Advertisement

Shanghai Newtouch Software Co., Ltd. (SHSE:688590) Not Doing Enough For Some Investors As Its Shares Slump 30%

Shanghai Newtouch Software Co., Ltd. (SHSE:688590) shareholders won't be pleased to see that the share price has had a very rough month, dropping 30% and undoing the prior period's positive performance. Longer-term, the stock has been solid despite a difficult 30 days, gaining 19% in the last year.

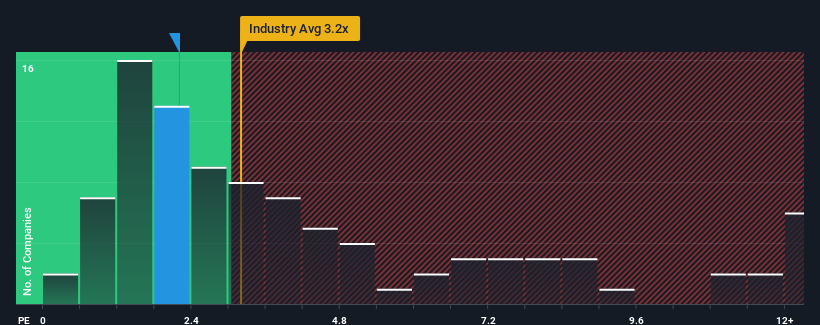

Although its price has dipped substantially, Shanghai Newtouch Software's price-to-sales (or "P/S") ratio of 2.2x might still make it look like a buy right now compared to the IT industry in China, where around half of the companies have P/S ratios above 3.2x and even P/S above 7x are quite common. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the reduced P/S.

View our latest analysis for Shanghai Newtouch Software

What Does Shanghai Newtouch Software's Recent Performance Look Like?

Shanghai Newtouch Software has been doing a good job lately as it's been growing revenue at a solid pace. One possibility is that the P/S is low because investors think this respectable revenue growth might actually underperform the broader industry in the near future. Those who are bullish on Shanghai Newtouch Software will be hoping that this isn't the case, so that they can pick up the stock at a lower valuation.

Want the full picture on earnings, revenue and cash flow for the company? Then our free report on Shanghai Newtouch Software will help you shine a light on its historical performance.How Is Shanghai Newtouch Software's Revenue Growth Trending?

The only time you'd be truly comfortable seeing a P/S as low as Shanghai Newtouch Software's is when the company's growth is on track to lag the industry.

If we review the last year of revenue growth, the company posted a terrific increase of 28%. Pleasingly, revenue has also lifted 57% in aggregate from three years ago, thanks to the last 12 months of growth. So we can start by confirming that the company has done a great job of growing revenue over that time.

This is in contrast to the rest of the industry, which is expected to grow by 34% over the next year, materially higher than the company's recent medium-term annualised growth rates.

With this in consideration, it's easy to understand why Shanghai Newtouch Software's P/S falls short of the mark set by its industry peers. Apparently many shareholders weren't comfortable holding on to something they believe will continue to trail the wider industry.

The Final Word

The southerly movements of Shanghai Newtouch Software's shares means its P/S is now sitting at a pretty low level. It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

In line with expectations, Shanghai Newtouch Software maintains its low P/S on the weakness of its recent three-year growth being lower than the wider industry forecast. Right now shareholders are accepting the low P/S as they concede future revenue probably won't provide any pleasant surprises. If recent medium-term revenue trends continue, it's hard to see the share price experience a reversal of fortunes anytime soon.

Before you take the next step, you should know about the 3 warning signs for Shanghai Newtouch Software (1 is a bit concerning!) that we have uncovered.

It's important to make sure you look for a great company, not just the first idea you come across. So if growing profitability aligns with your idea of a great company, take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:688590

Shanghai Newtouch Software

Operates as a software and information technology services company in China.

High growth potential and fair value.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor