Advertisement

- China

- /

- Real Estate

- /

- SHSE:600848

Shanghai Lingang HoldingsLtd (SHSE:600848) Use Of Debt Could Be Considered Risky

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that Shanghai Lingang Holdings Co.,Ltd. (SHSE:600848) does use debt in its business. But the more important question is: how much risk is that debt creating?

Why Does Debt Bring Risk?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

View our latest analysis for Shanghai Lingang HoldingsLtd

How Much Debt Does Shanghai Lingang HoldingsLtd Carry?

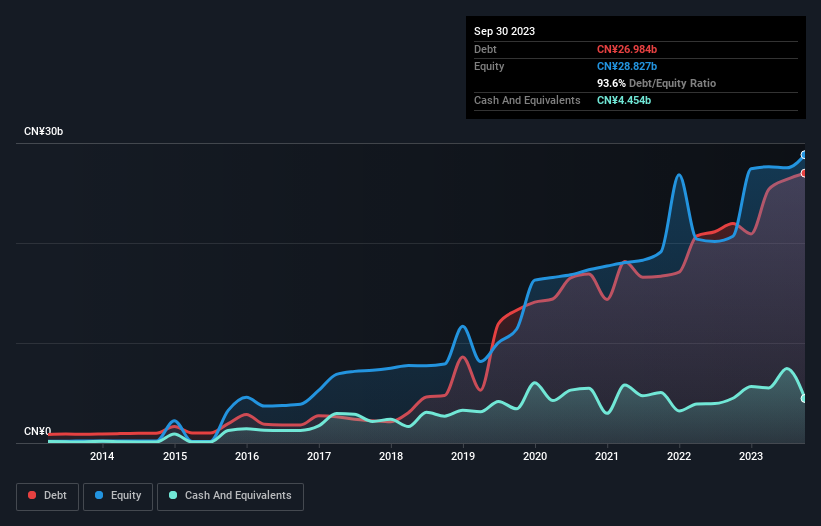

As you can see below, at the end of September 2023, Shanghai Lingang HoldingsLtd had CN¥27.0b of debt, up from CN¥21.9b a year ago. Click the image for more detail. However, it also had CN¥4.45b in cash, and so its net debt is CN¥22.5b.

A Look At Shanghai Lingang HoldingsLtd's Liabilities

The latest balance sheet data shows that Shanghai Lingang HoldingsLtd had liabilities of CN¥29.4b due within a year, and liabilities of CN¥18.0b falling due after that. Offsetting these obligations, it had cash of CN¥4.45b as well as receivables valued at CN¥407.2m due within 12 months. So its liabilities total CN¥42.5b more than the combination of its cash and short-term receivables.

This deficit casts a shadow over the CN¥25.4b company, like a colossus towering over mere mortals. So we definitely think shareholders need to watch this one closely. After all, Shanghai Lingang HoldingsLtd would likely require a major re-capitalisation if it had to pay its creditors today.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Shanghai Lingang HoldingsLtd has a rather high debt to EBITDA ratio of 8.2 which suggests a meaningful debt load. But the good news is that it boasts fairly comforting interest cover of 6.4 times, suggesting it can responsibly service its obligations. Unfortunately, Shanghai Lingang HoldingsLtd saw its EBIT slide 5.7% in the last twelve months. If that earnings trend continues then its debt load will grow heavy like the heart of a polar bear watching its sole cub. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Shanghai Lingang HoldingsLtd can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So it's worth checking how much of that EBIT is backed by free cash flow. Over the last three years, Shanghai Lingang HoldingsLtd saw substantial negative free cash flow, in total. While that may be a result of expenditure for growth, it does make the debt far more risky.

Our View

On the face of it, Shanghai Lingang HoldingsLtd's conversion of EBIT to free cash flow left us tentative about the stock, and its level of total liabilities was no more enticing than the one empty restaurant on the busiest night of the year. But at least it's pretty decent at covering its interest expense with its EBIT; that's encouraging. After considering the datapoints discussed, we think Shanghai Lingang HoldingsLtd has too much debt. That sort of riskiness is ok for some, but it certainly doesn't float our boat. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. These risks can be hard to spot. Every company has them, and we've spotted 2 warning signs for Shanghai Lingang HoldingsLtd (of which 1 can't be ignored!) you should know about.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:600848

Shanghai Lingang HoldingsLtd

Develops and sells industrial carriers in China.

Proven track record with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.2% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.7% overvalued

LI

Community Contributor