Advertisement

- China

- /

- Construction

- /

- SHSE:601133

Both Engineering Technology Co.,Ltd. Just Missed Earnings - But Analysts Have Updated Their Models

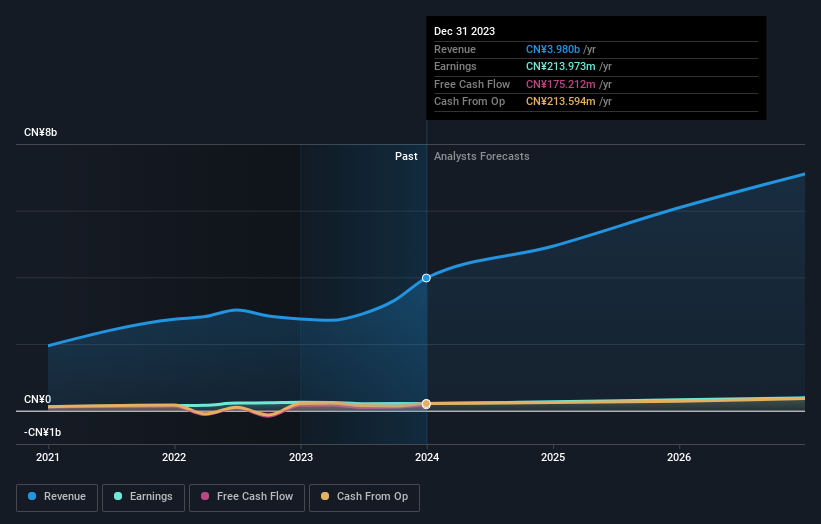

It's been a good week for Both Engineering Technology Co.,Ltd. (SHSE:601133) shareholders, because the company has just released its latest annual results, and the shares gained 3.3% to CN¥10.57. It was not a great result overall. While revenues of CN¥4.0b were in line with analyst predictions, earnings were less than expected, missing statutory estimates by 12% to hit CN¥0.45 per share. Earnings are an important time for investors, as they can track a company's performance, look at what the analysts are forecasting for next year, and see if there's been a change in sentiment towards the company. So we collected the latest post-earnings statutory consensus estimates to see what could be in store for next year.

View our latest analysis for Both Engineering TechnologyLtd

Taking into account the latest results, the consensus forecast from Both Engineering TechnologyLtd's two analysts is for revenues of CN¥4.93b in 2024. This reflects a huge 24% improvement in revenue compared to the last 12 months. Per-share earnings are expected to soar 25% to CN¥0.51. In the lead-up to this report, the analysts had been modelling revenues of CN¥5.17b and earnings per share (EPS) of CN¥0.68 in 2024. From this we can that sentiment has definitely become more bearish after the latest results, leading to lower revenue forecasts and a large cut to earnings per share estimates.

It'll come as no surprise then, to learn that the analysts have cut their price target 24% to CN¥12.99.

Of course, another way to look at these forecasts is to place them into context against the industry itself. The analysts are definitely expecting Both Engineering TechnologyLtd's growth to accelerate, with the forecast 24% annualised growth to the end of 2024 ranking favourably alongside historical growth of 15% per annum over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to grow their revenue at 10% per year. It seems obvious that, while the growth outlook is brighter than the recent past, the analysts also expect Both Engineering TechnologyLtd to grow faster than the wider industry.

The Bottom Line

The most important thing to take away is that the analysts downgraded their earnings per share estimates, showing that there has been a clear decline in sentiment following these results. Regrettably, they also downgraded their revenue estimates, but the latest forecasts still imply the business will grow faster than the wider industry. The consensus price target fell measurably, with the analysts seemingly not reassured by the latest results, leading to a lower estimate of Both Engineering TechnologyLtd's future valuation.

Following on from that line of thought, we think that the long-term prospects of the business are much more relevant than next year's earnings. At least one analyst has provided forecasts out to 2026, which can be seen for free on our platform here.

Don't forget that there may still be risks. For instance, we've identified 2 warning signs for Both Engineering TechnologyLtd that you should be aware of.

Valuation is complex, but we're here to simplify it.

Discover if Both Engineering TechnologyLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:601133

Both Engineering TechnologyLtd

Provides cleanroom system integration solutions for high-tech plant construction, technical transformation, and other projects in China.

Flawless balance sheet with limited growth.

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.8% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|7.6% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.5% undervalued

YI

Community Contributor