Top Chinese Growth Companies With High Insider Ownership August 2024

Reviewed by Simply Wall St

Amid a backdrop of mixed economic indicators and cautious investor sentiment, the Chinese market has shown resilience with key indices displaying varied performance. Despite challenges in manufacturing and domestic demand, certain growth companies with high insider ownership have managed to capture investor interest. In this environment, stocks with strong insider ownership can be particularly appealing as they often indicate confidence from those closest to the company’s operations. Here are three top Chinese growth companies that exemplify this trend as of August 2024.

Top 10 Growth Companies With High Insider Ownership In China

| Name | Insider Ownership | Earnings Growth |

| Ningbo Sunrise Elc TechnologyLtd (SZSE:002937) | 24.3% | 27.7% |

| ShenZhen Woer Heat-Shrinkable MaterialLtd (SZSE:002130) | 19% | 27.9% |

| Cubic Sensor and InstrumentLtd (SHSE:688665) | 10.1% | 34.3% |

| Arctech Solar Holding (SHSE:688408) | 38.7% | 28.4% |

| KEBODA TECHNOLOGY (SHSE:603786) | 12.8% | 25.1% |

| Suzhou Sunmun Technology (SZSE:300522) | 36.5% | 63.4% |

| Eoptolink Technology (SZSE:300502) | 26.7% | 39.4% |

| Sineng ElectricLtd (SZSE:300827) | 36.5% | 39.8% |

| UTour Group (SZSE:002707) | 23% | 36.1% |

| Fujian Wanchen Biotechnology Group (SZSE:300972) | 14.9% | 82.1% |

Here's a peek at a few of the choices from the screener.

Hunan Fangsheng Pharmaceutical (SHSE:603998)

Simply Wall St Growth Rating: ★★★★☆☆

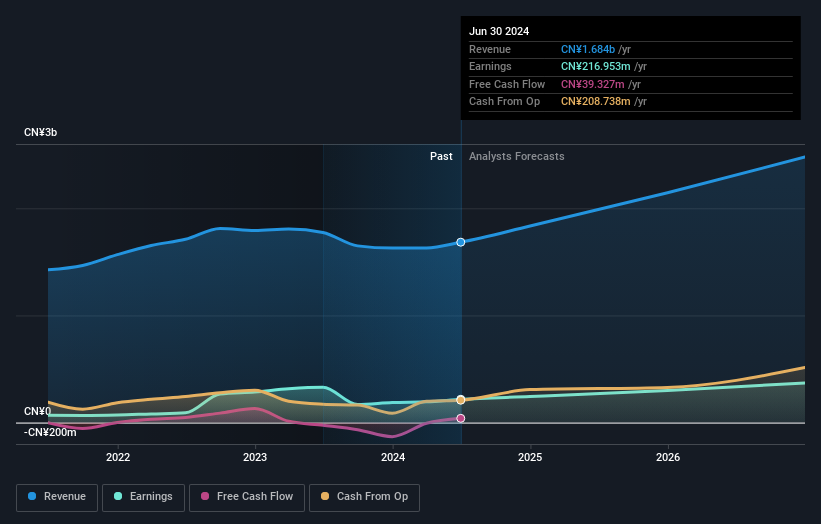

Overview: Hunan Fangsheng Pharmaceutical Co., Ltd. researches, develops, produces, and sells pharmaceutical products in China and has a market cap of CN¥4.85 billion.

Operations: The company's revenue segments include the research, development, production, and sale of pharmaceutical products in China.

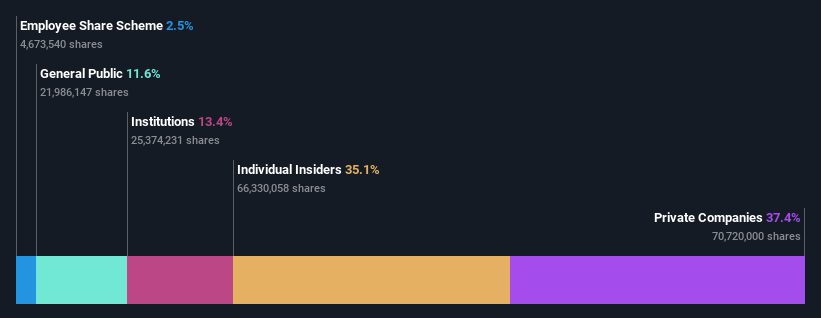

Insider Ownership: 37.1%

Revenue Growth Forecast: 15.3% p.a.

Hunan Fangsheng Pharmaceutical demonstrates notable growth potential with forecasted annual earnings growth of 22.58% over the next three years, outpacing the Chinese market's average. Despite a lower profit margin this year (11.9% vs. 17.5%), its price-to-earnings ratio of 25.1x remains attractive compared to the broader CN market at 28x. However, revenue growth is projected at a modest 15.3% annually, and return on equity is expected to be low at 16.7%.

- Unlock comprehensive insights into our analysis of Hunan Fangsheng Pharmaceutical stock in this growth report.

- The analysis detailed in our Hunan Fangsheng Pharmaceutical valuation report hints at an inflated share price compared to its estimated value.

Jiangsu Jibeier Pharmaceutical (SHSE:688566)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Jiangsu Jibeier Pharmaceutical Co., Ltd. is a pharmaceutical company involved in the research, development, production, and sale of chemical pharmaceutical preparations, Chinese medicine, and drugs with a market cap of CN¥4.17 billion.

Operations: The company's revenue is primarily derived from its Pharmaceutical Manufacturing segment, which generated CN¥889.82 million.

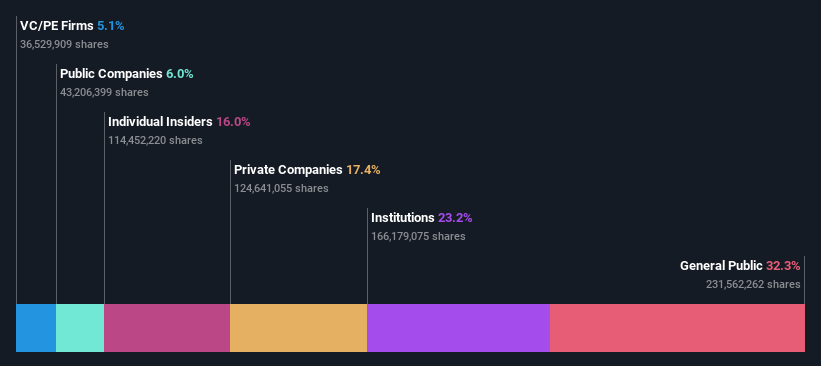

Insider Ownership: 35.1%

Revenue Growth Forecast: 20.8% p.a.

Jiangsu Jibeier Pharmaceutical exhibits strong growth potential with forecasted annual revenue growth of 20.8%, surpassing the Chinese market average. Earnings are projected to grow significantly at 21.24% per year, although slightly below market expectations. The company's price-to-earnings ratio of 17.9x indicates good value relative to peers, despite a low return on equity forecast (14.6%). Recent private placements raised CNY 188 million, reflecting confidence in future prospects despite dividend coverage concerns.

- Delve into the full analysis future growth report here for a deeper understanding of Jiangsu Jibeier Pharmaceutical.

- Upon reviewing our latest valuation report, Jiangsu Jibeier Pharmaceutical's share price might be too pessimistic.

Ninebot (SHSE:689009)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Ninebot Limited designs, develops, produces, sells, and services transportation and robot products globally with a market cap of CN¥31.94 billion.

Operations: Ninebot Limited generates revenue through the design, development, production, sale, and servicing of transportation and robot products worldwide.

Insider Ownership: 16.8%

Revenue Growth Forecast: 22.3% p.a.

Ninebot Limited demonstrates strong growth potential with earnings expected to grow 27.03% annually, significantly outpacing the Chinese market average of 22.1%. Revenue is also forecasted to rise by 22.3% per year, exceeding market expectations of 13.5%. Despite a low return on equity forecast (17.8%) and large one-off items impacting financial results, insider ownership remains high with no substantial insider selling or buying in the past three months.

- Dive into the specifics of Ninebot here with our thorough growth forecast report.

- In light of our recent valuation report, it seems possible that Ninebot is trading beyond its estimated value.

Where To Now?

- Get an in-depth perspective on all 363 Fast Growing Chinese Companies With High Insider Ownership by using our screener here.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Ninebot might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SHSE:689009

Ninebot

Engages in the design, research and development, production, sale, and servicing of transportation and robot products worldwide.

Flawless balance sheet with high growth potential.