Advertisement

- Germany

- /

- Auto Components

- /

- XTRA:NVM

It's Down 25% But Novem Group S.A. (ETR:NVM) Could Be Riskier Than It Looks

Novem Group S.A. (ETR:NVM) shareholders that were waiting for something to happen have been dealt a blow with a 25% share price drop in the last month. Instead of being rewarded, shareholders who have already held through the last twelve months are now sitting on a 46% share price drop.

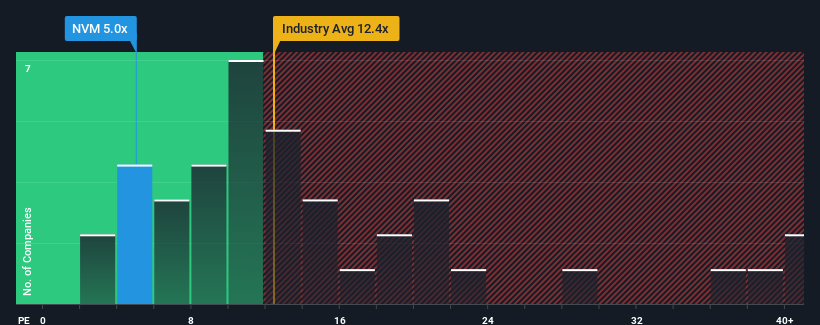

Although its price has dipped substantially, Novem Group may still be sending very bullish signals at the moment with its price-to-earnings (or "P/E") ratio of 5x, since almost half of all companies in Germany have P/E ratios greater than 17x and even P/E's higher than 36x are not unusual. However, the P/E might be quite low for a reason and it requires further investigation to determine if it's justified.

With earnings that are retreating more than the market's of late, Novem Group has been very sluggish. The P/E is probably low because investors think this poor earnings performance isn't going to improve at all. You'd much rather the company wasn't bleeding earnings if you still believe in the business. If not, then existing shareholders will probably struggle to get excited about the future direction of the share price.

Check out our latest analysis for Novem Group

How Is Novem Group's Growth Trending?

The only time you'd be truly comfortable seeing a P/E as depressed as Novem Group's is when the company's growth is on track to lag the market decidedly.

Retrospectively, the last year delivered a frustrating 30% decrease to the company's bottom line. This means it has also seen a slide in earnings over the longer-term as EPS is down 78% in total over the last three years. Therefore, it's fair to say the earnings growth recently has been undesirable for the company.

Turning to the outlook, the next year should generate growth of 22% as estimated by the four analysts watching the company. That's shaping up to be materially higher than the 13% growth forecast for the broader market.

In light of this, it's peculiar that Novem Group's P/E sits below the majority of other companies. It looks like most investors are not convinced at all that the company can achieve future growth expectations.

What We Can Learn From Novem Group's P/E?

Shares in Novem Group have plummeted and its P/E is now low enough to touch the ground. We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

Our examination of Novem Group's analyst forecasts revealed that its superior earnings outlook isn't contributing to its P/E anywhere near as much as we would have predicted. When we see a strong earnings outlook with faster-than-market growth, we assume potential risks are what might be placing significant pressure on the P/E ratio. It appears many are indeed anticipating earnings instability, because these conditions should normally provide a boost to the share price.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 2 warning signs with Novem Group, and understanding these should be part of your investment process.

If these risks are making you reconsider your opinion on Novem Group, explore our interactive list of high quality stocks to get an idea of what else is out there.

Valuation is complex, but we're here to simplify it.

Discover if Novem Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About XTRA:NVM

Novem Group

Develops and supplies trim elements and decorative function elements for car interiors in the automotive industry.

Undervalued with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor