As global markets navigate a landscape marked by rate cuts from the European Central Bank and mixed economic signals, U.S. indices like the S&P 500 and Nasdaq Composite have shown resilience, buoyed by sectors such as utilities and real estate, alongside robust earnings reports. In this environment of cautious optimism, growth companies with high insider ownership can offer unique insights into potential long-term value creation, as insiders often possess a deeper understanding of their company's prospects amidst evolving market conditions.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| Kirloskar Pneumatic (BSE:505283) | 30.3% | 30.1% |

| Clinuvel Pharmaceuticals (ASX:CUV) | 10.4% | 27.4% |

| People & Technology (KOSDAQ:A137400) | 16.4% | 35.6% |

| Medley (TSE:4480) | 34% | 30.4% |

| Seojin SystemLtd (KOSDAQ:A178320) | 30.7% | 49.1% |

| Findi (ASX:FND) | 35.8% | 64.8% |

| HANA Micron (KOSDAQ:A067310) | 18.3% | 105.8% |

| Adveritas (ASX:AV1) | 21.2% | 144.2% |

| Plenti Group (ASX:PLT) | 12.8% | 107.6% |

| UTI (KOSDAQ:A179900) | 33.1% | 134.6% |

Underneath we present a selection of stocks filtered out by our screen.

Beijing Konruns PharmaceuticalLtd (SHSE:603590)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Beijing Konruns Pharmaceutical Co., Ltd. is involved in the research, development, production, and sale of pharmaceuticals both in China and internationally, with a market cap of CN¥3.75 billion.

Operations: The company generates its revenue from the pharmaceutical manufacturing segment, amounting to CN¥874.20 million.

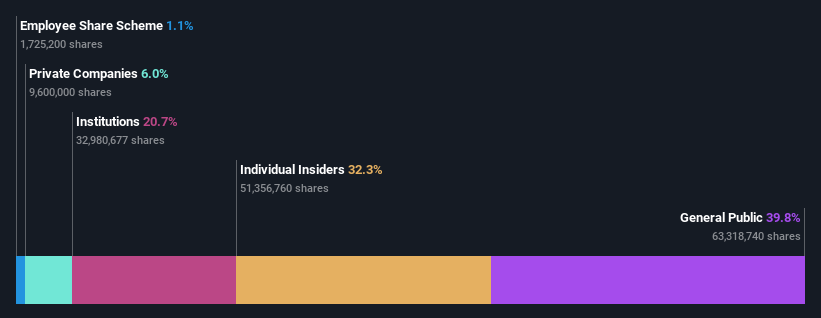

Insider Ownership: 32.3%

Beijing Konruns Pharmaceutical Ltd. is trading at a significant discount to its estimated fair value, suggesting potential upside. Despite recent declines in sales and revenue for H1 2024, the company is expected to achieve substantial earnings growth of 28.5% annually over the next three years, outpacing the Chinese market average. However, its return on equity remains low and it has an unstable dividend track record, indicating some caution for investors seeking sustainable returns.

- Get an in-depth perspective on Beijing Konruns PharmaceuticalLtd's performance by reading our analyst estimates report here.

- Our valuation report here indicates Beijing Konruns PharmaceuticalLtd may be undervalued.

Zhejiang Power New Energy (SHSE:688184)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Zhejiang Power New Energy Co., Ltd. focuses on the research, development, production, and sale of lithium-ion battery ternary cathode material precursors in China, with a market cap of CN¥2.19 billion.

Operations: The company's revenue is derived entirely from its Specialty Chemicals segment, amounting to CN¥1.42 billion.

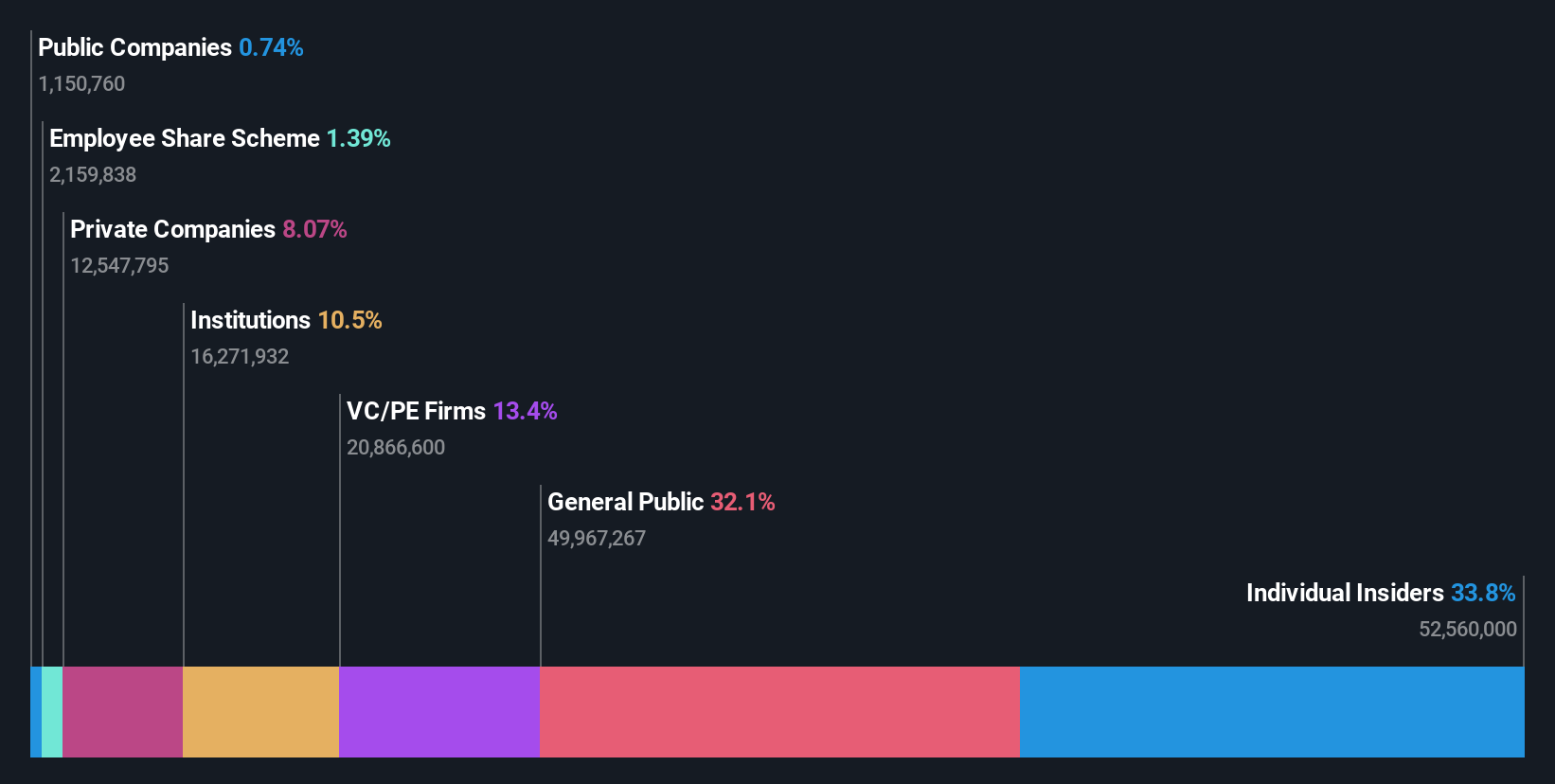

Insider Ownership: 32.6%

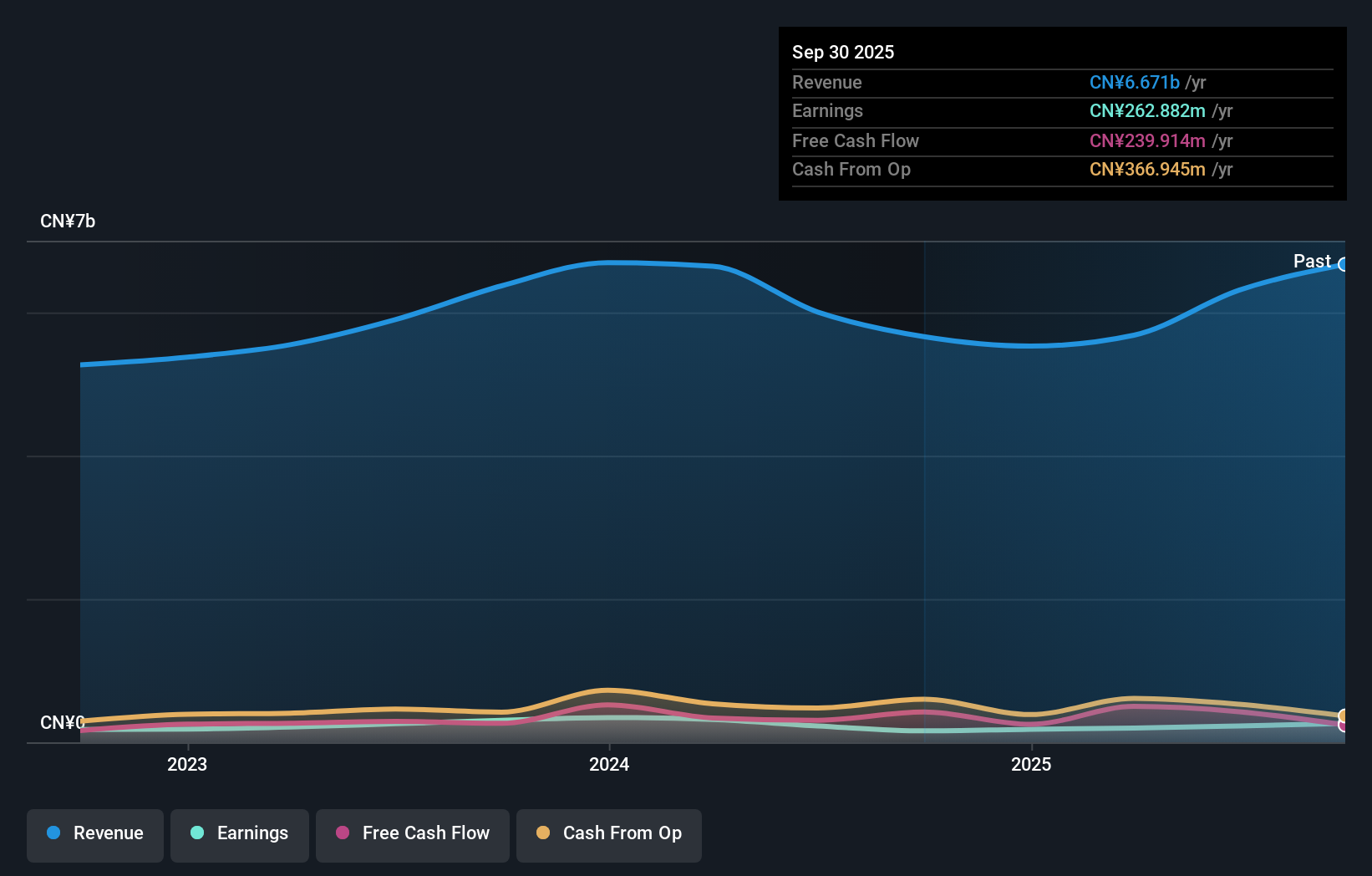

Zhejiang Power New Energy's insider ownership is complemented by strategic buybacks, with a recent repurchase of 1,043,804 shares worth CNY 12.89 million. Despite reporting a net loss of CNY 297.38 million for H1 2024, the company anticipates becoming profitable within three years, with earnings projected to grow significantly at over 100% annually. Revenue growth is expected to outpace the Chinese market average but remains below the high-growth threshold of 20%.

- Dive into the specifics of Zhejiang Power New Energy here with our thorough growth forecast report.

- Our valuation report here indicates Zhejiang Power New Energy may be overvalued.

Xiamen Jihong Technology (SZSE:002803)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Xiamen Jihong Technology Co., Ltd. operates in the cross-border social e-commerce sector in Southeast Asia with a market capitalization of CN¥4.66 billion.

Operations: The company generates revenue from its e-commerce business, amounting to CN¥3.62 billion, and its packaging business, contributing CN¥2.13 billion.

Insider Ownership: 35%

Xiamen Jihong Technology's insider ownership is highlighted by its completed buyback of 6.03 million shares for CNY 86.02 million. Despite a decline in H1 2024 earnings, with net income dropping to CNY 72.36 million from CNY 189.45 million a year ago, the company is forecasted to achieve significant earnings growth of over 30% annually, outpacing the Chinese market average and trading below estimated fair value, indicating potential for future appreciation.

- Navigate through the intricacies of Xiamen Jihong Technology with our comprehensive analyst estimates report here.

- Upon reviewing our latest valuation report, Xiamen Jihong Technology's share price might be too pessimistic.

Key Takeaways

- Unlock our comprehensive list of 1489 Fast Growing Companies With High Insider Ownership by clicking here.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Beijing Konruns PharmaceuticalLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SHSE:603590

Beijing Konruns PharmaceuticalLtd

Engages in the research and development, production, and sale of pharmaceuticals in China and internationally.

High growth potential with excellent balance sheet.