Advertisement

Tongyu Heavy Industry Co., Ltd. (SZSE:300185) Could Be Riskier Than It Looks

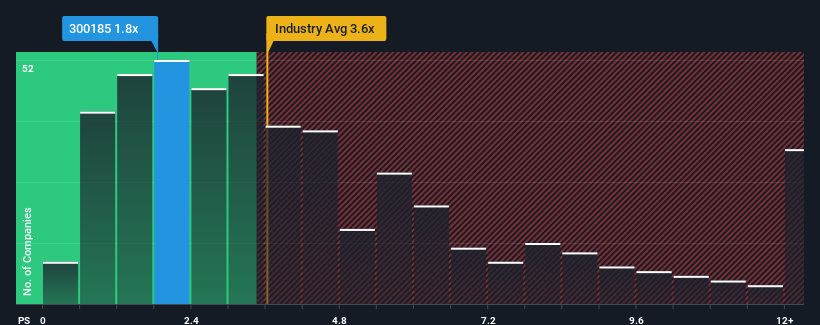

Tongyu Heavy Industry Co., Ltd.'s (SZSE:300185) price-to-sales (or "P/S") ratio of 1.8x might make it look like a buy right now compared to the Machinery industry in China, where around half of the companies have P/S ratios above 3.6x and even P/S above 7x are quite common. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's limited.

View our latest analysis for Tongyu Heavy Industry

What Does Tongyu Heavy Industry's Recent Performance Look Like?

Tongyu Heavy Industry could be doing better as its revenue has been going backwards lately while most other companies have been seeing positive revenue growth. Perhaps the P/S remains low as investors think the prospects of strong revenue growth aren't on the horizon. So while you could say the stock is cheap, investors will be looking for improvement before they see it as good value.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Tongyu Heavy Industry.How Is Tongyu Heavy Industry's Revenue Growth Trending?

The only time you'd be truly comfortable seeing a P/S as low as Tongyu Heavy Industry's is when the company's growth is on track to lag the industry.

Retrospectively, the last year delivered a frustrating 4.0% decrease to the company's top line. As a result, revenue from three years ago have also fallen 4.4% overall. So unfortunately, we have to acknowledge that the company has not done a great job of growing revenue over that time.

Shifting to the future, estimates from the one analyst covering the company suggest revenue should grow by 35% over the next year. That's shaping up to be materially higher than the 23% growth forecast for the broader industry.

With this in consideration, we find it intriguing that Tongyu Heavy Industry's P/S sits behind most of its industry peers. Apparently some shareholders are doubtful of the forecasts and have been accepting significantly lower selling prices.

The Bottom Line On Tongyu Heavy Industry's P/S

Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

To us, it seems Tongyu Heavy Industry currently trades on a significantly depressed P/S given its forecasted revenue growth is higher than the rest of its industry. There could be some major risk factors that are placing downward pressure on the P/S ratio. It appears the market could be anticipating revenue instability, because these conditions should normally provide a boost to the share price.

Having said that, be aware Tongyu Heavy Industry is showing 3 warning signs in our investment analysis, and 2 of those make us uncomfortable.

If you're unsure about the strength of Tongyu Heavy Industry's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Valuation is complex, but we're here to simplify it.

Discover if Tongyu Heavy Industry might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:300185

Tongyu Heavy Industry

Engages in the research and development, manufacture, and sale of forgings and castings.

Proven track record with mediocre balance sheet.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor