Advertisement

- China

- /

- Gas Utilities

- /

- SZSE:300332

Why Investors Shouldn't Be Surprised By Top Resource Energy Co., Ltd.'s (SZSE:300332) 28% Share Price Surge

Top Resource Energy Co., Ltd. (SZSE:300332) shares have had a really impressive month, gaining 28% after a shaky period beforehand. Unfortunately, the gains of the last month did little to right the losses of the last year with the stock still down 38% over that time.

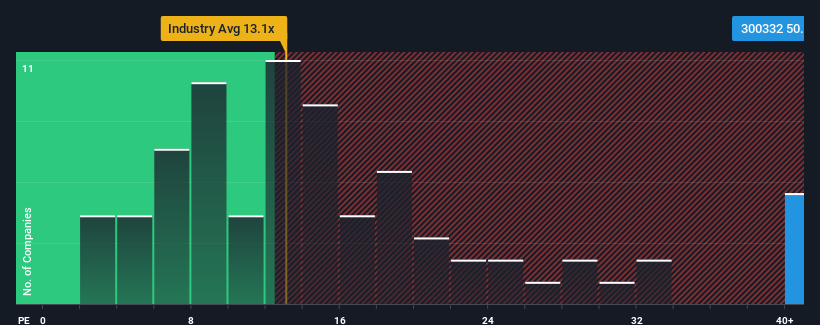

Following the firm bounce in price, Top Resource Energy may be sending very bearish signals at the moment with a price-to-earnings (or "P/E") ratio of 50.4x, since almost half of all companies in China have P/E ratios under 29x and even P/E's lower than 18x are not unusual. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/E.

Top Resource Energy has been struggling lately as its earnings have declined faster than most other companies. It might be that many expect the dismal earnings performance to recover substantially, which has kept the P/E from collapsing. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

See our latest analysis for Top Resource Energy

Does Growth Match The High P/E?

There's an inherent assumption that a company should far outperform the market for P/E ratios like Top Resource Energy's to be considered reasonable.

Retrospectively, the last year delivered a frustrating 74% decrease to the company's bottom line. Even so, admirably EPS has lifted 90% in aggregate from three years ago, notwithstanding the last 12 months. So we can start by confirming that the company has generally done a very good job of growing earnings over that time, even though it had some hiccups along the way.

Shifting to the future, estimates from the three analysts covering the company suggest earnings should grow by 85% per year over the next three years. That's shaping up to be materially higher than the 19% per annum growth forecast for the broader market.

With this information, we can see why Top Resource Energy is trading at such a high P/E compared to the market. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

The Key Takeaway

Top Resource Energy's P/E is flying high just like its stock has during the last month. We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

As we suspected, our examination of Top Resource Energy's analyst forecasts revealed that its superior earnings outlook is contributing to its high P/E. Right now shareholders are comfortable with the P/E as they are quite confident future earnings aren't under threat. Unless these conditions change, they will continue to provide strong support to the share price.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 2 warning signs with Top Resource Energy, and understanding these should be part of your investment process.

You might be able to find a better investment than Top Resource Energy. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Valuation is complex, but we're here to simplify it.

Discover if Top Resource Energy might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:300332

Top Resource Energy

Engages in the trading and sale of natural gas, pipeline transportation, urban gas transmission and distribution, gas engineering design, and technical services.

High growth potential with acceptable track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.3% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.7% overvalued

LI

Community Contributor