Advertisement

- China

- /

- Commercial Services

- /

- SZSE:300779

Qingdao Huicheng Environmental Technology Group Co., Ltd.'s (SZSE:300779) P/S Is Still On The Mark Following 33% Share Price Bounce

Qingdao Huicheng Environmental Technology Group Co., Ltd. (SZSE:300779) shares have had a really impressive month, gaining 33% after a shaky period beforehand. The last 30 days bring the annual gain to a very sharp 51%.

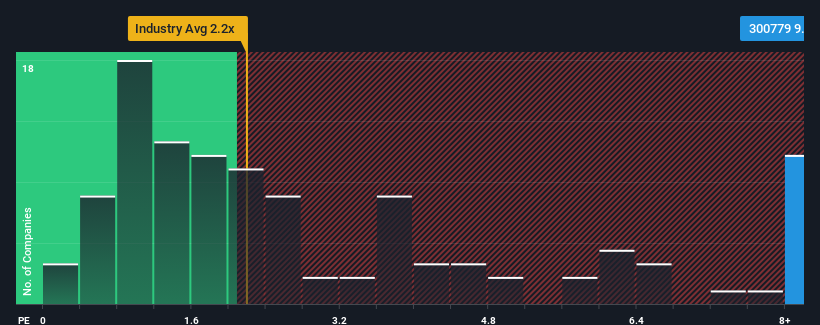

Following the firm bounce in price, given around half the companies in China's Commercial Services industry have price-to-sales ratios (or "P/S") below 2.2x, you may consider Qingdao Huicheng Environmental Technology Group as a stock to avoid entirely with its 9.4x P/S ratio. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's so lofty.

View our latest analysis for Qingdao Huicheng Environmental Technology Group

How Has Qingdao Huicheng Environmental Technology Group Performed Recently?

With revenue growth that's superior to most other companies of late, Qingdao Huicheng Environmental Technology Group has been doing relatively well. It seems the market expects this form will continue into the future, hence the elevated P/S ratio. However, if this isn't the case, investors might get caught out paying too much for the stock.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Qingdao Huicheng Environmental Technology Group.Do Revenue Forecasts Match The High P/S Ratio?

The only time you'd be truly comfortable seeing a P/S as steep as Qingdao Huicheng Environmental Technology Group's is when the company's growth is on track to outshine the industry decidedly.

If we review the last year of revenue growth, the company posted a terrific increase of 60%. Pleasingly, revenue has also lifted 295% in aggregate from three years ago, thanks to the last 12 months of growth. Therefore, it's fair to say the revenue growth recently has been superb for the company.

Looking ahead now, revenue is anticipated to climb by 59% during the coming year according to the two analysts following the company. Meanwhile, the rest of the industry is forecast to only expand by 29%, which is noticeably less attractive.

In light of this, it's understandable that Qingdao Huicheng Environmental Technology Group's P/S sits above the majority of other companies. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

The Key Takeaway

Shares in Qingdao Huicheng Environmental Technology Group have seen a strong upwards swing lately, which has really helped boost its P/S figure. Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

Our look into Qingdao Huicheng Environmental Technology Group shows that its P/S ratio remains high on the merit of its strong future revenues. It appears that shareholders are confident in the company's future revenues, which is propping up the P/S. It's hard to see the share price falling strongly in the near future under these circumstances.

There are also other vital risk factors to consider and we've discovered 3 warning signs for Qingdao Huicheng Environmental Technology Group (1 shouldn't be ignored!) that you should be aware of before investing here.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Valuation is complex, but we're here to simplify it.

Discover if Qingdao Huicheng Environmental Technology Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:300779

Qingdao Huicheng Environmental Technology Group

Qingdao Huicheng Environmental Technology Group Co., Ltd.

High growth potential with slight risk.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor