Advertisement

- China

- /

- Energy Services

- /

- SZSE:300084

Haimo Technologies Group Corp.'s (SZSE:300084) 33% Jump Shows Its Popularity With Investors

Those holding Haimo Technologies Group Corp. (SZSE:300084) shares would be relieved that the share price has rebounded 33% in the last thirty days, but it needs to keep going to repair the recent damage it has caused to investor portfolios. But the gains over the last month weren't enough to make shareholders whole, as the share price is still down 6.7% in the last twelve months.

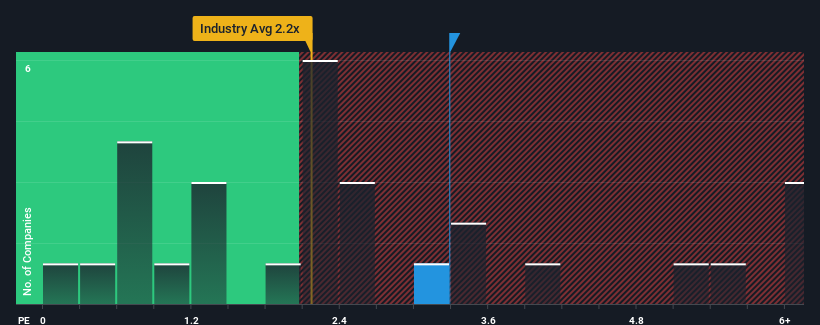

Since its price has surged higher, when almost half of the companies in China's Energy Services industry have price-to-sales ratios (or "P/S") below 2.2x, you may consider Haimo Technologies Group as a stock probably not worth researching with its 3.3x P/S ratio. However, the P/S might be high for a reason and it requires further investigation to determine if it's justified.

Check out our latest analysis for Haimo Technologies Group

How Haimo Technologies Group Has Been Performing

With revenue growth that's superior to most other companies of late, Haimo Technologies Group has been doing relatively well. It seems the market expects this form will continue into the future, hence the elevated P/S ratio. However, if this isn't the case, investors might get caught out paying too much for the stock.

Want the full picture on analyst estimates for the company? Then our free report on Haimo Technologies Group will help you uncover what's on the horizon.Do Revenue Forecasts Match The High P/S Ratio?

Haimo Technologies Group's P/S ratio would be typical for a company that's expected to deliver solid growth, and importantly, perform better than the industry.

If we review the last year of revenue growth, the company posted a terrific increase of 25%. Revenue has also lifted 23% in aggregate from three years ago, mostly thanks to the last 12 months of growth. Therefore, it's fair to say the revenue growth recently has been respectable for the company.

Looking ahead now, revenue is anticipated to climb by 26% during the coming year according to the lone analyst following the company. With the industry only predicted to deliver 18%, the company is positioned for a stronger revenue result.

With this information, we can see why Haimo Technologies Group is trading at such a high P/S compared to the industry. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

The Final Word

Haimo Technologies Group shares have taken a big step in a northerly direction, but its P/S is elevated as a result. It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

As we suspected, our examination of Haimo Technologies Group's analyst forecasts revealed that its superior revenue outlook is contributing to its high P/S. At this stage investors feel the potential for a deterioration in revenues is quite remote, justifying the elevated P/S ratio. Unless the analysts have really missed the mark, these strong revenue forecasts should keep the share price buoyant.

It is also worth noting that we have found 1 warning sign for Haimo Technologies Group that you need to take into consideration.

If these risks are making you reconsider your opinion on Haimo Technologies Group, explore our interactive list of high quality stocks to get an idea of what else is out there.

Valuation is complex, but we're here to simplify it.

Discover if Haimo Technologies Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:300084

Haimo Technologies Group

Manufactures and sells oilfield equipment and instruments for oilfield service companies in China, the Middle East, North Africa, Central, South and Southeast Asia, and North and South America.

Flawless balance sheet with weak fundamentals.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.3% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.0% undervalued

TI

Community Contributor