Advertisement

Little Excitement Around Zhejiang Dun'an Artificial Environment Co., Ltd's (SZSE:002011) Earnings

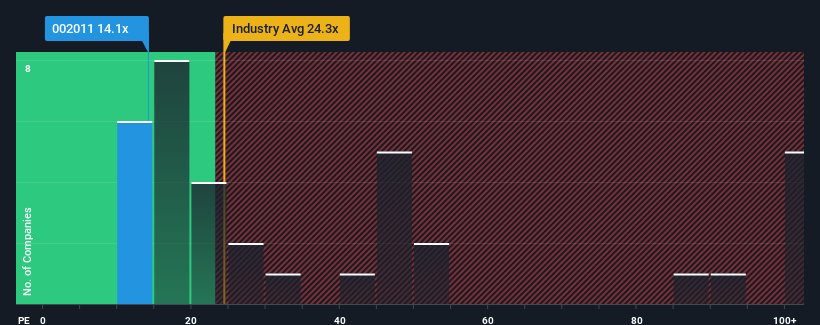

Zhejiang Dun'an Artificial Environment Co., Ltd's (SZSE:002011) price-to-earnings (or "P/E") ratio of 14.1x might make it look like a strong buy right now compared to the market in China, where around half of the companies have P/E ratios above 38x and even P/E's above 74x are quite common. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's so limited.

With its earnings growth in positive territory compared to the declining earnings of most other companies, Zhejiang Dun'an Artificial Environment has been doing quite well of late. It might be that many expect the strong earnings performance to degrade substantially, possibly more than the market, which has repressed the P/E. If not, then existing shareholders have reason to be quite optimistic about the future direction of the share price.

Check out our latest analysis for Zhejiang Dun'an Artificial Environment

How Is Zhejiang Dun'an Artificial Environment's Growth Trending?

There's an inherent assumption that a company should far underperform the market for P/E ratios like Zhejiang Dun'an Artificial Environment's to be considered reasonable.

Retrospectively, the last year delivered an exceptional 21% gain to the company's bottom line. Although, its longer-term performance hasn't been as strong with three-year EPS growth being relatively non-existent overall. Accordingly, shareholders probably wouldn't have been overly satisfied with the unstable medium-term growth rates.

Shifting to the future, estimates from the six analysts covering the company suggest earnings should grow by 30% over the next year. Meanwhile, the rest of the market is forecast to expand by 38%, which is noticeably more attractive.

With this information, we can see why Zhejiang Dun'an Artificial Environment is trading at a P/E lower than the market. It seems most investors are expecting to see limited future growth and are only willing to pay a reduced amount for the stock.

What We Can Learn From Zhejiang Dun'an Artificial Environment's P/E?

Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

As we suspected, our examination of Zhejiang Dun'an Artificial Environment's analyst forecasts revealed that its inferior earnings outlook is contributing to its low P/E. At this stage investors feel the potential for an improvement in earnings isn't great enough to justify a higher P/E ratio. Unless these conditions improve, they will continue to form a barrier for the share price around these levels.

A lot of potential risks can sit within a company's balance sheet. Our free balance sheet analysis for Zhejiang Dun'an Artificial Environment with six simple checks will allow you to discover any risks that could be an issue.

You might be able to find a better investment than Zhejiang Dun'an Artificial Environment. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Valuation is complex, but we're here to simplify it.

Discover if Zhejiang Dun'an Artificial Environment might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:002011

Zhejiang Dun'an Artificial Environment

Engages in the research and development, production, and sale of refrigeration accessories, refrigeration and air-conditioning equipment, and core components for thermal management of new energy vehicles in China and internationally.

Flawless balance sheet and good value.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor