicles, digital services, and operational restructuring in premium markets.

- Local production, global partnerships, and cost optimization help reduce geopolitical risks and support recurring revenue growth.

- Continued investment in software, premium brand expansion, and margin recovery contributes to long-term profitability potential.

Fair value: €68.40

Overvalued by 30.4%

Forecast revenue growth: 1.0%

- Strategic errors and past scandals have weighed on competitiveness and reputation, especially outside Germany.

- Heavy dependency on China and delays in the electric transition limit flexibility and expose Volkswagen to greater risks.

- Recent margin improvement targets have been postponed, reflecting a weak profitability outlook and muted growth guidance.

Do you think there's more to the story for Volkswagen? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About XTRA:VOW3

Volkswagen

Manufactures and sells automobiles in Germany, other European countries, North America, South America, the Asia-Pacific, and internationally.

Undervalued with adequate balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.6% undervalued

TI

Community Contributor

Recently Updated Narratives

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$26.6926.7% undervalued

44 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8147.4% undervalued

8 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

AU

AuCA on Nova Ljubljanska Banka d.d ·

Nova Ljubljanska Banka d.d will expect a 11.2% revenue boost driving future growth

Fair Value:€20916.5% undervalued

23 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

88 followersusers have followed this narrative

11 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

926 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative