Advertisement

- China

- /

- Communications

- /

- SZSE:000810

Skyworth Digital Co., Ltd.'s (SZSE:000810) Shares Leap 34% Yet They're Still Not Telling The Full Story

Despite an already strong run, Skyworth Digital Co., Ltd. (SZSE:000810) shares have been powering on, with a gain of 34% in the last thirty days. But the gains over the last month weren't enough to make shareholders whole, as the share price is still down 2.1% in the last twelve months.

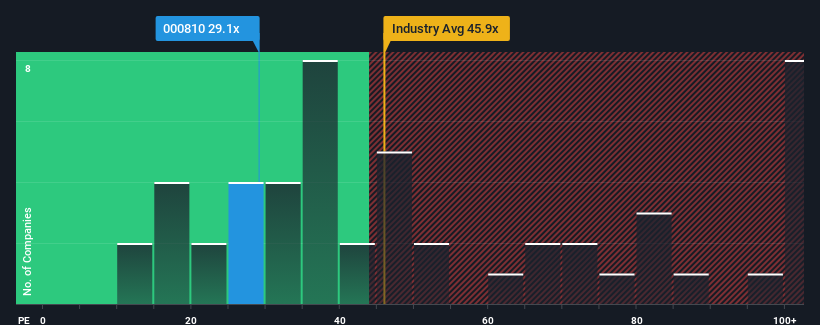

Even after such a large jump in price, there still wouldn't be many who think Skyworth Digital's price-to-earnings (or "P/E") ratio of 29.1x is worth a mention when the median P/E in China is similar at about 32x. Although, it's not wise to simply ignore the P/E without explanation as investors may be disregarding a distinct opportunity or a costly mistake.

With earnings that are retreating more than the market's of late, Skyworth Digital has been very sluggish. It might be that many expect the dismal earnings performance to revert back to market averages soon, which has kept the P/E from falling. If you still like the company, you'd want its earnings trajectory to turn around before making any decisions. Or at the very least, you'd be hoping it doesn't keep underperforming if your plan is to pick up some stock while it's not in favour.

Check out our latest analysis for Skyworth Digital

What Are Growth Metrics Telling Us About The P/E?

The only time you'd be comfortable seeing a P/E like Skyworth Digital's is when the company's growth is tracking the market closely.

Taking a look back first, the company's earnings per share growth last year wasn't something to get excited about as it posted a disappointing decline of 28%. As a result, earnings from three years ago have also fallen 13% overall. Accordingly, shareholders would have felt downbeat about the medium-term rates of earnings growth.

Shifting to the future, estimates from the four analysts covering the company suggest earnings should grow by 27% each year over the next three years. Meanwhile, the rest of the market is forecast to only expand by 18% per annum, which is noticeably less attractive.

With this information, we find it interesting that Skyworth Digital is trading at a fairly similar P/E to the market. It may be that most investors aren't convinced the company can achieve future growth expectations.

The Bottom Line On Skyworth Digital's P/E

Its shares have lifted substantially and now Skyworth Digital's P/E is also back up to the market median. While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

We've established that Skyworth Digital currently trades on a lower than expected P/E since its forecast growth is higher than the wider market. There could be some unobserved threats to earnings preventing the P/E ratio from matching the positive outlook. It appears some are indeed anticipating earnings instability, because these conditions should normally provide a boost to the share price.

And what about other risks? Every company has them, and we've spotted 2 warning signs for Skyworth Digital (of which 1 shouldn't be ignored!) you should know about.

If you're unsure about the strength of Skyworth Digital's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:000810

Skyworth Digital

Provides home video entertainment and intelligent connectivity solutions in China and internationally.

Excellent balance sheet with moderate growth potential.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor