As global markets navigate a mix of economic signals, with the S&P 500 and Nasdaq Composite seeing gains fueled by tech sector optimism, investors are increasingly focused on companies demonstrating robust growth potential and strong insider ownership. In this environment, high-growth companies with significant insider commitment can offer a compelling proposition, as they often signal confidence in the company's future prospects and alignment with shareholder interests.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| Lavvi Empreendimentos Imobiliários (BOVESPA:LAVV3) | 11.9% | 21.1% |

| Atlas Energy Solutions (NYSE:AESI) | 29.1% | 41.9% |

| Kirloskar Pneumatic (BSE:505283) | 30.3% | 30.1% |

| Arctech Solar Holding (SHSE:688408) | 37.8% | 29.8% |

| Laopu Gold (SEHK:6181) | 36.4% | 33.2% |

| HANA Micron (KOSDAQ:A067310) | 18.3% | 105.8% |

| Credo Technology Group Holding (NasdaqGS:CRDO) | 13.9% | 95% |

| Adveritas (ASX:AV1) | 21.2% | 144.2% |

| Plenti Group (ASX:PLT) | 12.8% | 106.4% |

| EHang Holdings (NasdaqGM:EH) | 32.8% | 81.4% |

Let's take a closer look at a couple of our picks from the screened companies.

Hangzhou Jingye Intelligent Technology (SHSE:688290)

Simply Wall St Growth Rating: ★★★★★☆

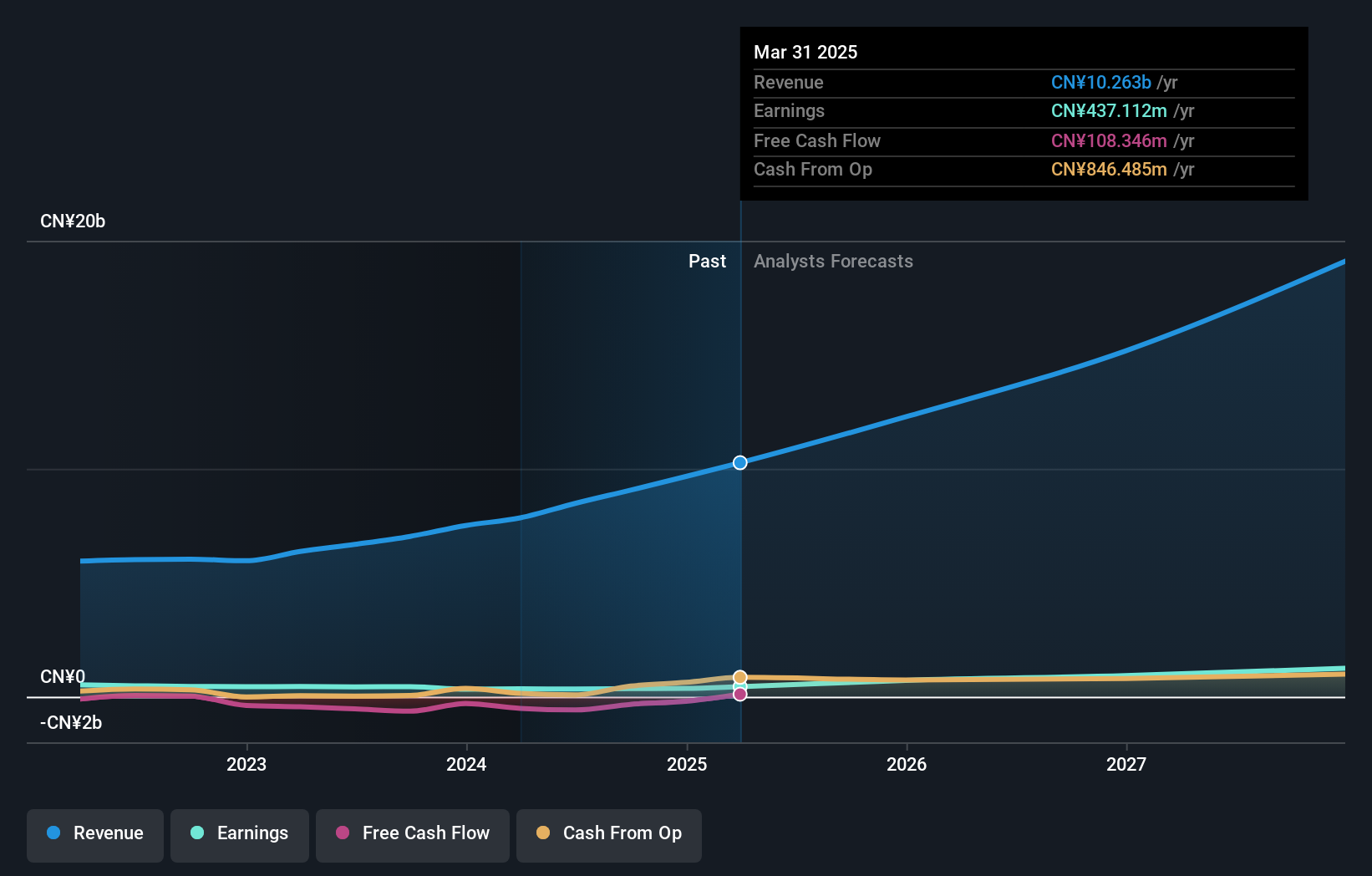

Overview: Hangzhou Jingye Intelligent Technology Co., Ltd. operates in the intelligent technology sector and has a market cap of CN¥3.98 billion.

Operations: The company's revenue primarily comes from its Machinery & Industrial Equipment segment, amounting to CN¥257.49 million.

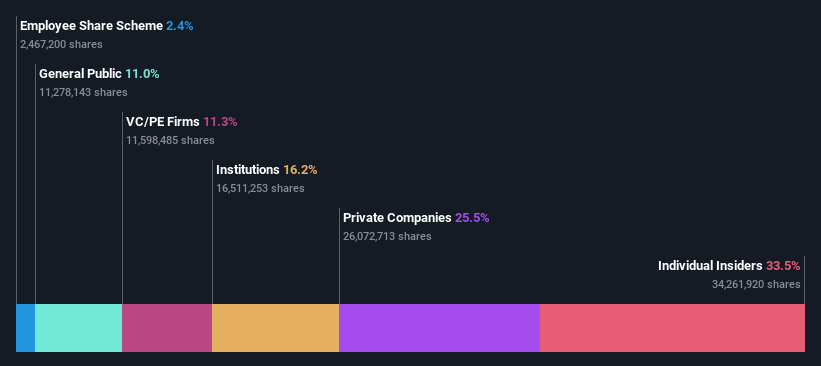

Insider Ownership: 33.5%

Hangzhou Jingye Intelligent Technology demonstrates significant growth potential with earnings expected to increase 55.6% annually, outpacing the Chinese market's 23.8%. Revenue is also projected to grow at 41.3% per year, surpassing market expectations. Despite a recent decline in profit margins from 23.7% to 14.2%, the company reported improved half-year net income of CNY 12.48 million and stable earnings per share growth, reflecting resilience amidst a highly volatile share price environment.

- Click here to discover the nuances of Hangzhou Jingye Intelligent Technology with our detailed analytical future growth report.

- Our valuation report unveils the possibility Hangzhou Jingye Intelligent Technology's shares may be trading at a premium.

Shenzhen H&T Intelligent ControlLtd (SZSE:002402)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Shenzhen H&T Intelligent Control Co. Ltd, along with its subsidiaries, engages in the research, development, manufacturing, sales, and marketing of intelligent controller products both in China and internationally with a market cap of CN¥10.43 billion.

Operations: The company's revenue is primarily derived from its Intelligent Controller Division, which accounts for CN¥8.28 billion, while the Integrated Circuit Division contributes CN¥193.90 million.

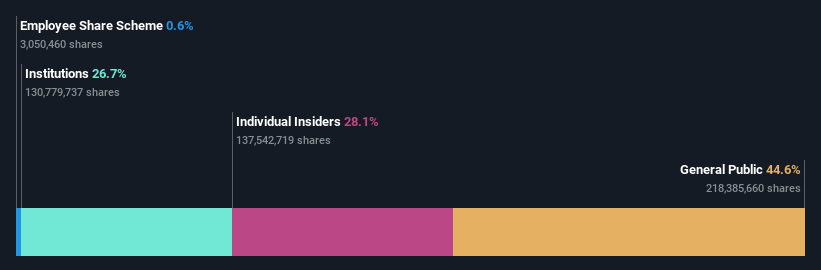

Insider Ownership: 16.2%

Shenzhen H&T Intelligent Control Ltd. shows promising growth prospects, with earnings anticipated to rise 44.1% annually, surpassing the Chinese market's 23.8%. Revenue is expected to grow at 20.9% per year, also exceeding market trends. Recent buybacks totaling CNY 104.99 million highlight management's confidence in the company's value proposition despite lower profit margins this year compared to last. Trading at a favorable price-to-earnings ratio of 31.1x relative to peers further underscores its potential as an attractive investment opportunity within its sector.

- Delve into the full analysis future growth report here for a deeper understanding of Shenzhen H&T Intelligent ControlLtd.

- According our valuation report, there's an indication that Shenzhen H&T Intelligent ControlLtd's share price might be on the cheaper side.

Hubei Century Network Technology (SZSE:300494)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Hubei Century Network Technology Inc. operates an online entertainment platform in China and internationally, with a market cap of CN¥5.93 billion.

Operations: The company's revenue is primarily derived from Gaming Operations (CN¥147.57 million), IP Operation (CN¥137.61 million), and Advertising and Value Added services (CN¥764.86 million).

Insider Ownership: 27.1%

Hubei Century Network Technology faces challenges with declining sales and net income, reporting CNY 539.57 million in revenue and CNY 4.07 million in net income for the half-year ending June 2024, a significant drop from the previous year. Despite this, its earnings are forecast to grow significantly at 57.5% annually, outpacing the Chinese market's growth rate of 23.8%. However, profit margins have decreased from last year’s levels of 14.5% to just 2.6%.

- Click here and access our complete growth analysis report to understand the dynamics of Hubei Century Network Technology.

- Our comprehensive valuation report raises the possibility that Hubei Century Network Technology is priced higher than what may be justified by its financials.

Turning Ideas Into Actions

- Unlock our comprehensive list of 1480 Fast Growing Companies With High Insider Ownership by clicking here.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Hangzhou Jingye Intelligent Technology might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SHSE:688290

Hangzhou Jingye Intelligent Technology

Hangzhou Jingye Intelligent Technology Co., Ltd.

Flawless balance sheet with high growth potential.