- China

- /

- Life Sciences

- /

- SZSE:300759

Earnings are growing at Pharmaron Beijing (SZSE:300759) but shareholders still don't like its prospects

Pharmaron Beijing Co., Ltd. (SZSE:300759) shareholders should be happy to see the share price up 10% in the last month. But only the myopic could ignore the astounding decline over three years. The share price has sunk like a leaky ship, down 73% in that time. So it sure is nice to see a bit of an improvement. But the more important question is whether the underlying business can justify a higher price still.

Given the past week has been tough on shareholders, let's investigate the fundamentals and see what we can learn.

Check out our latest analysis for Pharmaron Beijing

There is no denying that markets are sometimes efficient, but prices do not always reflect underlying business performance. One way to examine how market sentiment has changed over time is to look at the interaction between a company's share price and its earnings per share (EPS).

During the unfortunate three years of share price decline, Pharmaron Beijing actually saw its earnings per share (EPS) improve by 4.0% per year. This is quite a puzzle, and suggests there might be something temporarily buoying the share price. Alternatively, growth expectations may have been unreasonable in the past.

It looks to us like the market was probably too optimistic around growth three years ago. But it's possible a look at other metrics will be enlightening.

The modest 0.9% dividend yield is unlikely to be guiding the market view of the stock. Revenue is actually up 24% over the three years, so the share price drop doesn't seem to hinge on revenue, either. This analysis is just perfunctory, but it might be worth researching Pharmaron Beijing more closely, as sometimes stocks fall unfairly. This could present an opportunity.

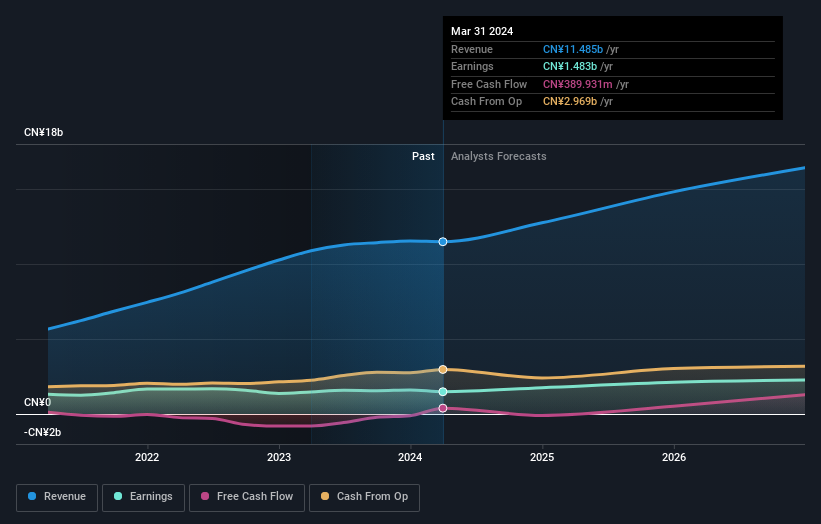

You can see how earnings and revenue have changed over time in the image below (click on the chart to see the exact values).

Pharmaron Beijing is well known by investors, and plenty of clever analysts have tried to predict the future profit levels. You can see what analysts are predicting for Pharmaron Beijing in this interactive graph of future profit estimates.

A Different Perspective

While the broader market lost about 10% in the twelve months, Pharmaron Beijing shareholders did even worse, losing 29% (even including dividends). However, it could simply be that the share price has been impacted by broader market jitters. It might be worth keeping an eye on the fundamentals, in case there's a good opportunity. On the bright side, long term shareholders have made money, with a gain of 6% per year over half a decade. It could be that the recent sell-off is an opportunity, so it may be worth checking the fundamental data for signs of a long term growth trend. I find it very interesting to look at share price over the long term as a proxy for business performance. But to truly gain insight, we need to consider other information, too. Even so, be aware that Pharmaron Beijing is showing 1 warning sign in our investment analysis , you should know about...

If you would prefer to check out another company -- one with potentially superior financials -- then do not miss this free list of companies that have proven they can grow earnings.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on Chinese exchanges.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:300759

Pharmaron Beijing

Provides drug research and development, and production services to the life sciences industry in North America, Europe, Japan, Mainland China, and internationally.

Undervalued with excellent balance sheet.