Advertisement

Yonyou Auto Information Technology (Shanghai) Co.,Ltd's (SHSE:688479) Shares Climb 28% But Its Business Is Yet to Catch Up

Yonyou Auto Information Technology (Shanghai) Co.,Ltd (SHSE:688479) shareholders would be excited to see that the share price has had a great month, posting a 28% gain and recovering from prior weakness. Looking further back, the 22% rise over the last twelve months isn't too bad notwithstanding the strength over the last 30 days.

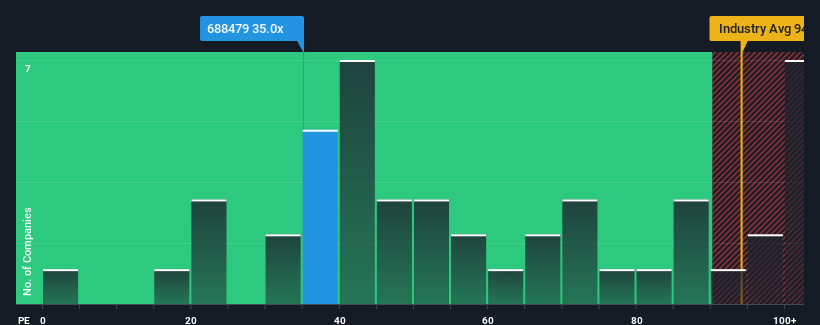

Although its price has surged higher, you could still be forgiven for feeling indifferent about Yonyou Auto Information Technology (Shanghai)Ltd's P/E ratio of 35x, since the median price-to-earnings (or "P/E") ratio in China is also close to 36x. Although, it's not wise to simply ignore the P/E without explanation as investors may be disregarding a distinct opportunity or a costly mistake.

For example, consider that Yonyou Auto Information Technology (Shanghai)Ltd's financial performance has been poor lately as its earnings have been in decline. It might be that many expect the company to put the disappointing earnings performance behind them over the coming period, which has kept the P/E from falling. If not, then existing shareholders may be a little nervous about the viability of the share price.

View our latest analysis for Yonyou Auto Information Technology (Shanghai)Ltd

Is There Some Growth For Yonyou Auto Information Technology (Shanghai)Ltd?

There's an inherent assumption that a company should be matching the market for P/E ratios like Yonyou Auto Information Technology (Shanghai)Ltd's to be considered reasonable.

If we review the last year of earnings, dishearteningly the company's profits fell to the tune of 27%. The last three years don't look nice either as the company has shrunk EPS by 49% in aggregate. Therefore, it's fair to say the earnings growth recently has been undesirable for the company.

Comparing that to the market, which is predicted to deliver 38% growth in the next 12 months, the company's downward momentum based on recent medium-term earnings results is a sobering picture.

In light of this, it's somewhat alarming that Yonyou Auto Information Technology (Shanghai)Ltd's P/E sits in line with the majority of other companies. It seems most investors are ignoring the recent poor growth rate and are hoping for a turnaround in the company's business prospects. There's a good chance existing shareholders are setting themselves up for future disappointment if the P/E falls to levels more in line with the recent negative growth rates.

The Bottom Line On Yonyou Auto Information Technology (Shanghai)Ltd's P/E

Yonyou Auto Information Technology (Shanghai)Ltd appears to be back in favour with a solid price jump getting its P/E back in line with most other companies. We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

We've established that Yonyou Auto Information Technology (Shanghai)Ltd currently trades on a higher than expected P/E since its recent earnings have been in decline over the medium-term. Right now we are uncomfortable with the P/E as this earnings performance is unlikely to support a more positive sentiment for long. If recent medium-term earnings trends continue, it will place shareholders' investments at risk and potential investors in danger of paying an unnecessary premium.

You should always think about risks. Case in point, we've spotted 2 warning signs for Yonyou Auto Information Technology (Shanghai)Ltd you should be aware of, and 1 of them is potentially serious.

If you're unsure about the strength of Yonyou Auto Information Technology (Shanghai)Ltd's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:688479

Yonyou Auto Information Technology (Shanghai)Ltd

Provides digital solutions, software and cloud services in China.

Flawless balance sheet with slight risk.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor