Beijing Thunisoft (SZSE:300271 investor three-year losses grow to 75% as the stock sheds CN¥422m this past week

As every investor would know, not every swing hits the sweet spot. But you have a problem if you face massive losses more than once in a while. So consider, for a moment, the misfortune of Beijing Thunisoft Co., Ltd. (SZSE:300271) investors who have held the stock for three years as it declined a whopping 75%. That would be a disturbing experience. And the ride hasn't got any smoother in recent times over the last year, with the price 50% lower in that time. Furthermore, it's down 22% in about a quarter. That's not much fun for holders.

Since Beijing Thunisoft has shed CN¥422m from its value in the past 7 days, let's see if the longer term decline has been driven by the business' economics.

See our latest analysis for Beijing Thunisoft

Beijing Thunisoft wasn't profitable in the last twelve months, it is unlikely we'll see a strong correlation between its share price and its earnings per share (EPS). Arguably revenue is our next best option. Generally speaking, companies without profits are expected to grow revenue every year, and at a good clip. That's because fast revenue growth can be easily extrapolated to forecast profits, often of considerable size.

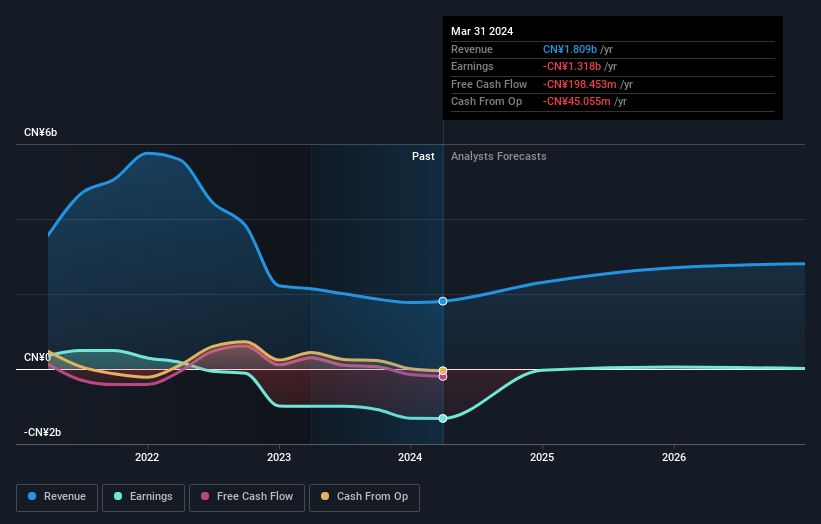

In the last three years Beijing Thunisoft saw its revenue shrink by 37% per year. That's definitely a weaker result than most pre-profit companies report. The swift share price decline at an annual compound rate of 21%, reflects this weak fundamental performance. We prefer leave it to clowns to try to catch falling knives, like this stock. There is a good reason that investors often describe buying a sharply falling stock price as 'trying to catch a falling knife'. Think about it.

You can see below how earnings and revenue have changed over time (discover the exact values by clicking on the image).

We're pleased to report that the CEO is remunerated more modestly than most CEOs at similarly capitalized companies. But while CEO remuneration is always worth checking, the really important question is whether the company can grow earnings going forward. You can see what analysts are predicting for Beijing Thunisoft in this interactive graph of future profit estimates.

A Different Perspective

We regret to report that Beijing Thunisoft shareholders are down 50% for the year. Unfortunately, that's worse than the broader market decline of 12%. Having said that, it's inevitable that some stocks will be oversold in a falling market. The key is to keep your eyes on the fundamental developments. Regrettably, last year's performance caps off a bad run, with the shareholders facing a total loss of 12% per year over five years. We realise that Baron Rothschild has said investors should "buy when there is blood on the streets", but we caution that investors should first be sure they are buying a high quality business. I find it very interesting to look at share price over the long term as a proxy for business performance. But to truly gain insight, we need to consider other information, too. Take risks, for example - Beijing Thunisoft has 1 warning sign we think you should be aware of.

If you like to buy stocks alongside management, then you might just love this free list of companies. (Hint: many of them are unnoticed AND have attractive valuation).

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on Chinese exchanges.

Valuation is complex, but we're here to simplify it.

Discover if Beijing Thunisoft might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:300271

Beijing Thunisoft

Provides software and information technology services to the government and enterprise customers in China.

Flawless balance sheet and slightly overvalued.