Advertisement

Can Wuxi Double Elephant Micro Fibre Material Co.,Ltd's (SZSE:002395) Weak Financials Pull The Plug On The Stock's Current Momentum On Its Share Price?

Most readers would already be aware that Wuxi Double Elephant Micro Fibre MaterialLtd's (SZSE:002395) stock increased significantly by 18% over the past three months. However, we decided to pay close attention to its weak financials as we are doubtful that the current momentum will keep up, given the scenario. Particularly, we will be paying attention to Wuxi Double Elephant Micro Fibre MaterialLtd's ROE today.

Return on Equity or ROE is a test of how effectively a company is growing its value and managing investors’ money. In short, ROE shows the profit each dollar generates with respect to its shareholder investments.

See our latest analysis for Wuxi Double Elephant Micro Fibre MaterialLtd

How Is ROE Calculated?

Return on equity can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Wuxi Double Elephant Micro Fibre MaterialLtd is:

7.2% = CN¥67m ÷ CN¥934m (Based on the trailing twelve months to March 2024).

The 'return' is the amount earned after tax over the last twelve months. One way to conceptualize this is that for each CN¥1 of shareholders' capital it has, the company made CN¥0.07 in profit.

What Has ROE Got To Do With Earnings Growth?

So far, we've learned that ROE is a measure of a company's profitability. Based on how much of its profits the company chooses to reinvest or "retain", we are then able to evaluate a company's future ability to generate profits. Assuming all else is equal, companies that have both a higher return on equity and higher profit retention are usually the ones that have a higher growth rate when compared to companies that don't have the same features.

Wuxi Double Elephant Micro Fibre MaterialLtd's Earnings Growth And 7.2% ROE

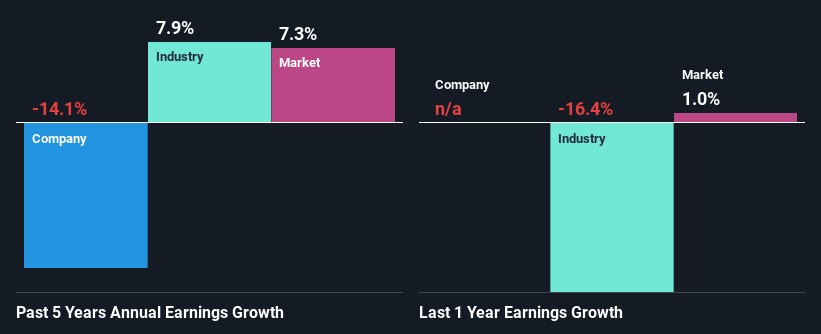

On the face of it, Wuxi Double Elephant Micro Fibre MaterialLtd's ROE is not much to talk about. However, its ROE is similar to the industry average of 6.3%, so we won't completely dismiss the company. But then again, Wuxi Double Elephant Micro Fibre MaterialLtd's five year net income shrunk at a rate of 14%. Remember, the company's ROE is a bit low to begin with. Therefore, the decline in earnings could also be the result of this.

So, as a next step, we compared Wuxi Double Elephant Micro Fibre MaterialLtd's performance against the industry and were disappointed to discover that while the company has been shrinking its earnings, the industry has been growing its earnings at a rate of 7.9% over the last few years.

Earnings growth is an important metric to consider when valuing a stock. What investors need to determine next is if the expected earnings growth, or the lack of it, is already built into the share price. By doing so, they will have an idea if the stock is headed into clear blue waters or if swampy waters await. One good indicator of expected earnings growth is the P/E ratio which determines the price the market is willing to pay for a stock based on its earnings prospects. So, you may want to check if Wuxi Double Elephant Micro Fibre MaterialLtd is trading on a high P/E or a low P/E, relative to its industry.

Is Wuxi Double Elephant Micro Fibre MaterialLtd Efficiently Re-investing Its Profits?

Wuxi Double Elephant Micro Fibre MaterialLtd has a high three-year median payout ratio of 58% (that is, it is retaining 42% of its profits). This suggests that the company is paying most of its profits as dividends to its shareholders. This goes some way in explaining why its earnings have been shrinking. With only a little being reinvested into the business, earnings growth would obviously be low or non-existent. You can see the 3 risks we have identified for Wuxi Double Elephant Micro Fibre MaterialLtd by visiting our risks dashboard for free on our platform here.

In addition, Wuxi Double Elephant Micro Fibre MaterialLtd has been paying dividends over a period of at least ten years suggesting that keeping up dividend payments is way more important to the management even if it comes at the cost of business growth.

Conclusion

On the whole, Wuxi Double Elephant Micro Fibre MaterialLtd's performance is quite a big let-down. Because the company is not reinvesting much into the business, and given the low ROE, it's not surprising to see the lack or absence of growth in its earnings. Until now, we have only just grazed the surface of the company's past performance by looking at the company's fundamentals. To gain further insights into Wuxi Double Elephant Micro Fibre MaterialLtd's past profit growth, check out this visualization of past earnings, revenue and cash flows.

Valuation is complex, but we're here to simplify it.

Discover if Wuxi Double Elephant Micro Fibre MaterialLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SZSE:002395

Wuxi Double Elephant Micro Fibre MaterialLtd

Manufactures and sells artificial and synthetic leather products in the People’s Republic of China and internationally.

Flawless balance sheet with solid track record and pays a dividend.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.2% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.7% overvalued

LI

Community Contributor