Advertisement

After Leaping 41% Guangdong Wanlima Industry Co. ,Ltd (SZSE:300591) Shares Are Not Flying Under The Radar

Guangdong Wanlima Industry Co. ,Ltd (SZSE:300591) shareholders have had their patience rewarded with a 41% share price jump in the last month. Not all shareholders will be feeling jubilant, since the share price is still down a very disappointing 33% in the last twelve months.

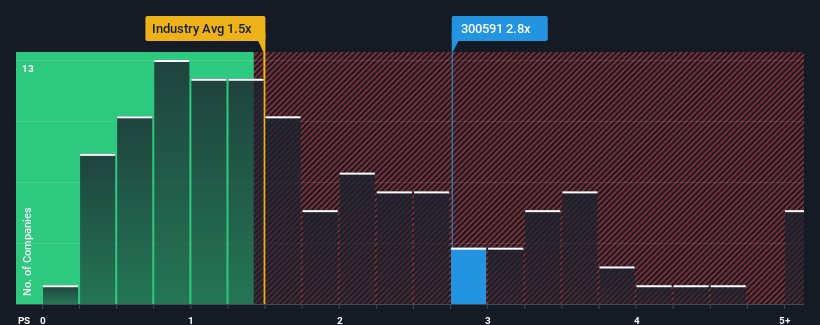

Following the firm bounce in price, when almost half of the companies in China's Luxury industry have price-to-sales ratios (or "P/S") below 1.5x, you may consider Guangdong Wanlima Industry Ltd as a stock probably not worth researching with its 2.8x P/S ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the elevated P/S.

Check out our latest analysis for Guangdong Wanlima Industry Ltd

What Does Guangdong Wanlima Industry Ltd's Recent Performance Look Like?

Guangdong Wanlima Industry Ltd has been doing a good job lately as it's been growing revenue at a solid pace. Perhaps the market is expecting this decent revenue performance to beat out the industry over the near term, which has kept the P/S propped up. If not, then existing shareholders may be a little nervous about the viability of the share price.

Want the full picture on earnings, revenue and cash flow for the company? Then our free report on Guangdong Wanlima Industry Ltd will help you shine a light on its historical performance.Is There Enough Revenue Growth Forecasted For Guangdong Wanlima Industry Ltd?

There's an inherent assumption that a company should outperform the industry for P/S ratios like Guangdong Wanlima Industry Ltd's to be considered reasonable.

Retrospectively, the last year delivered an exceptional 24% gain to the company's top line. The latest three year period has also seen an excellent 79% overall rise in revenue, aided by its short-term performance. Therefore, it's fair to say the revenue growth recently has been superb for the company.

Comparing that recent medium-term revenue trajectory with the industry's one-year growth forecast of 14% shows it's noticeably more attractive.

With this in consideration, it's not hard to understand why Guangdong Wanlima Industry Ltd's P/S is high relative to its industry peers. It seems most investors are expecting this strong growth to continue and are willing to pay more for the stock.

The Bottom Line On Guangdong Wanlima Industry Ltd's P/S

The large bounce in Guangdong Wanlima Industry Ltd's shares has lifted the company's P/S handsomely. While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

As we suspected, our examination of Guangdong Wanlima Industry Ltd revealed its three-year revenue trends are contributing to its high P/S, given they look better than current industry expectations. Right now shareholders are comfortable with the P/S as they are quite confident revenue aren't under threat. If recent medium-term revenue trends continue, it's hard to see the share price falling strongly in the near future under these circumstances.

Before you settle on your opinion, we've discovered 3 warning signs for Guangdong Wanlima Industry Ltd (2 don't sit too well with us!) that you should be aware of.

If these risks are making you reconsider your opinion on Guangdong Wanlima Industry Ltd, explore our interactive list of high quality stocks to get an idea of what else is out there.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:300591

Guangdong Wanlima Industry Ltd

Engages in the designing, researching, production, manufacturing, and marketing of leather products in China.

Flawless balance sheet with very low risk.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor