- China

- /

- Electrical

- /

- SZSE:300014

August 2024's Chinese Exchange Picks For Estimated Undervalued Stocks

Reviewed by Simply Wall St

Chinese stocks have recently faced downward pressure, with the Shanghai Composite Index falling 1.48% and the blue-chip CSI 300 down 1.56%, amid concerns about deflationary pressures despite a stronger-than-expected increase in consumer prices. However, these market conditions can present potential opportunities for discerning investors to identify undervalued stocks. In this article, we will explore three Chinese stocks that appear to be undervalued based on current market metrics and economic indicators.

Top 10 Undervalued Stocks Based On Cash Flows In China

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Imeik Technology DevelopmentLtd (SZSE:300896) | CN¥169.70 | CN¥326.54 | 48% |

| Anhui Huaheng Biotechnology (SHSE:688639) | CN¥39.21 | CN¥76.16 | 48.5% |

| Shenzhen Hopewind Electric (SHSE:603063) | CN¥13.55 | CN¥26.87 | 49.6% |

| Proya CosmeticsLtd (SHSE:603605) | CN¥86.45 | CN¥165.54 | 47.8% |

| Jiangsu Hualan New Pharmaceutical MaterialLtd (SZSE:301093) | CN¥18.99 | CN¥37.43 | 49.3% |

| Guangzhou Tinci Materials Technology (SZSE:002709) | CN¥14.77 | CN¥28.97 | 49% |

| Qingdao NovelBeam TechnologyLtd (SHSE:688677) | CN¥31.47 | CN¥62.60 | 49.7% |

| Songcheng Performance DevelopmentLtd (SZSE:300144) | CN¥8.10 | CN¥15.65 | 48.2% |

| NBTM New Materials Group (SHSE:600114) | CN¥14.41 | CN¥27.67 | 47.9% |

| Beijing Aosaikang Pharmaceutical (SZSE:002755) | CN¥11.08 | CN¥21.79 | 49.1% |

Underneath we present a selection of stocks filtered out by our screen.

Beijing Aosaikang Pharmaceutical (SZSE:002755)

Overview: Beijing Aosaikang Pharmaceutical Co., Ltd. is a pharmaceutical company engaged in the research, development, and production of various pharmaceutical products with a market cap of approximately CN¥10.28 billion.

Operations: Beijing Aosaikang Pharmaceutical Co., Ltd. generates revenue through the research, development, and production of various pharmaceutical products.

Estimated Discount To Fair Value: 49.1%

Beijing Aosaikang Pharmaceutical is trading at CN¥11.08, significantly below its estimated fair value of CN¥21.79, indicating it may be undervalued based on cash flows. The company’s revenue is forecast to grow 18.3% per year, outpacing the Chinese market's average growth rate of 13.5%. Earnings are expected to grow 90.67% annually and become profitable within three years, although Return on Equity is projected to remain low at 4.3%.

- In light of our recent growth report, it seems possible that Beijing Aosaikang Pharmaceutical's financial performance will exceed current levels.

- Click to explore a detailed breakdown of our findings in Beijing Aosaikang Pharmaceutical's balance sheet health report.

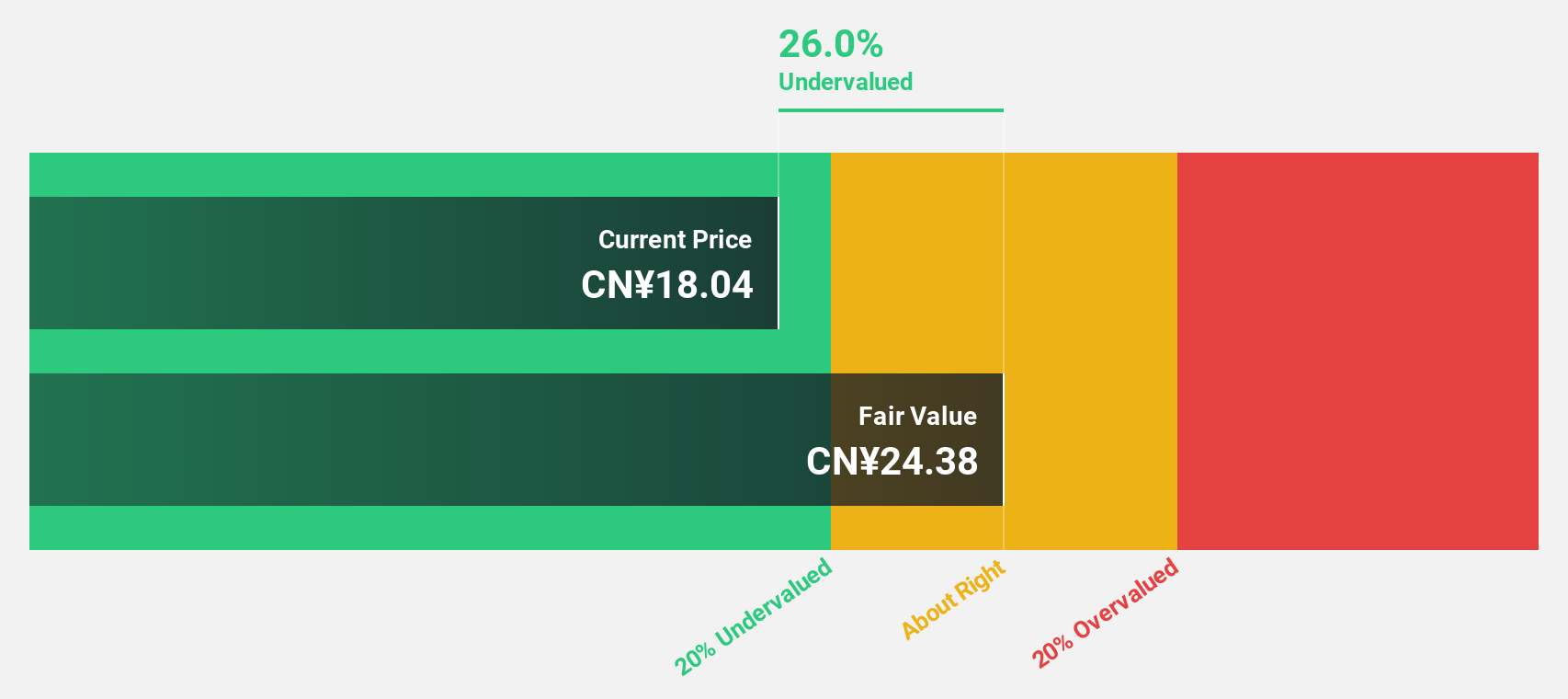

EVE Energy (SZSE:300014)

Overview: EVE Energy Co., Ltd. is a company that supplies lithium batteries both in China and globally, with a market cap of CN¥77.41 billion.

Operations: EVE Energy's revenue from electronic component manufacturing is CN¥46.92 billion.

Estimated Discount To Fair Value: 31.4%

EVE Energy is currently trading at CN¥37.93, significantly below its estimated fair value of CN¥55.26, suggesting it is undervalued based on cash flows. Despite a history of unstable dividends and large one-off items affecting financial results, the company’s revenue and earnings are forecast to grow at 21.6% and 23.11% per year respectively, outpacing the Chinese market averages. However, Return on Equity is expected to remain low at 14.8%.

- Our earnings growth report unveils the potential for significant increases in EVE Energy's future results.

- Click here to discover the nuances of EVE Energy with our detailed financial health report.

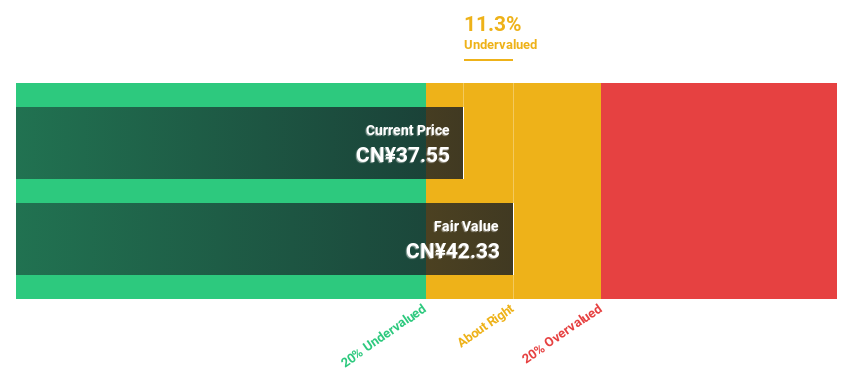

POCO Holding (SZSE:300811)

Overview: POCO Holding Co., Ltd. develops, produces, and sells alloy soft magnetic powder, alloy soft magnetic cores, and related inductance components for electronic equipment users, with a market cap of CN¥10.75 billion.

Operations: POCO Holding's revenue primarily comes from electronic components, amounting to CN¥1.20 billion.

Estimated Discount To Fair Value: 22.5%

POCO Holding is trading at CN¥38.3, well below its estimated fair value of CN¥49.39, indicating it is undervalued based on cash flows. The company’s revenue and earnings are forecast to grow at 26.6% and 28% per year respectively, significantly surpassing market averages. Recent dividend affirmations reflect financial stability despite a highly volatile share price over the past three months and a forecasted low Return on Equity of 18%.

- The analysis detailed in our POCO Holding growth report hints at robust future financial performance.

- Delve into the full analysis health report here for a deeper understanding of POCO Holding.

Next Steps

- Click this link to deep-dive into the 102 companies within our Undervalued Chinese Stocks Based On Cash Flows screener.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if EVE Energy might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SZSE:300014

Undervalued with high growth potential.