Advertisement

3 Growth Companies Insiders Own With Earnings Rising Up To 66%

Simply Wall St

Reviewed by Simply Wall St

In recent weeks, global markets have faced volatility due to tariff uncertainties and mixed economic data, with U.S. job growth falling short of expectations and manufacturing activity showing signs of recovery. Despite these challenges, many companies have reported strong earnings performances, which has been a key driver of investor sentiment. In such an environment, stocks with high insider ownership can be appealing as they often indicate confidence from those closest to the company in its future prospects. Companies that combine this insider confidence with rising earnings may present compelling opportunities for growth-oriented investors seeking resilience amid market fluctuations.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| Lavvi Empreendimentos Imobiliários (BOVESPA:LAVV3) | 17.3% | 22.8% |

| SKS Technologies Group (ASX:SKS) | 29.7% | 24.8% |

| Propel Holdings (TSX:PRL) | 36.5% | 38.7% |

| CD Projekt (WSE:CDR) | 29.7% | 39.4% |

| Medley (TSE:4480) | 34.1% | 27.3% |

| Pharma Mar (BME:PHM) | 11.9% | 45.4% |

| Kingstone Companies (NasdaqCM:KINS) | 20.8% | 24.9% |

| Elliptic Laboratories (OB:ELABS) | 26.8% | 121.1% |

| Plenti Group (ASX:PLT) | 12.7% | 120.1% |

| Findi (ASX:FND) | 35.8% | 111.4% |

Let's uncover some gems from our specialized screener.

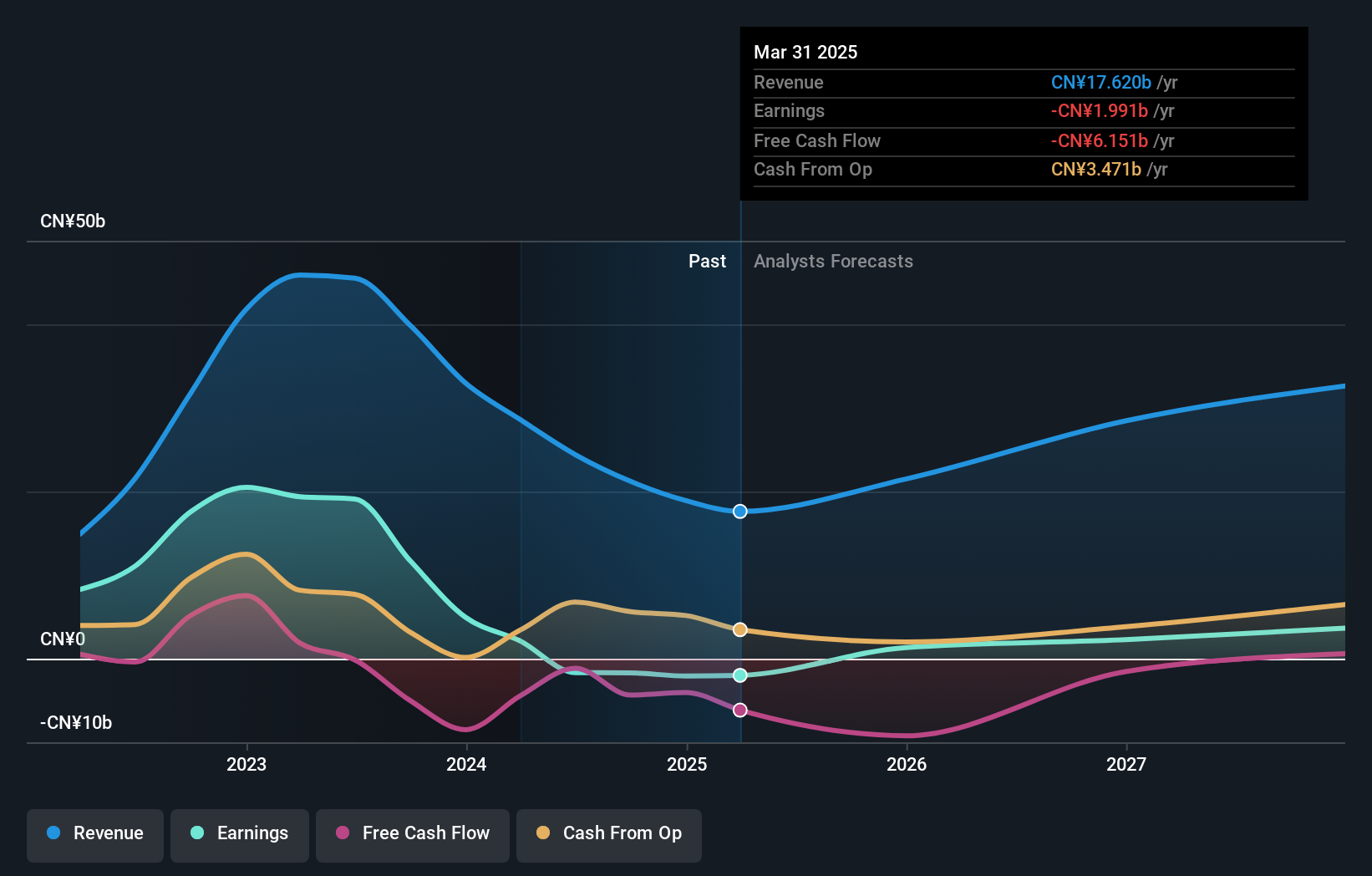

Ganfeng Lithium Group (SZSE:002460)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Ganfeng Lithium Group Co., Ltd. is a company that manufactures and sells lithium products across Mainland China, South Korea, Europe, the rest of Asia, North America, and internationally with a market cap of approximately CN¥65.11 billion.

Operations: Ganfeng Lithium Group Co., Ltd. generates revenue through the manufacture and sale of lithium products across various regions, including Mainland China, South Korea, Europe, the rest of Asia, North America, and other international markets.

Insider Ownership: 27.8%

Earnings Growth Forecast: 66.9% p.a.

Ganfeng Lithium Group faces challenges with a forecasted net loss between RMB 1.4 billion and RMB 2.1 billion for 2024, largely due to declining lithium product prices and significant fair value losses on financial assets like Pilbara Minerals Limited shares. Despite this, the company is expected to achieve above-average profit growth over the next three years as it becomes profitable, although its current debt coverage by operating cash flow remains weak.

- Unlock comprehensive insights into our analysis of Ganfeng Lithium Group stock in this growth report.

- Upon reviewing our latest valuation report, Ganfeng Lithium Group's share price might be too optimistic.

ASE Technology Holding (TWSE:3711)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: ASE Technology Holding Co., Ltd. offers semiconductor packaging and testing, as well as electronic manufacturing services globally, with a market cap of NT$740.31 billion.

Operations: Revenue Segments (in millions of NT$): Semiconductor packaging and testing contribute NT$357,000 million, while electronic manufacturing services account for NT$265,000 million.

Insider Ownership: 28.5%

Earnings Growth Forecast: 30.9% p.a.

ASE Technology Holding demonstrates potential for growth with earnings forecasted to rise significantly, outpacing the TW market. Despite a low Return on Equity projection and a dividend not well-covered by free cash flow, its Price-To-Earnings ratio remains attractive compared to industry peers. Recent revenue growth aligns with expectations, though insider ownership details are limited. The company continues securing substantial contracts through its subsidiary SPIL, potentially bolstering future performance.

- Take a closer look at ASE Technology Holding's potential here in our earnings growth report.

- Insights from our recent valuation report point to the potential overvaluation of ASE Technology Holding shares in the market.

Chenbro Micom (TWSE:8210)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Chenbro Micom Co., Ltd. is involved in the research, development, design, manufacture, processing, and trading of computer peripherals and systems globally, with a market cap of NT$34.84 billion.

Operations: The company's revenue is primarily derived from its computer peripherals segment, which generated NT$15.38 billion.

Insider Ownership: 25%

Earnings Growth Forecast: 15.7% p.a.

Chenbro Micom shows promise with its stock trading at 40.7% below estimated fair value, suggesting potential upside. Analysts agree on a price increase of 24.7%. Although earnings are forecast to grow slower than the TW market, they still show a healthy annual growth rate of 15.67%. Revenue is expected to grow faster than both the market and peers at 20.1% per year, despite recent volatility and an unstable dividend track record.

- Dive into the specifics of Chenbro Micom here with our thorough growth forecast report.

- Our comprehensive valuation report raises the possibility that Chenbro Micom is priced lower than what may be justified by its financials.

Key Takeaways

- Access the full spectrum of 1451 Fast Growing Companies With High Insider Ownership by clicking on this link.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SZSE:002460

Ganfeng Lithium Group

Manufactures and sells lithium products in Mainland China, South Korea, Europe, Rest of Asia, North America, and internationally.

Reasonable growth potential with worrying balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Vita Life Sciences Set for a 12.72% Revenue Growth While Tackling Operational Challenges

Fair Value AU$2.42|9.1% undervalued

RO

Community Contributor

Vossloh rides a €500 billion wave to boost growth and earnings in the next decade

Fair Value €78.41|6.1% undervalued

CH

Community Contributor

Intuitive Surgical Will Transform Healthcare with 12% Revenue Growth

Fair Value US$325.55|56.5% overvalued

UN

Community Contributor