Advertisement

- China

- /

- Consumer Durables

- /

- SZSE:002351

Why Investors Shouldn't Be Surprised By Edifier Technology Co., Ltd.'s (SZSE:002351) 26% Share Price Plunge

Edifier Technology Co., Ltd. (SZSE:002351) shares have retraced a considerable 26% in the last month, reversing a fair amount of their solid recent performance. The recent drop has obliterated the annual return, with the share price now down 5.9% over that longer period.

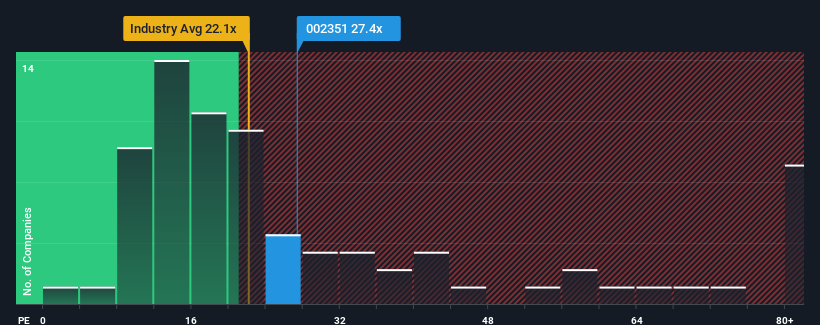

In spite of the heavy fall in price, Edifier Technology's price-to-earnings (or "P/E") ratio of 27.4x might still make it look like a buy right now compared to the market in China, where around half of the companies have P/E ratios above 33x and even P/E's above 63x are quite common. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's limited.

Edifier Technology certainly has been doing a good job lately as its earnings growth has been positive while most other companies have been seeing their earnings go backwards. One possibility is that the P/E is low because investors think the company's earnings are going to fall away like everyone else's soon. If not, then existing shareholders have reason to be quite optimistic about the future direction of the share price.

See our latest analysis for Edifier Technology

Is There Any Growth For Edifier Technology?

The only time you'd be truly comfortable seeing a P/E as low as Edifier Technology's is when the company's growth is on track to lag the market.

Taking a look back first, we see that the company grew earnings per share by an impressive 35% last year. The latest three year period has also seen an excellent 40% overall rise in EPS, aided by its short-term performance. Therefore, it's fair to say the earnings growth recently has been superb for the company.

Shifting to the future, estimates from the three analysts covering the company suggest earnings should grow by 25% over the next year. That's shaping up to be materially lower than the 38% growth forecast for the broader market.

In light of this, it's understandable that Edifier Technology's P/E sits below the majority of other companies. Apparently many shareholders weren't comfortable holding on while the company is potentially eyeing a less prosperous future.

The Bottom Line On Edifier Technology's P/E

Edifier Technology's P/E has taken a tumble along with its share price. We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

As we suspected, our examination of Edifier Technology's analyst forecasts revealed that its inferior earnings outlook is contributing to its low P/E. At this stage investors feel the potential for an improvement in earnings isn't great enough to justify a higher P/E ratio. Unless these conditions improve, they will continue to form a barrier for the share price around these levels.

Plus, you should also learn about these 2 warning signs we've spotted with Edifier Technology.

Of course, you might find a fantastic investment by looking at a few good candidates. So take a peek at this free list of companies with a strong growth track record, trading on a low P/E.

Valuation is complex, but we're here to simplify it.

Discover if Edifier Technology might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:002351

Edifier Technology

Designs, produces, and sells audio equipment in China.

Flawless balance sheet established dividend payer.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor