Advertisement

Returns Are Gaining Momentum At Tibet GaoZheng Explosive (SZSE:002827)

If we want to find a potential multi-bagger, often there are underlying trends that can provide clues. One common approach is to try and find a company with returns on capital employed (ROCE) that are increasing, in conjunction with a growing amount of capital employed. This shows us that it's a compounding machine, able to continually reinvest its earnings back into the business and generate higher returns. With that in mind, we've noticed some promising trends at Tibet GaoZheng Explosive (SZSE:002827) so let's look a bit deeper.

Understanding Return On Capital Employed (ROCE)

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. The formula for this calculation on Tibet GaoZheng Explosive is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.099 = CN¥172m ÷ (CN¥2.7b - CN¥928m) (Based on the trailing twelve months to June 2024).

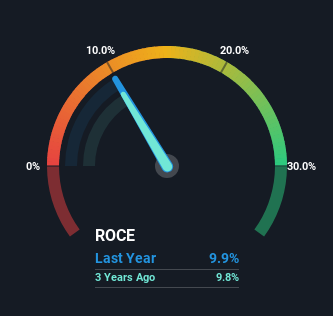

So, Tibet GaoZheng Explosive has an ROCE of 9.9%. On its own that's a low return, but compared to the average of 5.5% generated by the Chemicals industry, it's much better.

See our latest analysis for Tibet GaoZheng Explosive

Above you can see how the current ROCE for Tibet GaoZheng Explosive compares to its prior returns on capital, but there's only so much you can tell from the past. If you'd like, you can check out the forecasts from the analysts covering Tibet GaoZheng Explosive for free.

The Trend Of ROCE

While in absolute terms it isn't a high ROCE, it's promising to see that it has been moving in the right direction. Over the last five years, returns on capital employed have risen substantially to 9.9%. The company is effectively making more money per dollar of capital used, and it's worth noting that the amount of capital has increased too, by 128%. The increasing returns on a growing amount of capital is common amongst multi-baggers and that's why we're impressed.

For the record though, there was a noticeable increase in the company's current liabilities over the period, so we would attribute some of the ROCE growth to that. Essentially the business now has suppliers or short-term creditors funding about 35% of its operations, which isn't ideal. Keep an eye out for future increases because when the ratio of current liabilities to total assets gets particularly high, this can introduce some new risks for the business.

Our Take On Tibet GaoZheng Explosive's ROCE

In summary, it's great to see that Tibet GaoZheng Explosive can compound returns by consistently reinvesting capital at increasing rates of return, because these are some of the key ingredients of those highly sought after multi-baggers. And a remarkable 179% total return over the last five years tells us that investors are expecting more good things to come in the future. So given the stock has proven it has promising trends, it's worth researching the company further to see if these trends are likely to persist.

One more thing: We've identified 2 warning signs with Tibet GaoZheng Explosive (at least 1 which makes us a bit uncomfortable) , and understanding them would certainly be useful.

While Tibet GaoZheng Explosive may not currently earn the highest returns, we've compiled a list of companies that currently earn more than 25% return on equity. Check out this free list here.

Valuation is complex, but we're here to simplify it.

Discover if Tibet GaoZheng Explosive might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:002827

Tibet GaoZheng Explosive

Produces and sells civil explosives and blasting products in China.

Exceptional growth potential with proven track record.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|5.4% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.3% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|4.1% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|62.7% undervalued

DA

Community Contributor