- China

- /

- Consumer Durables

- /

- SHSE:603610

Don't Buy Keeson Technology Corporation Limited (SHSE:603610) For Its Next Dividend Without Doing These Checks

Some investors rely on dividends for growing their wealth, and if you're one of those dividend sleuths, you might be intrigued to know that Keeson Technology Corporation Limited (SHSE:603610) is about to go ex-dividend in just 3 days. The ex-dividend date occurs one day before the record date which is the day on which shareholders need to be on the company's books in order to receive a dividend. The ex-dividend date is an important date to be aware of as any purchase of the stock made on or after this date might mean a late settlement that doesn't show on the record date. Meaning, you will need to purchase Keeson Technology's shares before the 13th of June to receive the dividend, which will be paid on the 13th of June.

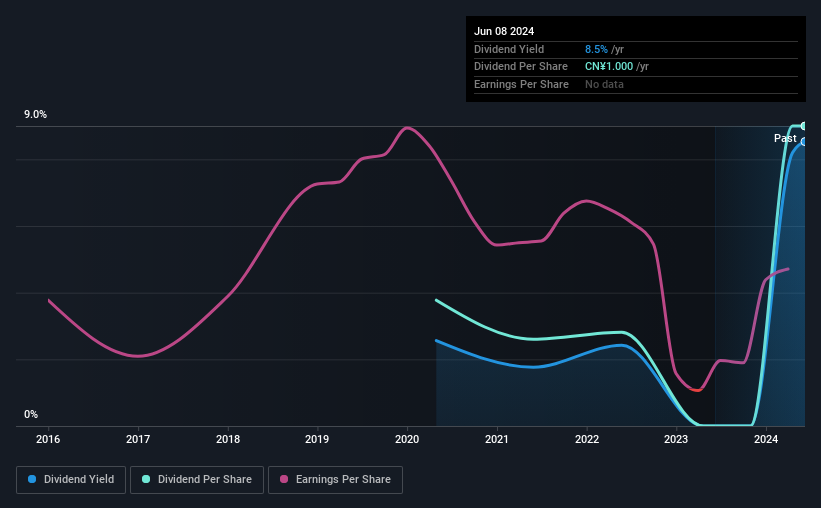

The company's next dividend payment will be CN¥1.00 per share, on the back of last year when the company paid a total of CN¥1.00 to shareholders. Looking at the last 12 months of distributions, Keeson Technology has a trailing yield of approximately 8.5% on its current stock price of CN¥11.72. Dividends are a major contributor to investment returns for long term holders, but only if the dividend continues to be paid. As a result, readers should always check whether Keeson Technology has been able to grow its dividends, or if the dividend might be cut.

See our latest analysis for Keeson Technology

Dividends are typically paid out of company income, so if a company pays out more than it earned, its dividend is usually at a higher risk of being cut. Keeson Technology distributed an unsustainably high 157% of its profit as dividends to shareholders last year. Without more sustainable payment behaviour, the dividend looks precarious. Yet cash flows are even more important than profits for assessing a dividend, so we need to see if the company generated enough cash to pay its distribution. Thankfully its dividend payments took up just 43% of the free cash flow it generated, which is a comfortable payout ratio.

It's disappointing to see that the dividend was not covered by profits, but cash is more important from a dividend sustainability perspective, and Keeson Technology fortunately did generate enough cash to fund its dividend. Still, if the company repeatedly paid a dividend greater than its profits, we'd be concerned. Extraordinarily few companies are capable of persistently paying a dividend that is greater than their profits.

Click here to see how much of its profit Keeson Technology paid out over the last 12 months.

Have Earnings And Dividends Been Growing?

Businesses with shrinking earnings are tricky from a dividend perspective. Investors love dividends, so if earnings fall and the dividend is reduced, expect a stock to be sold off heavily at the same time. Readers will understand then, why we're concerned to see Keeson Technology's earnings per share have dropped 10% a year over the past five years. Ultimately, when earnings per share decline, the size of the pie from which dividends can be paid, shrinks.

Another key way to measure a company's dividend prospects is by measuring its historical rate of dividend growth. Keeson Technology has delivered an average of 24% per year annual increase in its dividend, based on the past four years of dividend payments. The only way to pay higher dividends when earnings are shrinking is either to pay out a larger percentage of profits, spend cash from the balance sheet, or borrow the money. Keeson Technology is already paying out a high percentage of its income, so without earnings growth, we're doubtful of whether this dividend will grow much in the future.

Final Takeaway

From a dividend perspective, should investors buy or avoid Keeson Technology? It's never great to see earnings per share declining, especially when a company is paying out 157% of its profit as dividends, which we feel is uncomfortably high. Yet cashflow was much stronger, which makes us wonder if there are some large timing issues in Keeson Technology's cash flows, or perhaps the company has written down some assets aggressively, reducing its income. It's not that we think Keeson Technology is a bad company, but these characteristics don't generally lead to outstanding dividend performance.

So if you're still interested in Keeson Technology despite it's poor dividend qualities, you should be well informed on some of the risks facing this stock. For instance, we've identified 2 warning signs for Keeson Technology (1 is a bit concerning) you should be aware of.

If you're in the market for strong dividend payers, we recommend checking our selection of top dividend stocks.

Valuation is complex, but we're here to simplify it.

Discover if Keeson Technology might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:603610

Keeson Technology

Research and develops, produces, and sells smart beds, mattresses, and pillows worldwide.

Undervalued with excellent balance sheet.