Advertisement

- China

- /

- Tech Hardware

- /

- SZSE:002180

Earnings Miss: Ninestar Corporation Missed EPS And Analysts Are Revising Their Forecasts

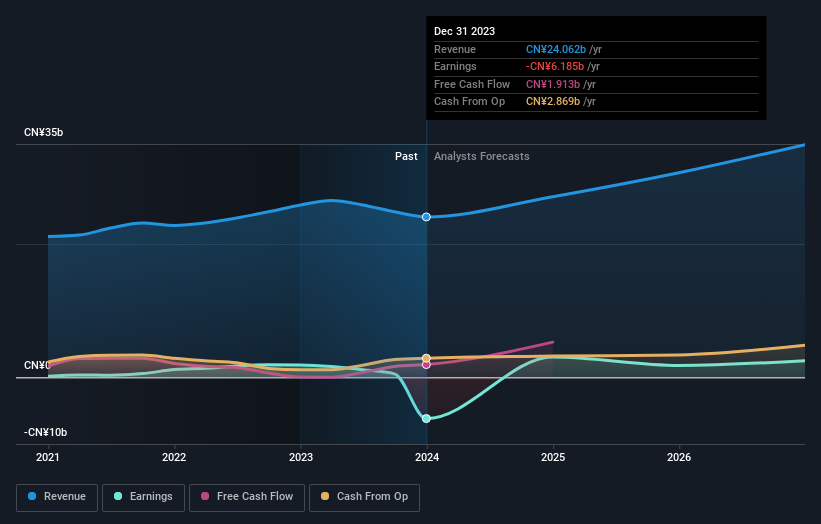

It's been a pretty great week for Ninestar Corporation (SZSE:002180) shareholders, with its shares surging 14% to CN¥25.32 in the week since its latest annual results. Revenues fell 9.9% short of expectations, at CN¥24b. Earnings correspondingly dipped, with Ninestar reporting a statutory loss of CN¥4.40 per share, whereas the analyst had previously modelled a profit in this period. Earnings are an important time for investors, as they can track a company's performance, look at what the analyst is forecasting for next year, and see if there's been a change in sentiment towards the company. So we collected the latest post-earnings statutory consensus estimate to see what could be in store for next year.

Check out our latest analysis for Ninestar

Taking into account the latest results, the current consensus from Ninestar's single analyst is for revenues of CN¥27.1b in 2024. This would reflect a solid 13% increase on its revenue over the past 12 months. Earnings are expected to improve, with Ninestar forecast to report a statutory profit of CN¥2.16 per share. Yet prior to the latest earnings, the analyst had been anticipated revenues of CN¥34.3b and earnings per share (EPS) of CN¥1.92 in 2024. So there's been quite a change-up of views after the latest results, with the analyst making a serious cut to their revenue forecasts while also granting a substantial gain in to the earnings per share numbers.

The analyst has cut their price target 7.8% to CN¥35.16per share, suggesting that the declining revenue was a more crucial indicator than the expected improvement in earnings.

Taking a look at the bigger picture now, one of the ways we can understand these forecasts is to see how they compare to both past performance and industry growth estimates. It's clear from the latest estimates that Ninestar's rate of growth is expected to accelerate meaningfully, with the forecast 13% annualised revenue growth to the end of 2024 noticeably faster than its historical growth of 3.1% p.a. over the past five years. Other similar companies in the industry (with analyst coverage) are also forecast to grow their revenue at 15% per year. Factoring in the forecast acceleration in revenue, it's pretty clear that Ninestar is expected to grow at about the same rate as the wider industry.

The Bottom Line

The biggest takeaway for us is the consensus earnings per share upgrade, which suggests a clear improvement in sentiment around Ninestar's earnings potential next year. Sadly, they also downgraded their revenue forecasts, but the business is still expected to grow at roughly the same rate as the industry itself. With that said, earnings are more important to the long-term value of the business. The consensus price target fell measurably, with the analyst seemingly not reassured by the latest results, leading to a lower estimate of Ninestar's future valuation.

Following on from that line of thought, we think that the long-term prospects of the business are much more relevant than next year's earnings. At least one analyst has provided forecasts out to 2026, which can be seen for free on our platform here.

Plus, you should also learn about the 1 warning sign we've spotted with Ninestar .

Valuation is complex, but we're here to simplify it.

Discover if Ninestar might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:002180

Ninestar

Engages in the research and development, production, processing, and sales of self-produced printers, and printer consumables and accessories.

High growth potential with excellent balance sheet.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor