- China

- /

- Semiconductors

- /

- SHSE:688478

Shenzhen Kiwi Instruments And 2 Insider Picks For Promising Growth

Reviewed by Simply Wall St

As global markets navigate a landscape marked by interest rate adjustments and mixed economic indicators, investors are increasingly turning their attention to growth companies with strong insider ownership as potential opportunities. In this environment, stocks like Shenzhen Kiwi Instruments exemplify the appeal of businesses where insiders have significant stakes, suggesting alignment with shareholder interests and confidence in the company's future prospects.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| Lavvi Empreendimentos Imobiliários (BOVESPA:LAVV3) | 11.9% | 21.1% |

| Archean Chemical Industries (NSEI:ACI) | 22.9% | 34% |

| Kirloskar Pneumatic (BSE:505283) | 30.3% | 30.1% |

| People & Technology (KOSDAQ:A137400) | 16.4% | 35.6% |

| Arctech Solar Holding (SHSE:688408) | 37.8% | 29.8% |

| Seojin SystemLtd (KOSDAQ:A178320) | 30.7% | 49.1% |

| Medley (TSE:4480) | 34% | 30.4% |

| HANA Micron (KOSDAQ:A067310) | 18.3% | 105.8% |

| Adveritas (ASX:AV1) | 21.2% | 144.2% |

| Plenti Group (ASX:PLT) | 12.8% | 106.4% |

Let's take a closer look at a couple of our picks from the screened companies.

Shenzhen Kiwi Instruments (SHSE:688045)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Shenzhen Kiwi Instruments Co., Ltd. develops and sells analog and mixed-signal power management integrated circuits, with a market cap of CN¥2.31 billion.

Operations: The company generates revenue of CN¥580.64 million from its semiconductors segment.

Insider Ownership: 38.2%

Earnings Growth Forecast: 91.8% p.a.

Shenzhen Kiwi Instruments is poised for significant growth, with revenue expected to increase by 24.1% annually, surpassing the Chinese market's average. Despite a recent net loss of CNY 10.61 million and volatile share prices, the company is forecast to become profitable within three years and achieve earnings growth of 91.82% per year. Insider ownership remains stable with no substantial insider trading activity reported recently, while a completed buyback reflects shareholder confidence.

- Click here and access our complete growth analysis report to understand the dynamics of Shenzhen Kiwi Instruments.

- Our comprehensive valuation report raises the possibility that Shenzhen Kiwi Instruments is priced higher than what may be justified by its financials.

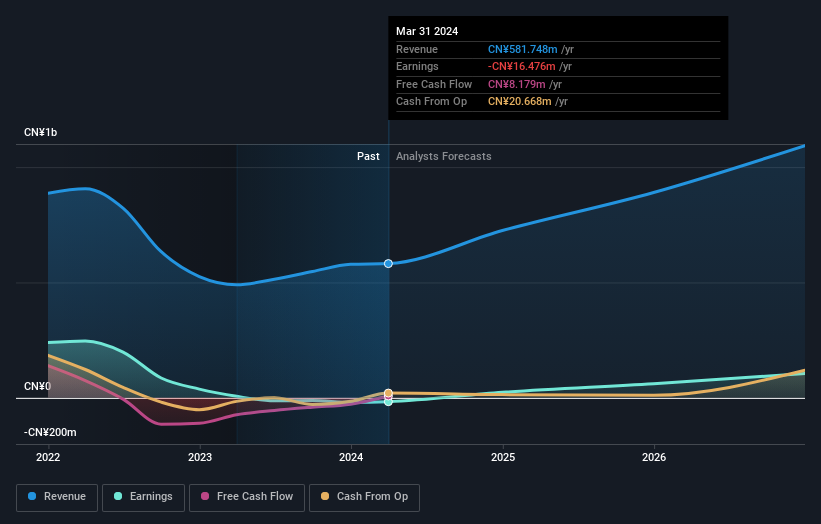

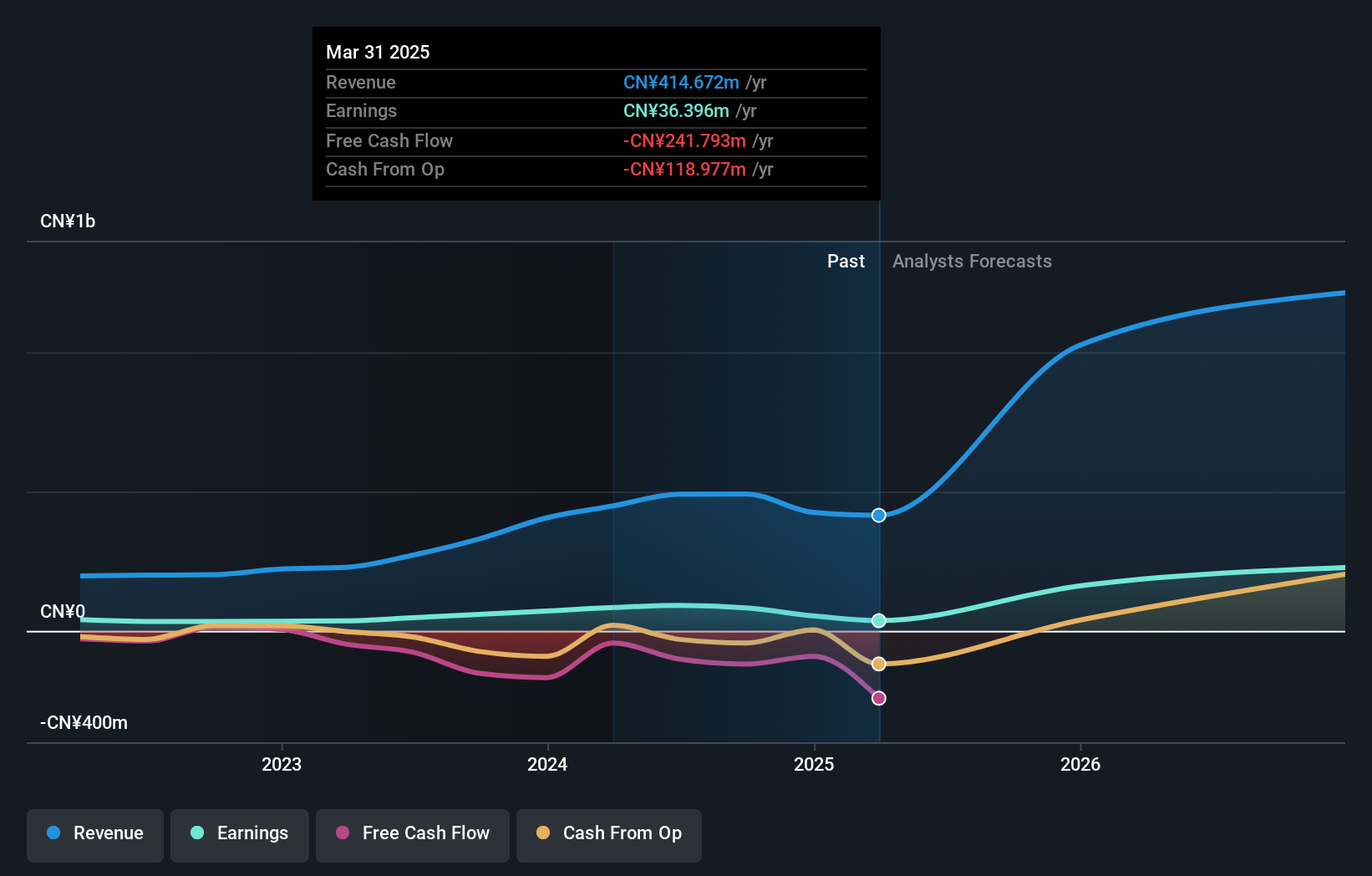

Crystal Growth & Energy EquipmentLtd (SHSE:688478)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Crystal Growth & Energy Equipment Co., Ltd. operates in the field of crystal growth and energy equipment, with a market capitalization of CN¥4.27 billion.

Operations: Crystal Growth & Energy Equipment Co., Ltd. derives its revenue from various segments related to crystal growth and energy equipment.

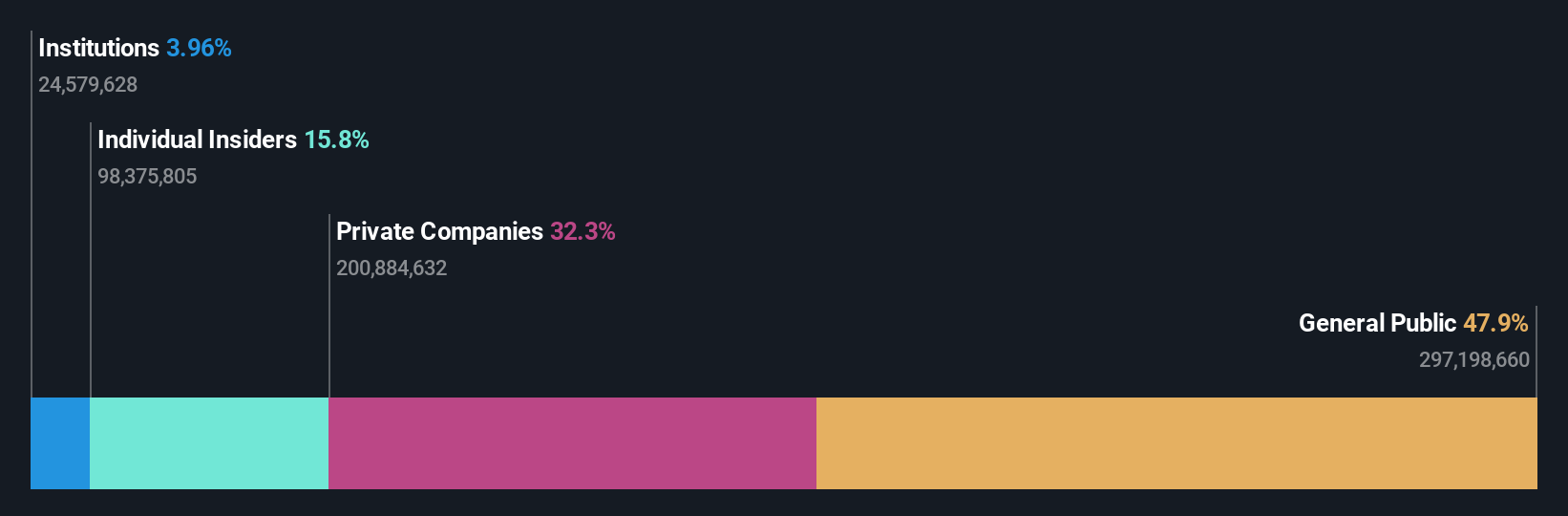

Insider Ownership: 25%

Earnings Growth Forecast: 31% p.a.

Crystal Growth & Energy Equipment Ltd. anticipates robust growth, with earnings projected to rise 31% annually, outpacing the CN market. Revenue is also expected to grow at a similar rate. Despite high share price volatility recently, the company reported significant revenue and net income increases for H1 2024 compared to last year. The completion of a share buyback program totaling CNY 49.27 million underscores management's confidence in its future prospects amidst stable insider ownership levels.

- Get an in-depth perspective on Crystal Growth & Energy EquipmentLtd's performance by reading our analyst estimates report here.

- The analysis detailed in our Crystal Growth & Energy EquipmentLtd valuation report hints at an deflated share price compared to its estimated value.

Jiangsu Huahong Technology (SZSE:002645)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Jiangsu Huahong Technology Co., Ltd. is involved in the research, development, manufacturing, marketing, and servicing of renewable resource processing equipment both in China and internationally, with a market cap of CN¥4.53 billion.

Operations: The company generates revenue through its core activities of developing, producing, promoting, and maintaining equipment for processing renewable resources in both domestic and international markets.

Insider Ownership: 18.7%

Earnings Growth Forecast: 74.6% p.a.

Jiangsu Huahong Technology has shown a turnaround with a net income of CNY 2.22 million for H1 2024, recovering from a previous loss. The company's revenue is forecast to grow by 18.7% annually, surpassing the market average, while earnings are expected to rise significantly at 74.6% per year over the next three years. Trading at a substantial discount to its estimated fair value, it presents an attractive valuation despite low forecasted return on equity.

- Click to explore a detailed breakdown of our findings in Jiangsu Huahong Technology's earnings growth report.

- Our expertly prepared valuation report Jiangsu Huahong Technology implies its share price may be lower than expected.

Make It Happen

- Take a closer look at our Fast Growing Companies With High Insider Ownership list of 1485 companies by clicking here.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SHSE:688478

Crystal Growth & Energy EquipmentLtd

Crystal Growth & Energy Equipment Co.,Ltd.

Flawless balance sheet with high growth potential.