- China

- /

- Semiconductors

- /

- SZSE:300672

The five-year decline in earnings might be taking its toll on Hunan Goke MicroelectronicsLtd (SZSE:300672) shareholders as stock falls 6.0% over the past week

It might be of some concern to shareholders to see the Hunan Goke Microelectronics Co.,Ltd. (SZSE:300672) share price down 19% in the last month. But that doesn't change the fact that the returns over the last five years have been pleasing. After all, the share price is up a market-beating 64% in that time. While the long term returns are impressive, we do have some sympathy for those who bought more recently, given the 41% drop, in the last year.

While this past week has detracted from the company's five-year return, let's look at the recent trends of the underlying business and see if the gains have been in alignment.

Check out our latest analysis for Hunan Goke MicroelectronicsLtd

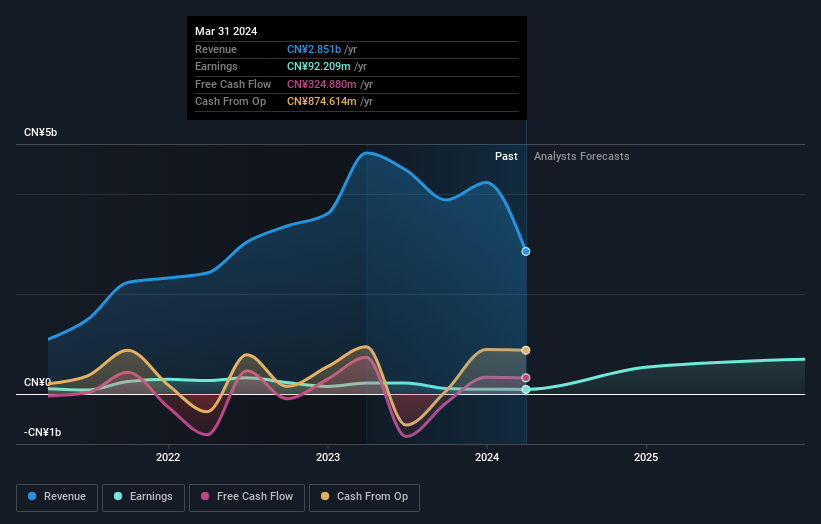

We don't think that Hunan Goke MicroelectronicsLtd's modest trailing twelve month profit has the market's full attention at the moment. We think revenue is probably a better guide. Generally speaking, we'd consider a stock like this alongside loss-making companies, simply because the quantum of the profit is so low. For shareholders to have confidence a company will grow profits significantly, it must grow revenue.

In the last 5 years Hunan Goke MicroelectronicsLtd saw its revenue grow at 43% per year. Even measured against other revenue-focussed companies, that's a good result. While the compound gain of 10% per year is good, it's not unreasonable given the strong revenue growth. If the strong revenue growth continues, we'd hope to see the share price to follow, in time. Opportunity lies where the market hasn't fully priced growth in the underlying business.

You can see below how earnings and revenue have changed over time (discover the exact values by clicking on the image).

You can see how its balance sheet has strengthened (or weakened) over time in this free interactive graphic.

What About Dividends?

As well as measuring the share price return, investors should also consider the total shareholder return (TSR). The TSR incorporates the value of any spin-offs or discounted capital raisings, along with any dividends, based on the assumption that the dividends are reinvested. So for companies that pay a generous dividend, the TSR is often a lot higher than the share price return. As it happens, Hunan Goke MicroelectronicsLtd's TSR for the last 5 years was 67%, which exceeds the share price return mentioned earlier. This is largely a result of its dividend payments!

A Different Perspective

We regret to report that Hunan Goke MicroelectronicsLtd shareholders are down 40% for the year (even including dividends). Unfortunately, that's worse than the broader market decline of 18%. Having said that, it's inevitable that some stocks will be oversold in a falling market. The key is to keep your eyes on the fundamental developments. Longer term investors wouldn't be so upset, since they would have made 11%, each year, over five years. It could be that the recent sell-off is an opportunity, so it may be worth checking the fundamental data for signs of a long term growth trend. While it is well worth considering the different impacts that market conditions can have on the share price, there are other factors that are even more important. Even so, be aware that Hunan Goke MicroelectronicsLtd is showing 2 warning signs in our investment analysis , you should know about...

We will like Hunan Goke MicroelectronicsLtd better if we see some big insider buys. While we wait, check out this free list of undervalued stocks (mostly small caps) with considerable, recent, insider buying.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on Chinese exchanges.

Valuation is complex, but we're here to simplify it.

Discover if Hunan Goke MicroelectronicsLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SZSE:300672

Hunan Goke MicroelectronicsLtd

Engages in the research and development of integrated circuit chips in China.

Adequate balance sheet with moderate growth potential.