Advertisement

- China

- /

- Semiconductors

- /

- SZSE:300861

Yangling Metron New Material (SZSE:300861) Is Paying Out Less In Dividends Than Last Year

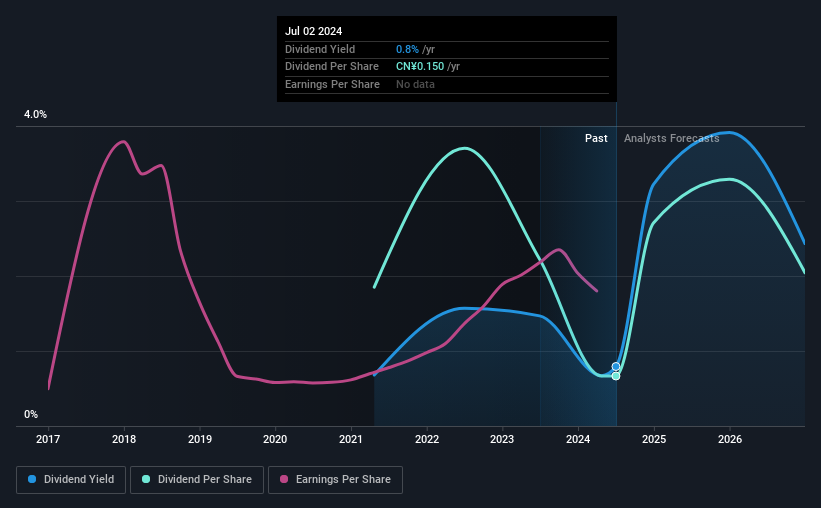

Yangling Metron New Material Inc. (SZSE:300861) is reducing its dividend from last year's comparable payment to CN¥0.15 on the 5th of July. This means that the dividend yield is 0.8%, which is a bit low when comparing to other companies in the industry.

While the dividend yield is important for income investors, it is also important to consider any large share price moves, as this will generally outweigh any gains from distributions. Yangling Metron New Material's stock price has reduced by 33% in the last 3 months, which is not ideal for investors and can explain a sharp increase in the dividend yield.

Check out our latest analysis for Yangling Metron New Material

Yangling Metron New Material's Dividend Is Well Covered By Earnings

It would be nice for the yield to be higher, but we should also check if higher levels of dividend payment would be sustainable. However, Yangling Metron New Material's earnings easily cover the dividend. This means that most of its earnings are being retained to grow the business.

Over the next year, EPS is forecast to fall by 29.4%. If the dividend continues along recent trends, we estimate the payout ratio could be 5.4%, which we consider to be quite comfortable, with most of the company's earnings left over to grow the business in the future.

Yangling Metron New Material's Dividend Has Lacked Consistency

The track record isn't the longest, but we are already seeing a bit of instability in the payments. The annual payment during the last 3 years was CN¥0.417 in 2021, and the most recent fiscal year payment was CN¥0.15. This works out to a decline of approximately 64% over that time. Declining dividends isn't generally what we look for as they can indicate that the company is running into some challenges.

The Dividend Has Growth Potential

Given that dividend payments have been shrinking like a glacier in a warming world, we need to check if there are some bright spots on the horizon. Yangling Metron New Material has seen EPS rising for the last five years, at 9.9% per annum. Growth in EPS bodes well for the dividend, as does the low payout ratio that the company is currently reporting.

We Really Like Yangling Metron New Material's Dividend

It is generally not great to see the dividend being cut, but we don't think this should happen much if at all in the future given that Yangling Metron New Material has the makings of a solid income stock moving forward. The cut will allow the company to continue paying out the dividend without putting the balance sheet under pressure, which means that it could remain sustainable for longer. All of these factors considered, we think this has solid potential as a dividend stock.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. To that end, Yangling Metron New Material has 3 warning signs (and 2 which don't sit too well with us) we think you should know about. Is Yangling Metron New Material not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SZSE:300861

Yangling Metron New Material

Researches, develops, manufactures, and sells electroplated diamond wires and other superhard diamond tools in China and internationally.

Excellent balance sheet with reasonable growth potential.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.3% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.7% overvalued

LI

Community Contributor